- Executive Summary

- Global Hot Melt Glue Labeler Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-economic Factors

- Global Sectoral Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Tool Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Analysis, 2025A

- Key Highlights

- Key Factors Impacting Deployment Costs

- Pricing Analysis, By Product Type

- Global Hot Melt Glue Labeler Market Outlook

- Key Highlights

- Market Volume (Units) Projections

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Current Market Size (US$ Bn) Analysis and Forecast, 2026 - 2033

- Global Hot Melt Glue Labeler Market Outlook: Product Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Product Type, 2020 - 2025

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Automatic

- Semi-Automatic

- Market Attractiveness Analysis: Product Type

- Global Hot Melt Glue Labeler Market Outlook: Label Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Label Type, 2020 - 2025

- Current Market Size (US$ Bn) Analysis and Forecast, By Label Type, 2026 - 2033

- Pre-Cut

- Roll-Fed

- Market Attractiveness Analysis: Label Type

- Global Hot Melt Glue Labeler Market Outlook: Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application, 2020 - 2025

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2026 - 2033

- Food

- Beverage

- Pharmaceutical

- Chemical

- Others

- Market Attractiveness Analysis: Application

- Key Highlights

- Global Hot Melt Glue Labeler Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Region, 2020 - 2025

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Region, 2026 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Hot Melt Glue Labeler Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product Type

- By Label Type

- By Application

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- U.S.

- Canada

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Automatic

- Semi-Automatic

- Current Market Size (US$ Bn) Analysis and Forecast, By Label Type, 2026 - 2033

- Pre-Cut

- Roll-Fed

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Food

- Beverage

- Pharmaceutical

- Chemical

- Others

- Market Attractiveness Analysis

- Europe Hot Melt Glue Labeler Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product Type

- By Label Type

- By Application

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Automatic

- Semi-Automatic

- Current Market Size (US$ Bn) Analysis and Forecast, By Label Type, 2026 - 2033

- Pre-Cut

- Roll-Fed

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Food

- Beverage

- Pharmaceutical

- Chemical

- Others

- Market Attractiveness Analysis

- East Asia Hot Melt Glue Labeler Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product Type

- By Label Type

- By Application

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- China

- Japan

- South Korea

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Automatic

- Semi-Automatic

- Current Market Size (US$ Bn) Analysis and Forecast, By Label Type, 2026 - 2033

- Pre-Cut

- Roll-Fed

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Food

- Beverage

- Pharmaceutical

- Chemical

- Others

- Market Attractiveness Analysis

- South Asia & Oceania Hot Melt Glue Labeler Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product Type

- By Label Type

- By Application

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Automatic

- Semi-Automatic

- Current Market Size (US$ Bn) Analysis and Forecast, By Label Type, 2026 - 2033

- Pre-Cut

- Roll-Fed

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Food

- Beverage

- Pharmaceutical

- Chemical

- Others

- Market Attractiveness Analysis

- Latin America Hot Melt Glue Labeler Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product Type

- By Label Type

- By Application

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Automatic

- Semi-Automatic

- Current Market Size (US$ Bn) Analysis and Forecast, By Label Type, 2026 - 2033

- Pre-Cut

- Roll-Fed

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Food

- Beverage

- Pharmaceutical

- Chemical

- Others

- Market Attractiveness Analysis

- Middle East & Africa Hot Melt Glue Labeler Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product Type

- By Label Type

- By Application

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Automatic

- Semi-Automatic

- Current Market Size (US$ Bn) Analysis and Forecast, By Label Type, 2026 - 2033

- Pre-Cut

- Roll-Fed

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Food

- Beverage

- Pharmaceutical

- Chemical

- Others

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- Krones AG

- Overview

- Segments and Deployments

- Key Financials

- Market Developments

- Market Strategy

- Sidel, Inc. (Tetra Laval Group)

- Sacmi Packaging SpA

- KHS Group

- Accutek Packaging Equipment Companies Inc.

- Propack Automation Limited

- Criveller Group

- Clearpack Group

- Multi-Tech Systems International Inc.

- Della Toffola SpA

- Aesus Packaging Systems, Inc.

- Krones AG

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Non-food Packaging

- Hot Melt Glue Labeler Market

Hot Melt Glue Labeler Market Size, Share, and Growth Forecast, 2026 - 2033

Hot Melt Glue Labeler Market by Product Type (Automatic, Semi-Automatic), Label Type (Pre-Cut, Roll-Fed), Application (Food, Beverage, Pharmaceutical, Chemical, Others), and Regional Analysis for 2026 - 2033

Key Industry Highlights

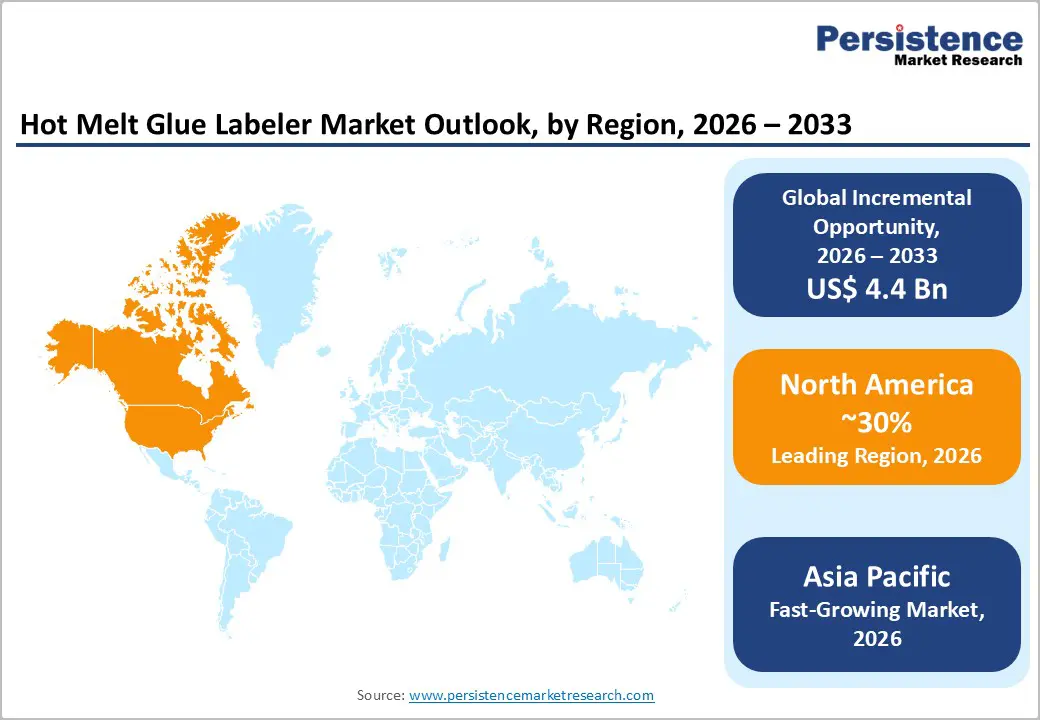

- Dominant Region: By 2026, North America is expected to lead with an estimated 30% market share, on the back of advanced packaging infrastructure and high-speed bottling operations.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, driven by escalating packaged goods demand and adoption of automated labeling technologies.

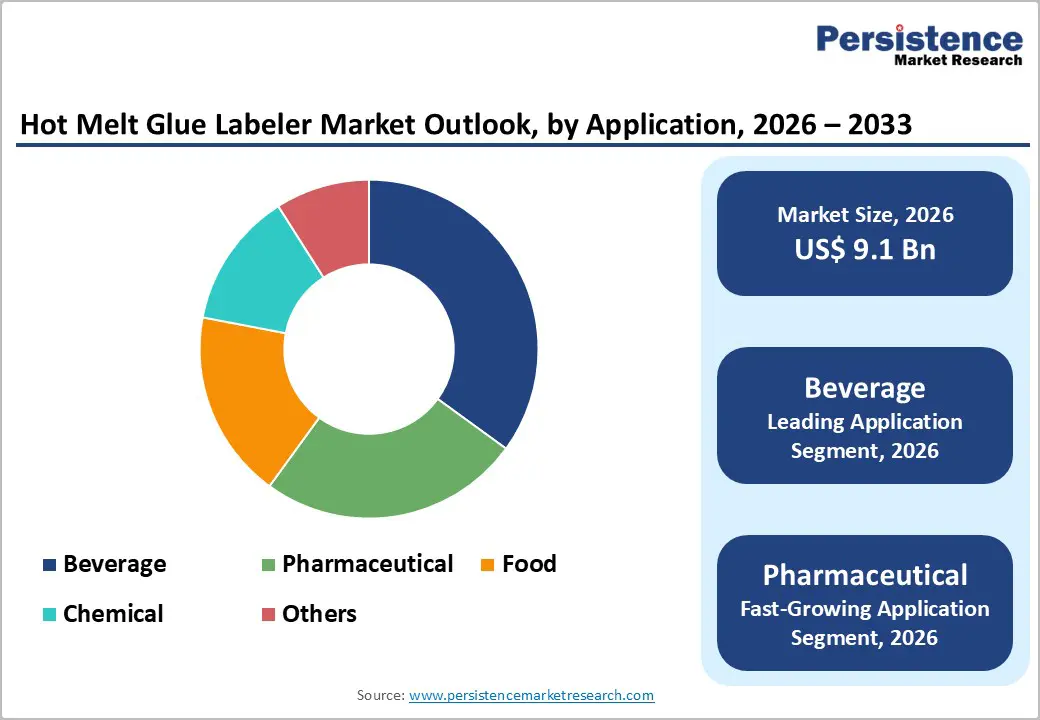

- Leading Application: Beverage are likely to dominate with a projected 35% revenue share in 2026, supported by high production volumes, continuous bottling operations, and regulatory labeling standards.

- Fastest-growing Application: Pharmaceutical are anticipated to be the fastest-growing segment from 2026 to 2033, propelled by serialization mandates and anti-counterfeiting measures.

- October 2025: ACMI launched the Opera Omnia modular labeler, designed to handle roll-fed, cold glue, self-adhesive, and hot melt applications within a single platform to improve production flexibility and automation.

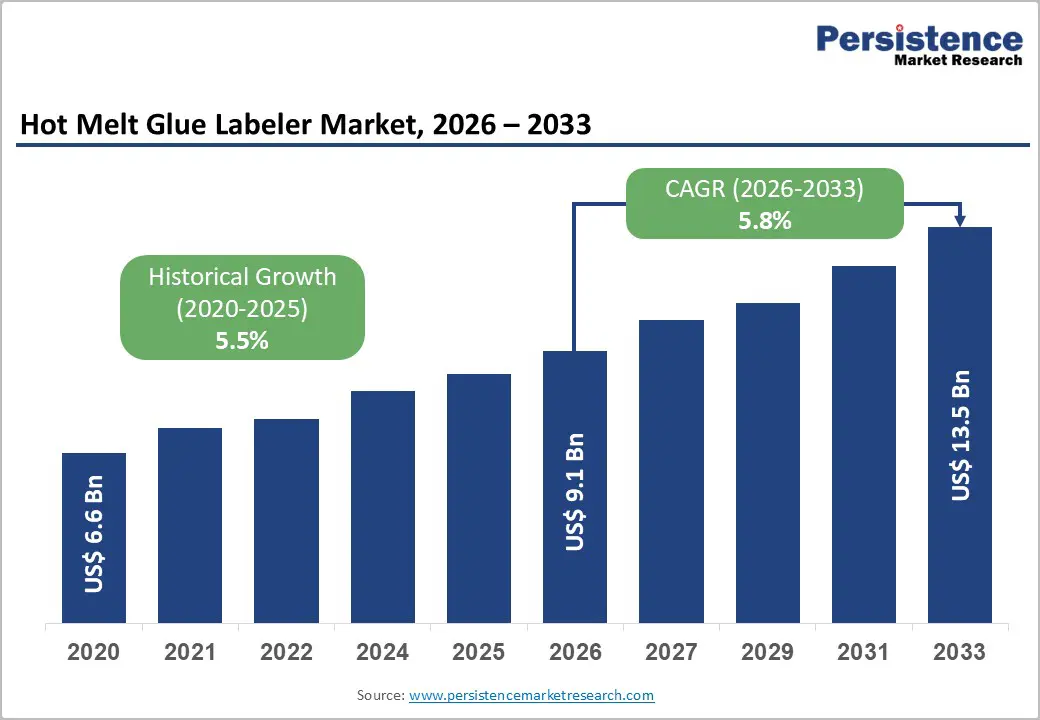

| Key Insights | Details |

|---|---|

|

Hot Melt Glue Labeler Market Size (2026E) |

US$ 9.1 Bn |

|

Market Value Forecast (2033F) |

US$ 13.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Need for Cost-Effective Labeling Solutions for High-Volume Production

High-volume manufacturing environments are intensely focused on reducing per-unit packaging costs and eliminating bottlenecks that affect throughput and profitability. When production scales into millions of units per month, even a minor inefficiency in labeling can translate into significant operational expense or downtime. Hot melt glue labeling systems provide rapid bonding with minimal adhesive waste and very fast cure times, supporting continuous operation on high-speed conveyor systems while reducing rework and label misalignment. Lower material consumption and stable performance under continuous use lead to predictable operating budgets, which is critical for manufacturing cost control and competitiveness in crowded product categories such as beverages, consumer goods, and pharmaceuticals.

Industrial production trends reinforce the need for cost-efficient production infrastructure. Official data from the Ministry of Statistics and Programme Implementation (MOSPI) show that the Index of Industrial Production (IIP) recorded 7.8% growth in December 2025, while manufacturing output increased by 8.1% year on year. Rising output levels indicate expanding production volumes across sectors. In this environment, labeling efficiency directly influences overall packaging economics, as it represents a recurring operational cost within high-speed manufacturing systems. Strategic investment in efficient labeling technology supports scalable production while maintaining disciplined expenditure management.

Expansion of Organized Retail and Packaged Goods Consumption Globally

Organized retail growth and rising packaged goods consumption are reshaping packaging operations across food, beverage, pharmaceutical, and household product manufacturing. Modern retail formats demand uniform labeling standards, machine-readable codes, batch traceability, and compliance-ready product information to support centralized procurement and digital inventory systems. Large production volumes within fast-moving consumer goods environments require labeling equipment capable of operating at high speeds with consistent adhesive application and minimal line interruptions. Hot melt glue labeling systems align with these operational requirements through rapid bonding strength, precise label positioning, and compatibility with multiple container materials including glass, metal, and polymer substrates. Expansion of private label portfolios within supermarkets and hypermarkets further increases labeling frequency, driving equipment upgrades and capacity expansion in manufacturing facilities.

Urbanization, evolving consumption habits, and wider product assortments intensify stock keeping unit proliferation across organized retail shelves. Manufacturers introduce frequent product variants, promotional packs, and limited-edition formats to maintain shelf visibility and competitive differentiation. Each variation requires efficient label changeovers, reliable adhesion under varied storage conditions, and stable performance during transportation and distribution. Hot melt systems support high-throughput environments where packaging lines operate continuously to meet retail replenishment cycles. Greater integration of automated warehousing and barcode-based tracking reinforces the need for durable, accurately positioned labels that maintain readability across the supply chain.

Fluctuations in Adhesive Raw Material Prices Affecting Operational Costs

Volatility in petrochemical-derived inputs used in hot melt adhesives creates structural cost uncertainty across industrial labeling operations. Key raw materials such as ethylene-vinyl acetate polymers, hydrocarbon resins, and specialty waxes are directly linked to crude oil and natural gas supply chains, exposing adhesive pricing to geopolitical developments, refinery utilization rates, trade policies, and feedstock availability cycles. Price shifts in upstream energy markets transmit rapidly through polymer manufacturing networks, resulting in frequent revisions to adhesive procurement contracts. This cost instability limits pricing visibility for manufacturers operating continuous, high-speed labeling lines where adhesive consumption volumes remain constant and non-substitutable in the short term.

Operating expenditure models in automated labeling environments rely on stable consumable input pricing to maintain margin discipline. Adhesive systems require controlled heating, storage, and metered application, preventing sudden formulation changes without technical recalibration and quality validation. When raw material prices rise unpredictably, procurement budgets expand while finished goods pricing often remains constrained by retail agreements and competitive pressure. Financial planning complexity increases, particularly for mid-scale producers with limited leverage in supplier negotiations and reduced capacity to hedge commodity exposure. Production scheduling decisions, supplier diversification strategies, and capital investment planning become more conservative under sustained price uncertainty.

Availability of Alternative Labeling Technologies

Competitive pressure from alternative labeling technologies is a key restraint because manufacturers frequently evaluate multiple options and may select formats that deliver operational simplicity and broader substrate compatibility. Self-adhesive, pressure-sensitive labels dominate the label application landscape, accounting for a significant share of label usage due to their ease of handling and ability to adhere reliably across diverse surfaces including glass, plastic and metal. A U.S. government Federal Register notice related to food labeling procedures references the regulatory context for pressure-sensitive sticker use in 2025, underscoring how widely this method is codified in compliance frameworks for packaged products.

Packaging operations under time constraints or with frequent product changeovers gravitate toward technologies that minimize setup complexity and training requirements. Pressure-sensitive systems eliminate the need for heated glue application or curing processes, reducing mechanical complexity, energy consumption and potential points of failure on an automated line. This means that businesses with diverse product portfolios or premium packaging runs can maintain throughput without extensive operator intervention. At the same time, other alternatives like in-mold, heat-shrink or direct printed solutions offer distinct advantages such as full-surface coverage or integration with specific container formats.

Integration of Industry 4.0 Technologies to Open New Avenues

Adoption of smart sensors and predictive maintenance systems strengthens operational intelligence across automated labeling lines by converting real-time machine data into structured performance insights. Sensors track parameters such as adhesive temperature, viscosity stability, motor vibration, pressure levels, and cycle timing, enabling early identification of irregularities that may affect label placement accuracy or bonding strength. Continuous monitoring supports condition-based servicing rather than fixed maintenance intervals, improving planning accuracy and reducing unexpected production interruptions. Data transparency enhances decision-making at plant level by providing measurable indicators linked to throughput efficiency, defect rates, and machine utilization.

Strategic value emerges through improved asset reliability, optimized maintenance expenditure, and enhanced production continuity. Predictive analytics models assess historical performance trends and trigger alerts before component fatigue or adhesive system blockages escalate into line shutdowns. Structured maintenance scheduling minimizes emergency repairs, reduces material wastage, and stabilizes output quality standards. Integration with enterprise resource planning systems enables better spare-parts forecasting and workforce allocation, strengthening cost control frameworks. Digital connectivity also supports compliance documentation and audit traceability within regulated production environments.

Development of Sustainable and Bio-Based Adhesives to Meet Environmental Regulations

Formulation of sustainable and bio-based hot melt adhesives represents a strategic opportunity driven by tightening environmental regulations and structured government procurement policies that prioritize renewable materials. Regulatory authorities are advancing circular economy frameworks, emission reduction targets, and responsible material usage standards that influence adhesive selection across industrial applications. The U.S. Department of Agriculture (USDA) administers the BioPreferred® Program to promote procurement of certified bio-based products within federal purchasing. This policy direction signals long-term institutional commitment toward renewable material integration within supply chains and manufacturing ecosystems.

Industrial buyers are embedding environmental, social, and governance (ESG) performance metrics into supplier qualification processes, increasing preference for materials aligned with carbon reduction and low-emission objectives. Bio-based hot melt adhesives support compliance with volatile organic compound (VOC) control standards overseen by the U.S. Environmental Protection Agency (EPA), while contributing to sustainability disclosures and responsible sourcing mandates. Brand owners in food packaging, pharmaceutical, and consumer goods sectors are advancing decarbonization roadmaps that require environmentally aligned input materials. Adoption of renewable adhesive formulations strengthens regulatory preparedness, enhances eligibility for sustainability-driven procurement contracts, and supports long-term risk mitigation against evolving environmental legislation.

Category-wise Analysis

Product Type Insights

Automatic is anticipated to secure around 68% of the hot melt glue labeler market revenue share in 2026, reflecting strong adoption in high-volume manufacturing environments. Large beverage bottling plants and pharmaceutical packaging units require continuous, high-speed operation with integrated inspection systems. Automatic systems deliver consistent adhesive temperature control, rapid changeover, and reduced labor dependency. Provider preference centers on throughput optimization, lower defect rates, and compatibility with serialization modules. Accessibility to industrial financing and integration with digital monitoring systems further strengthens segment dominance. Production environments operating multi-shift schedules benefit from stable performance, minimal downtime, and synchronized conveyor integration. Advanced sensor-based alignment systems improve label placement accuracy across diverse container formats.

Semi-automatic is expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by rising demand from small and medium-sized manufacturers seeking cost-efficient automation upgrades. This segment offers flexible operation, simplified maintenance, and lower capital barriers. Adoption increases in regional food processing units transitioning from manual labeling. Innovation in modular designs enhances scalability and supports incremental automation pathways. Equipment footprint suitability for compact production facilities improves accessibility for emerging enterprises. Operator-assisted control enables precision adjustments for varied packaging sizes and seasonal production runs. Reduced energy consumption and adaptable configuration support operational efficiency.

Application Insights

Beverages are likely to be the leading segment with a projected 35% of the hot melt glue labeler market share in 2026 due to high production volumes and continuous bottling operations. Regulatory labeling standards covering nutritional disclosure and batch identification reinforce equipment upgrades. Digitalization of bottling plants and cost efficiency imperatives further strengthen this segment. High-speed filling lines demand synchronized labeling systems capable of maintaining alignment accuracy across varied bottle shapes and materials. Carbonated drinks, bottled water, juices, and alcoholic beverages operate under strict throughput targets, requiring reliable adhesive performance and minimal downtime. Integration with automated inspection cameras supports defect detection and quality assurance.

Pharmaceutical are anticipated to be the fastest-growing segment from 2026 to 2033, fueled by serialization mandates, anti-counterfeiting measures, and technology-enabled inspection systems. Clinical credibility and provider referrals increase packaged medicine distribution. Compliance-driven investment in precise adhesive application enhances growth prospects. Stringent regulatory frameworks require clear batch coding, tamper evidence, and track-and-trace compatibility across primary packaging formats. Growth in generic drug production and vaccine distribution increases labeling complexity and volume requirements. Automated verification systems linked with enterprise resource planning platforms strengthen data transparency and audit readiness.

Regional Insights

North America Hot Melt Glue Labeler Market Trends

North America is expected to lead with an estimated 30% of the hot melt glue labeler market value in 2026, aided by advanced packaging infrastructure and widespread adoption of automated labeling systems across beverage, pharmaceutical, and consumer goods production. Continuous high-speed bottling operations and multi-shift manufacturing schedules require precise adhesive application, integrated inspection modules, and minimal downtime, creating strong demand for reliable hot melt glue solutions. Regulatory compliance with serialization, anti-counterfeiting, and traceability standards further incentivizes investment in high-precision equipment. Large-scale contract manufacturing and multi-national production units prioritize throughput optimization, consistent quality, and rapid changeover, reinforcing market dominance.

Integration with digital monitoring and predictive maintenance systems improves operational visibility, reduces unplanned interruptions, and strengthens supplier preference for technologically advanced labeling systems. Operational efficiency and adaptability drive additional growth, as manufacturers manage diverse container shapes, multi-material packaging, and specialty products requiring flexible labeling capabilities. Capital availability and established supplier networks facilitate adoption of high-capacity solutions, supporting rapid scaling and modernization of existing lines. Emphasis on sustainability, waste reduction, and traceable production further reinforces investment in automated hot melt glue labelers.

Europe Hot Melt Glue Labeler Market Trends

Europe holds a central position in the market for hot melt glue labelers, backed by mature manufacturing infrastructure, high regulatory standards, and strong demand from beverage, pharmaceutical, and consumer goods industries. Advanced production facilities emphasize precision, quality, and operational reliability, creating consistent demand for automated and semi-automated labeling systems. Strict labeling and traceability requirements for food, beverages, and pharmaceutical products drive investment in equipment capable of maintaining compliance with serialization, batch coding, and anti-counterfeiting standards. Established industrial supply chains favor technology that ensures consistent adhesive application, minimal defects, and seamless integration with inspection and digital monitoring systems.

Sustainability and energy efficiency initiatives further influence equipment adoption, as industrial operators seek solutions that reduce adhesive waste, lower energy consumption, and align with environmental regulations. Modular and scalable systems enable incremental upgrades, supporting continuous production improvement without significant line disruption. Strong technical support networks, financing availability, and supplier collaboration facilitate rapid deployment of high-performance labeling solutions. Growth is reinforced by increasing demand for premium and export-oriented products, which require precise, high-quality labeling to maintain brand reputation and regulatory compliance.

Asia Pacific Hot Melt Glue Labeler Market Trends

Asia Pacific is forecasted to be the fastest-growing market for hot melt glue labelers between 2026 and 2033, propelled by rapid industrial expansion, rising packaged goods demand, and increasing adoption of automated production technologies. High-volume beverage bottling, pharmaceutical packaging, and consumer goods manufacturing are modernizing legacy lines to enhance throughput, reduce labor dependence, and ensure precise adhesive application across varied container formats. Government initiatives supporting industrial infrastructure and technology adoption facilitate integration of digital monitoring, inspection systems, and advanced process controls. Export-oriented manufacturing drives compliance with international labeling and traceability standards, further stimulating demand for high-performance labeling solutions.

Flexible financing and modular equipment designs accelerate adoption among small and medium-sized manufacturers transitioning from manual operations, enabling scalable automation aligned with growth strategies. Precision adhesive application, reduced downtime, and enhanced reliability improve production margins while supporting regulatory and quality compliance. Integration with serialization, inspection, and digital monitoring platforms strengthens supply chain visibility and operational transparency. Rising regional manufacturing capacity, coupled with cost-effective modernization, positions the market for accelerated expansion, combining industrial growth, technology adoption, and increasing end-user demand to drive sustained hot melt glue labeler deployment across Asia Pacific.

Competitive Landscape

The global hot melt glue labeler market structure is moderately consolidated, with key players such as Krones AG, Sidel, Sacmi Packaging SpA, KHS Group, and Accutek Packaging collectively capturing a substantial portion of market share. These companies leverage advanced automation technologies, precision adhesive application systems, and integrated inspection solutions to maintain leadership positions. Their focus on research and development enables continuous innovation in high-speed labeling, temperature-controlled adhesive delivery, and modular equipment designs. Global distribution networks and established service infrastructures allow these players to cater to multinational beverage, pharmaceutical, and consumer goods manufacturers, ensuring reliable installation, maintenance, and technical support.

Beyond the dominant players, the remainder of the market consists of regional manufacturers and specialized equipment providers offering semi-automated or niche solutions tailored to small and medium-sized production facilities. These companies often capitalize on cost-efficient designs, flexible configurations, and localized service offerings to address emerging market demand. The market structure allows leading players to pursue global expansion while enabling smaller companies to focus on niche applications, such as specialty packaging or modular automation solutions. Strategic partnerships, technological collaboration, and targeted customer engagement further reinforce competitive positioning.

Key Industry Developments

- In January 2026, Super Bond Adhesives showcased its Hot-Melt Pressure Sensitive Adhesive (HMPSA) range at Pamex, highlighting enhanced adhesive performance and versatility for label and packaging applications.

- In September 2025, BioBond Adhesives, Inc. entered the hot melt market with its new BioMelt™ plant-based pressure sensitive adhesive offerings for labels, tape, and industrial uses, expanding sustainable, biobased technology options for adhesive applications.

- In August 2025, Henkel introduced Technomelt EM 335 RE, a new hot melt adhesive for PET bottle labeling that enables up to 98 % adhesive removal during recycling and supports cleaner PET flake production while maintaining high bonding performance and regulatory compliance.

Companies Covered in Hot Melt Glue Labeler Market

- Krones AG

- Sidel, Inc. (Tetra Laval Group)

- Sacmi Packaging SpA

- KHS Group

- Accutek Packaging Equipment Companies Inc.

- Propack Automation Limited

- Criveller Group

- Clearpack Group

- Multi-Tech Systems International Inc.

- Della Toffola SpA

- Aesus Packaging Systems, Inc.

Frequently Asked Questions

The global hot melt glue labeler market is projected to reach US$ 9.1 billion in 2026.

Increasing demand for automated, high-speed labeling solutions across beverage, pharmaceutical, and consumer goods industries is driving the market.

The market is poised to witness a CAGR of 5.8% from 2026 to 2033.

Adoption of sustainable bio-based adhesives, integration of digital monitoring systems, and expansion in emerging manufacturing hubs represent key market opportunities.

Some of the key market players include Krones AG, Sidel, Inc. (Tetra Laval Group), Sacmi Packaging SpA, KHS Group, Accutek Packaging Equipment Companies Inc.