- Telecommunications

- Fiber Optics Market

Fiber Optics Market Size, Share, and Growth Forecast 2026 - 2033

Fiber Optics Market by Fiber Type (Glass Optical Fiber, Plastic Optical Fiber; Specialty Optical Fibers), by Deployment (Underground, Aerial, Underwater), by Application (Communication, Non-Communication), by Industry (IT & Telecom, Defense & Aerospace, Healthcare, Energy & Utilities, Manufacturing, Automotive, Government/Public Sector), by Regional Analysis, 2026 - 2033

Fiber Optics Market Size and Trend Analysis

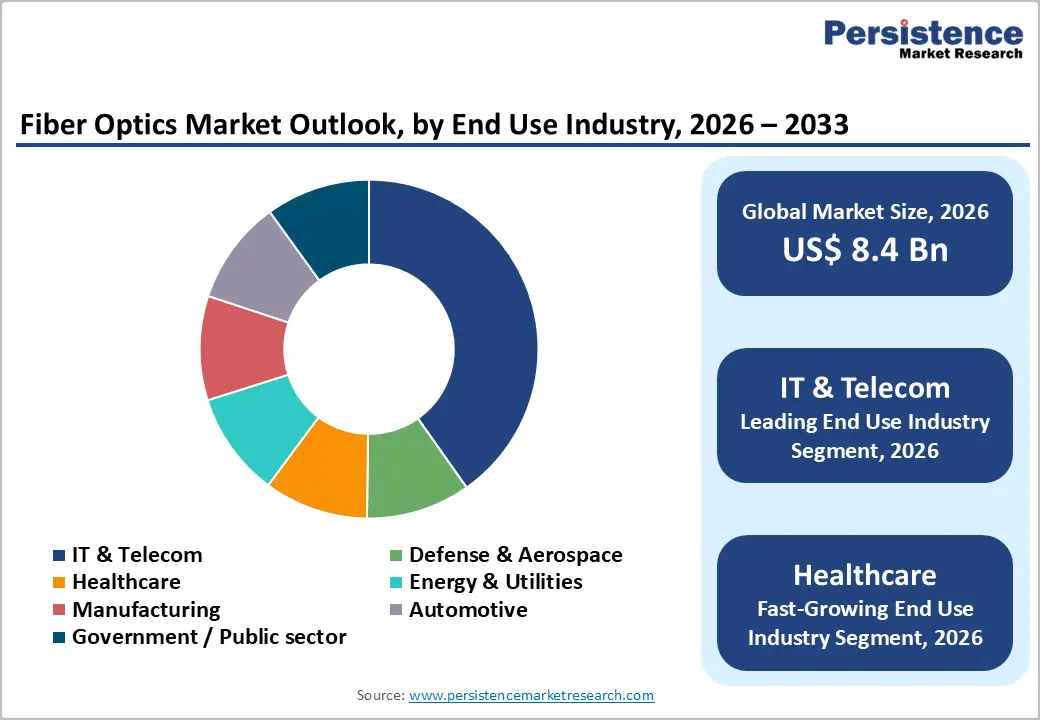

The global fiber optics market size is expected to be valued at US$ 8.4 billion in 2026 and projected to reach US$ 16.9 billion by 2033, growing at a CAGR of 10.5% between 2026 and 2033. This is fundamentally driven by the global acceleration of 5G network rollouts, which require dense fiber backhaul infrastructure, and the unprecedented scale-up of hyperscale data centers fueled by AI workloads and cloud computing.

Governments across North America, Asia Pacific, and Europe are committing billions in public funding, including the US$ 42.45 billion Broadband Equity, Access, and Deployment (BEAD) Program in the United States, to extend high-speed connectivity to underserved regions, directly expanding the addressable market for fiber optics manufacturers and deployment service providers.

Key Industry Highlights

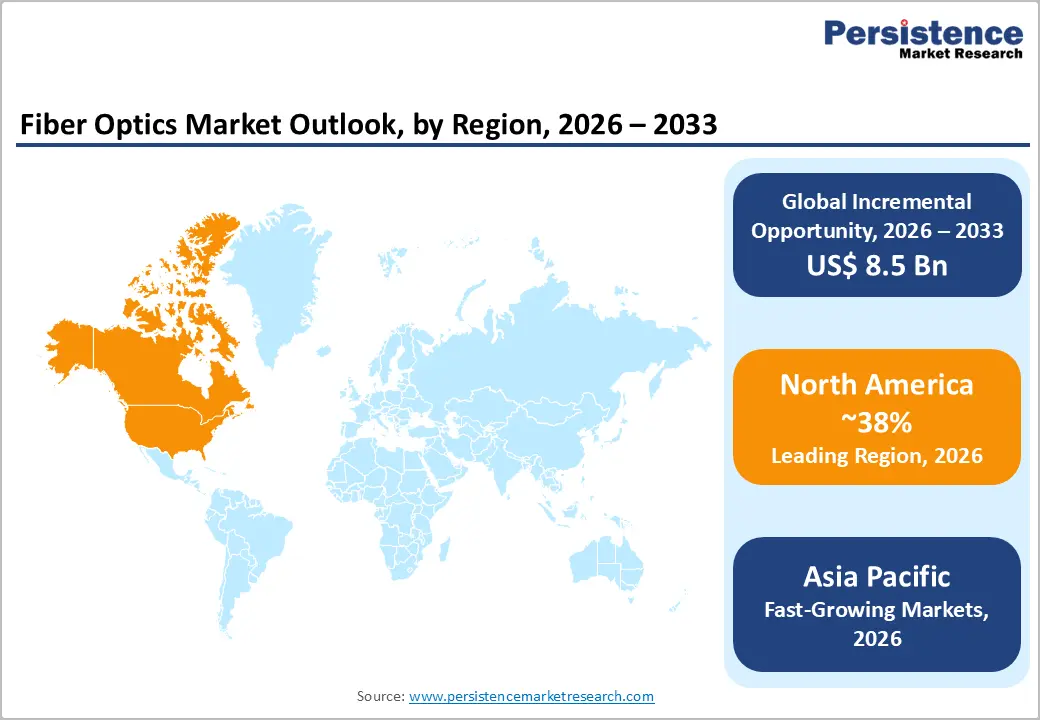

- Leading Region: North America holds approximately 38% of the global fiber optics market share in 2025, driven by massive federal broadband funding programs, aggressive 5G infrastructure investments, and accelerating AI data center buildouts by hyperscalers.

- Fastest Growing Region: Asia Pacific is the fastest growing region with a projected CAGR exceeding 12% through 2033, catalyzed by large-scale government FTTH mandates, 5G network densification across China, India, and Southeast Asia, and a world-leading fiber manufacturing base.

- Dominant Optical Fiber: Single-mode GOF commands approximately 52% market share in 2025, sustained by its essential role in 5G backhaul, long-haul backbone networks, and hyperscale data center interconnects requiring low-loss, high-bandwidth performance over extended distances.

- Fastest Growing End-Use: The Healthcare end-use segment is the fastest growing category with a projected CAGR above 13% through 2033, driven by expanding adoption in surgical imaging, telemedicine infrastructure, and remote patient monitoring networks globally.

- Key Opportunity: The AI-driven hyperscale data center build-out represents a high-margin, premium-pricing opportunity for specialty fiber manufacturers; companies with AI-optimized high-density cable solutions, such as Corning's GlassWorks AI™, are best positioned to capture this growing and underserved demand.

Market Dynamics

Drivers - 5G Infrastructure Rollout Creating Structural Demand for Fiber Backhaul

The deployment of 5G networks represents the most consequential demand catalyst for the fiber optics industry, as every 5G small cell requires fiber backhaul to function effectively. Industry stakeholders, telecom operators, infrastructure vendors, and cable manufacturers stand to benefit from a prolonged investment cycle as mobile network operators race to build out high-frequency 5G coverage.

According to the International Telecommunication Union (ITU), global mobile subscriptions are surpassing 8 billion, with 5G accounts anticipated to represent the largest growth cohort through the end of the decade. Mobile operators worldwide are projected to carry 60% of all mobile traffic over fiber by 2026, directly driving procurement of single-mode fiber cables for long-haul and metro-backhaul applications. This structural shift from copper to fiber is irreversible, and companies with vertically integrated manufacturing and installation capabilities are best positioned to capture sustained revenue growth.

Government Broadband Mandates and Public-Sector Fiber Investment

National broadband programs worldwide are transforming government policy into a reliable, large-scale demand engine for fiber optics, a signal that market participants should treat as a durable multi-year revenue opportunity rather than cyclical stimulus. The US Infrastructure Investment and Jobs Act committed US$ 65 billion specifically for broadband expansion, with the BEAD Program directing US$ 42.45 billion primarily toward fiber deployments in unserved and underserved areas.

Similarly, the European Union's Digital Decade 2030 targets mandate that all EU households have access to gigabit connectivity by the end of the decade. In the Asia Pacific, India's BharatNet Phase III program targets connectivity to 600,000 villages using optical fiber, backed by a government investment of approximately US$ 13 billion. These policy commitments directly underwrite fiber cable procurement, making governments among the most creditworthy and large-volume customers in the market.

Restraints - High Capital Expenditure and Labor-Intensive Deployment Costs

The capital intensity of fiber optic deployment acts as a structural barrier that suppresses the pace of network expansion, particularly in low-density rural and remote geographies. According to the 2024 Fiber Deployment Cost Annual Report published by the Fiber Broadband Association (FBA), labor costs now constitute 60-80% of total fiber deployment project expenses, a figure that has climbed steadily as skilled installation crews remain scarce relative to demand.

This cost structure creates a self-limiting dynamic where regions most in need of connectivity are also the least economically viable to serve, leading operators to prioritize dense urban corridors unless supported by government subsidies. For new entrants and smaller regional players, high upfront capital requirements and long payback periods create financing constraints that limit market entry. This reinforces the dominance of well-capitalized incumbents while slowing broader infrastructure expansion.

Supply Chain Vulnerabilities and Raw Material Concentration Risks

The fiber optics supply chain carries a concentrated risk profile that translates directly into delivery delays, price volatility, and margin pressure for cable manufacturers and network builders. The production of optical fiber preforms, the foundational raw material, relies on highly purified silica and specialty chemical inputs, the sourcing of which is geographically concentrated, with China controlling a disproportionate share of global production capacity for key precursor materials.

Supply disruptions or geopolitical tensions along this chain can create extended lead times and elevated input costs that erode project economics. Additionally, the rapid surge in AI data center construction has tightened global fiber supply in 2024-2025, with some manufacturers reporting lead times extending to 12-18 months for certain cable types. This supply tightness disadvantages smaller buyers and creates execution risk for time-sensitive government-funded broadband projects, potentially causing missed deployment milestones and cost overruns.

Opportunities - AI-Driven Hyperscale Data Center Expansion Unlocking Premium Fiber Demand

The rapid proliferation of artificial intelligence workloads is creating a high-value demand segment for fiber optics that rewards innovation over pure volume, a window that specialty fiber manufacturers and high-density cable solution providers should move quickly to capture. Corning Incorporated reported that its enterprise sales grew 58% year-over-year in Q3 2025, driven primarily by its Gen AI products as hyperscalers accelerate infrastructure buildouts.

The company's GlassWorks AI™ solutions, launched in March 2025, target the specific requirements of AI data centers, high fiber density, bend resilience, and rapid deployment capability. The Contour™ Flow Cable, which doubles fiber capacity within existing conduit diameters, exemplifies the product differentiation opportunities that exist for manufacturers who understand the unique constraints of data center floor planning. As global AI capital expenditure by leading technology firms continues to escalate through the forecast period, companies with AI-optimized fiber portfolios will command premium pricing and preferred-supplier relationships with the world's most creditworthy buyers.

Emerging Market Broadband Buildouts Creating High-Volume, High-Growth Demand Centers

Developing economies across Southeast Asia, Sub-Saharan Africa, and Latin America represent a structurally underserved market where the combination of rising digital demand, falling fiber costs, and increasing multilateral funding is creating a compelling, time-sensitive growth opportunity for cable manufacturers and network builders. In 2024 alone, over 250,000 km of new fiber lines were installed across emerging economies to support education, telehealth, and digital inclusion initiatives.

Nigeria's President Bola Tinubu announced a US$ 2 billion investments in February 2025 to accelerate nationwide fiber deployment. The World Bank and regional development banks are actively co-financing fiber infrastructure projects to bridge the digital divide, providing de-risked capital structures that lower the investment threshold for private operators. Companies that establish early distribution and installation partnerships in these markets will gain first-mover advantages in markets that could represent among the fastest-growing demand centers through 2033.

Category-wise Analysis

Fiber Type Insights

The Glass Optical Fiber (GOF) - Single Mode segment commands an approximately 52% share of the fiber optics market in 2025, a leadership position grounded in structural technical advantages rather than mere incumbency. Single-mode fiber's ability to transmit data over distances exceeding 100 km with minimal attenuation makes it the default specification for telecom operators building 5G backhaul, long-haul backbone networks, and subsea cable systems.

The global build-out of hyperscale data center interconnects further entrenches single-mode dominance, as these facilities require high-density, low-loss fiber to manage the bandwidth demands of cloud and AI applications.

The specialty optical fibers are the fast-growing segment within fiber type, which is gaining rapid traction in healthcare imaging, defense sensing, and industrial monitoring applications that require fiber tailored for extreme environments, high sensitivity, or wavelength-specific performance, attributes that command significant price premiums over commodity glass fiber.

Deployment Insights

The underground deployment segment holds the leading market share of approximately 45% in 2025, reflecting its structural suitability for dense urban environments where the majority of high-bandwidth subscribers are concentrated. Underground conduit systems offer superior protection against weather-related outages, physical damage, and signal interference, attributes that incentivize network operators and municipalities to specify underground routes despite higher upfront civil works costs.

Major FTTH (Fiber-to-the-Home) programs in South Korea, China, and the United States have predominantly followed underground routes in urban and suburban roll-outs, creating consistent demand for conduit, micro-duct, and direct-buried cable products. The Fastest Growing Deployment Segment is Aerial deployment, driven by its cost efficiency in rural broadband expansion programs, particularly in markets such as India and Sub-Saharan Africa, where civil construction costs make underground trenching economically prohibitive at scale.

Application Insights

The communication application segment accounts for approximately 72% of the fiber optics market in 2025, an enduring leadership position sustained by the insatiable global appetite for bandwidth across fixed broadband, mobile backhaul, and enterprise connectivity. The explosion of data-intensive applications, video streaming, cloud gaming, remote work platforms, and AI inference services, is continuously compressing the timeline within which operators must upgrade network capacity, making fiber the structural backbone of every major communication network upgrade cycle

The Telecommunications segment alone contributed approximately 42% of total market revenue in 2025, according to industry analysis. The Non-communication segment represents the fastest-growing application driven by expanding adoption in industrial automation, medical diagnostics, defense sensing systems, and distributed energy monitoring, segments where fiber's immunity to electromagnetic interference and precision sensing capabilities are creating new use cases beyond traditional data transmission.

Industry Insights

The IT & Telecom end-use segment commands approximately 43% of the fiber optics market in 2025, a share sustained by the sector's role as the primary infrastructure investor and network operator in the digital economy. Telecom operators globally are executing the most significant network transformation programs in a generation, replacing legacy copper infrastructure with all-fiber networks to support 5G deployment, FTTH roll-outs, and enterprise connectivity upgrades.

The scale of this transition is evidenced by the commitment of over 100 providers in the UK collectively investing more than £40 billion in gigabit-capable broadband networks. The Fastest Growing End-Use Segment is Healthcare, where fiber optics are finding expanding applications in surgical imaging systems, telemedicine infrastructure, remote patient monitoring networks, and hospital information systems, a convergence of clinical and digital transformation trends that is driving double-digit procurement growth from healthcare institutions globally.

Regional Insights

North America Fiber Optics Market Trends and Insights

North America holds the largest regional share of the global fiber optics market at approximately 38% in 2025, anchored by the United States' world-leading investment in broadband infrastructure modernization. The region's competitive dynamics are shaped by the convergence of federally-funded rural broadband programs, aggressive private investment by major telecom operators, and the unprecedented capex surge from AI data center construction.

The BEAD Program, Rural Digital Opportunity Fund (RDOF), and Capital Projects Fund (CPF) are collectively channeling tens of billions of dollars into fiber deployments in underserved markets, providing a durable policy backstop to private demand. North America is on a clear trajectory toward near-universal fiber coverage, with the window for capturing government-backed deployment contracts expected to be especially active through 2030.

U.S. Fiber Optics Market Size

The United States accounts for approximately 87% of North American fiber optics demand, driven by aggressive investments from carriers such as AT&T, Verizon, and Comcast in fiber-to-the-home rollouts. By the end of 2023, fiber had passed nearly 77.9 million U.S. homes, over 50% of all residences, according to the Fiber Broadband Association (FBA). The BEAD Program's US$ 42.45 billion commitments are expected to drive additional large-scale deployments in rural areas through 2028, positioning the U.S. as the leading single-country market for fiber cable procurement globally through the forecast horizon.

Europe Fiber Optics Market Trends and Insights

Europe represents approximately 20% of the global fiber optics market, with growth underpinned by the European Union's Digital Decade 2030 targets requiring gigabit connectivity for all households. The region's regulatory environment is distinctly favorable, with national governments providing structured subsidy frameworks, including the UK's £0.5 billion Project Gigabit, Germany's Gigabitstrategie 2025, and France's Très Haut Débit initiative, that are systematically derisking private infrastructure investment.

Investments in the Europe data center is also surging, driven by AI workloads and digital sovereignty imperatives, further reinforcing fiber procurement across the region through the forecast period.

Germany Fiber Optics Market Size

Germany accounts for approximately 20% of European fiber optics revenue, yet it remains one of the region's largest infrastructure modernization opportunities given that historically less than 30% of German homes had fiber access as recently as 2022. The Gigabitstrategie 2025 has dramatically accelerated deployment timelines, with estimates projecting that nearly half of all German homes will be passed with fiber by end of 2024. As the EU's largest economy, Germany's accelerating fiber adoption trajectory signals a multi-year equipment and cable procurement cycle of significant scale.

U.K. Fiber Optics Market Size

The United Kingdom contributes approximately 17% of European fiber optics revenue, with 61% of UK properties now passed by full-fiber networks as of 2023. The UK government has set a target of at least 85% gigabit coverage by 2025 and nationwide coverage thereafter, with over 100 broadband providers collectively committing over £40 billion to gigabit-capable infrastructure. Project Gigabit, backed by £5 billion in public funding, focuses on connecting rural premises, ensuring that the UK remains one of Europe's most dynamic fiber deployment markets through 2033.

France Fiber Optics Market Size

France accounts for roughly 14% of European fiber optics revenue and has achieved some of the continent's highest FTTH penetration rates, with the Très Haut Débit national plan targeting universal very-high-speed broadband access. Around 90% of French households are now eligible for fiber connections, and the country is transitioning from deployment to the adoption-acceleration phase. Growing enterprise and public-sector demand, coupled with the continued rollout of 5G backhaul infrastructure and suburban FTTH densification, will sustain healthy fiber cable demand in France through the forecast period.

Asia Pacific Fiber Optics Market Trends and Insights

Asia Pacific commands approximately 40% of global fiber optics market volume in 2025, driven by the region's sheer scale of 5G and broadband infrastructure investment and a mature domestic manufacturing ecosystem. China remains the dominant force, accounting for the world's largest fiber production capacity, exceeding 250 million fiber-kilometers annually, and is supported by national programs such as Broadband China.

China and India together accounted for 45% of all new global fiber deployments in 2023, setting a baseline of sustained high-volume procurement. Asia Pacific is the fastest growing market propelled by urbanization trends, expanding FTTH programs, and aggressive government investment in smart city infrastructure, making the region an essential commercial priority for fiber optics manufacturers seeking to scale globally.

India Fiber Optics Market Size

India represents approximately 14% of Asia Pacific fiber optics revenue and is one of the world's highest-growth markets, anchored by the BharatNet program targeting 600,000 gram panchayats and backed by government investment exceeding US$ 13 billion. STL (Sterlite Technologies Limited) was awarded a multi-year contract valued at approximately INR1,800 crore in April 2025 to deploy 64,000 km of optical fiber across Telangana. India's 5G rollout, among the fastest in the world by subscriber adoption speed, is creating simultaneous demand for both metro-area and backhaul fiber, supporting a robust procurement outlook through 2033.

Japan Fiber Optics Market Size

Japan contributes approximately 11% of Asia Pacific fiber optics revenue, underpinned by one of the world's highest fixed broadband penetration rates and a sophisticated telecom infrastructure ecosystem anchored by carriers such as NTT and SoftBank. Japan's IOWN (Innovative Optical and Wireless Network) Forum is driving next-generation optical infrastructure investment, with a Vision 2030 White Paper outlining advanced optical networking as a national technology priority. Japan is also a leading innovator in specialty optical fiber, with companies such as Fujikura and Sumitomo Electric maintaining globally competitive positions in high-performance fiber segments.

Southeast Asia Fiber Optics Market Size

Southeast Asia accounts for approximately 8% of Asia Pacific fiber optics revenue and represents one of the fastest-growing sub-regional markets, driven by rapid urbanization, surging mobile data consumption, and active government broadband programs across Vietnam, Indonesia, Thailand, and Philippines. Vietnam emerged as the leading buyer of fiber optics in 2024 by import volume, reflecting aggressive national broadband expansion. The region's combination of young population demographics, increasing smartphone penetration, and ASEAN Digital Masterplan 2025 policy framework positions Southeast Asia as a high-priority emerging market for fiber cable manufacturers seeking volume growth outside China through 2033.

Competitive Landscape

The global fiber optics market exhibits a moderately consolidated structure at the high-value end, where large integrated players dominate through scale, vertical integration, and strong control over the value chain from preform manufacturing to cable assembly. In contrast, the lower and mid-tier segments remain fragmented, populated by regional suppliers and niche manufacturers competing primarily on price and localized demand.

Competitive strategies are increasingly shaped by supply chain security and long-term demand visibility. Integrated participants are strengthening their positions through capacity expansion, strategic acquisitions, and long-term supply agreements with hyperscale cloud providers and public infrastructure programs. Technological leadership through R&D and product innovation in high-capacity and subsea solutions remains a key differentiator. Meanwhile, cost-focused competitors, particularly from Asia, are expanding aggressively in price-sensitive and emerging markets.

A growing trend is the shift toward partnership-led business models, including public-private collaborations, open-access network infrastructure, and Build-Operate-Transfer structures, reflecting the increasing role of governments and digital ecosystem players in driving demand.

Key Developments

- March, 2026: Legrand announced the launch of its color-indexed hyper-density fiber solution for AI data centers, designed to simplify deployment and management of ultra-dense fiber networks by improving installation speed, reducing complexity, and supporting high-capacity 800G-plus AI-driven infrastructure.

- March, 2026: Corning Incorporated announced at OFC 2026 its new AI-focused innovations in fiber, cable, and connectivity, aimed at enabling higher-density optical networks, faster deployment, and scalable infrastructure for hyperscale data centers and next-generation AI-driven communication systems.

- March 2025: Corning Incorporated launched GlassWorks AI™ solutions targeting AI data center applications, including the Contour™ Flow Cable that doubles fiber capacity within existing conduit diameters, directly responding to hyperscaler infrastructure demands.

Fiber Optics Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 4.9 Billion |

| Current Market Value (2026) | US$ 8.4 Billion |

| Projected Market Value (2033) | US$ 16.9 Billion |

| CAGR (2026 - 2033) | 10.5% |

| Leading Region | North America, 38% market share (2025) |

| Dominant Fiber Type | Glass Optical Fiber - Single Mode, 52% share (2025) |

| Top-Ranking Industry | IT & Telecom, 43% share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 8.5 Billion |

Companies Covered in Fiber Optics Market

- AFL

- Birla Furukawa Fiber Optics Limited

- Corning Incorporated

- Finolex Cables Limited

- Molex, LLC

- OFS Fitel, LLC

- Optical Cable Corporation (OCC)

- Prysmian Group

- Sterlite Technologies Limited (STL)

- Yangtze Optical Fiber and Cable Joint Stock Limited Company (YOFC)

- Sumitomo Electric Industries, Ltd.

- Fujikura Ltd.

- CommScope Holding Company, Inc.

- Hengtong Optic-Electric Co., Ltd.

- Furukawa Electric Co., Ltd.

- FiberHome Technologies

Frequently Asked Questions

The global Fiber Optics market is valued at US$ 8.4 billion in 2026 and is expected to reach US$ 16.9 billion by 2033, growing at a CAGR of 10.5%.

The primary driver is large-scale 5G network rollout supported by fiber backhaul expansion and government broadband funding programs.

North America leads the market with about 38% share in 2025, driven by broadband investments, 5G expansion, and AI data center growth.

The key opportunity lies in AI-driven hyperscale data centers requiring high-density, high-performance fiber solutions.

Key players include major global and regional manufacturers such as Corning, Prysmian, Sterlite Technologies, YOFC, OFS Fitel, AFL, Sumitomo Electric, Fujikura, Finolex Cables, OCC, CommScope, Hengtong, and Birla Furukawa Fiber Optics.