- Agrochemicals

- Fermentation Chemicals Market

Fermentation Chemicals Market Size, Share, and Growth Forecast 2026 - 2033

Fermentation Chemicals Market by Product Type (Alcohols, Enzymes, Organic Acids, Others), Application (Industrial, Food and Beverage, Pharmaceutical and Nutritional, Plastics & Fibers, Other), and Regional Analysis for 2026 - 2033

Fermentation Chemicals Market Size and Trend Analysis

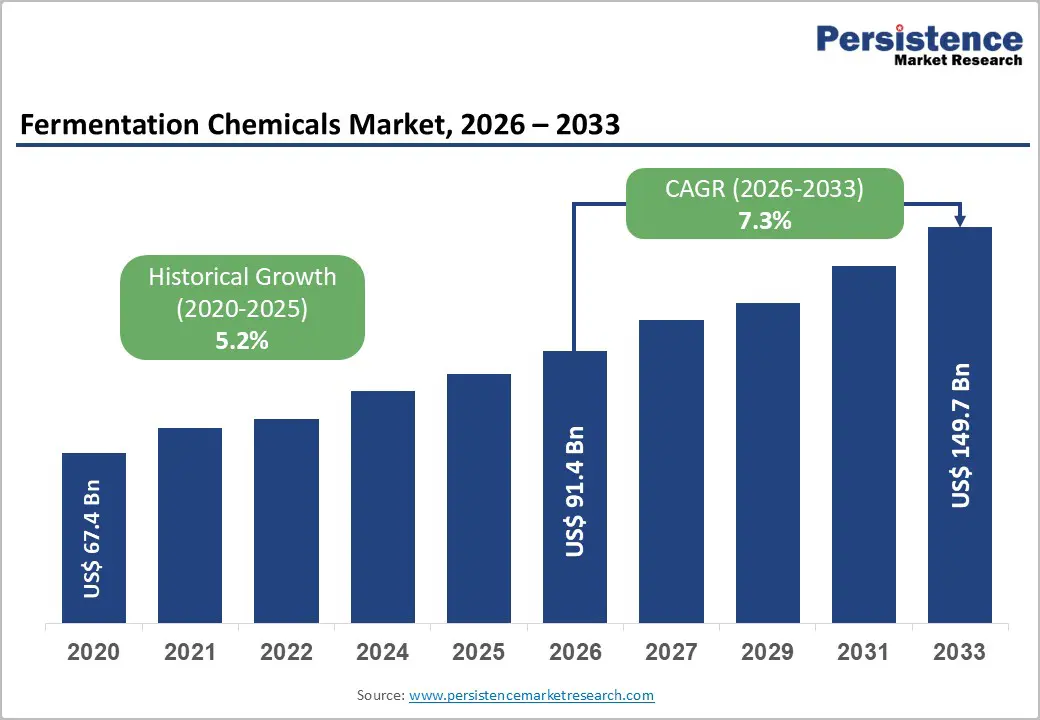

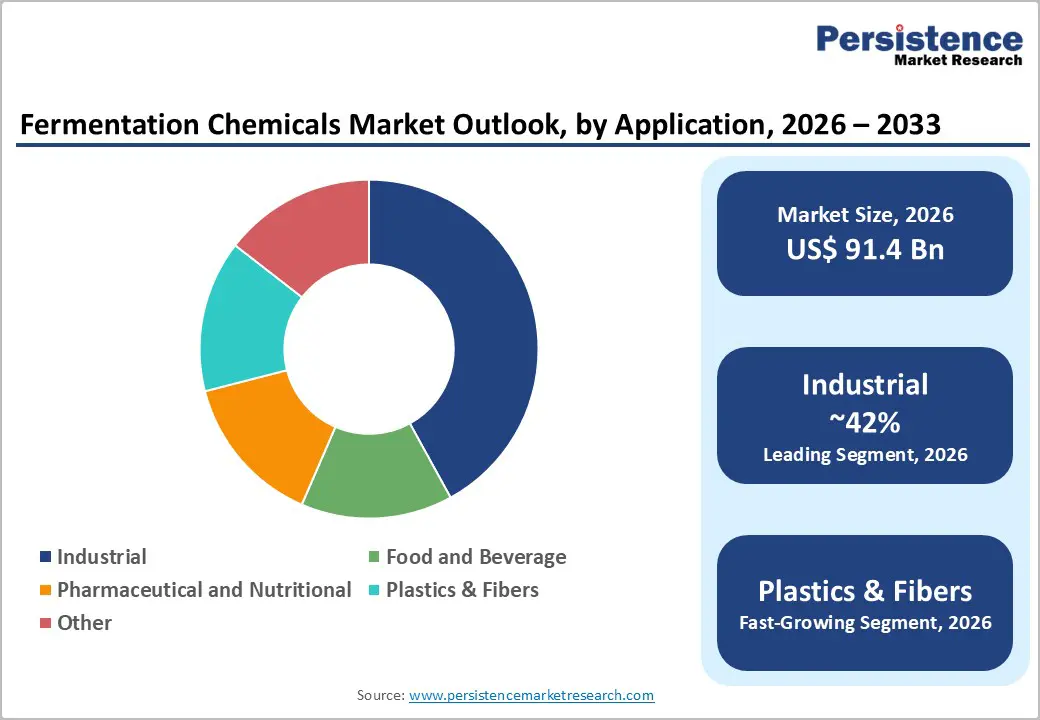

The global Fermentation Chemicals market size is valued at US$ 91.4 Bn in 2026 and is projected to reach US$ 149.7 Bn by 2033, growing at a CAGR of 7.3% between 2026 and 2033.

The market is being propelled by a confluence of powerful structural forces: rising global demand for bio-based and sustainable chemicals, the expanding pharmaceutical and food & beverage sectors, and rapid technological advancements in fermentation bioprocesses. Governments across North America, Europe, and the Asia Pacific are increasingly incentivizing the shift from petroleum-derived chemicals to renewable bio-based alternatives, directly benefiting fermentation chemical producers. Additionally, growing consumer awareness of clean-label and naturally sourced products is generating sustained demand across industrial, nutritional, and pharmaceutical end-use segments.

Key Industry Highlights:

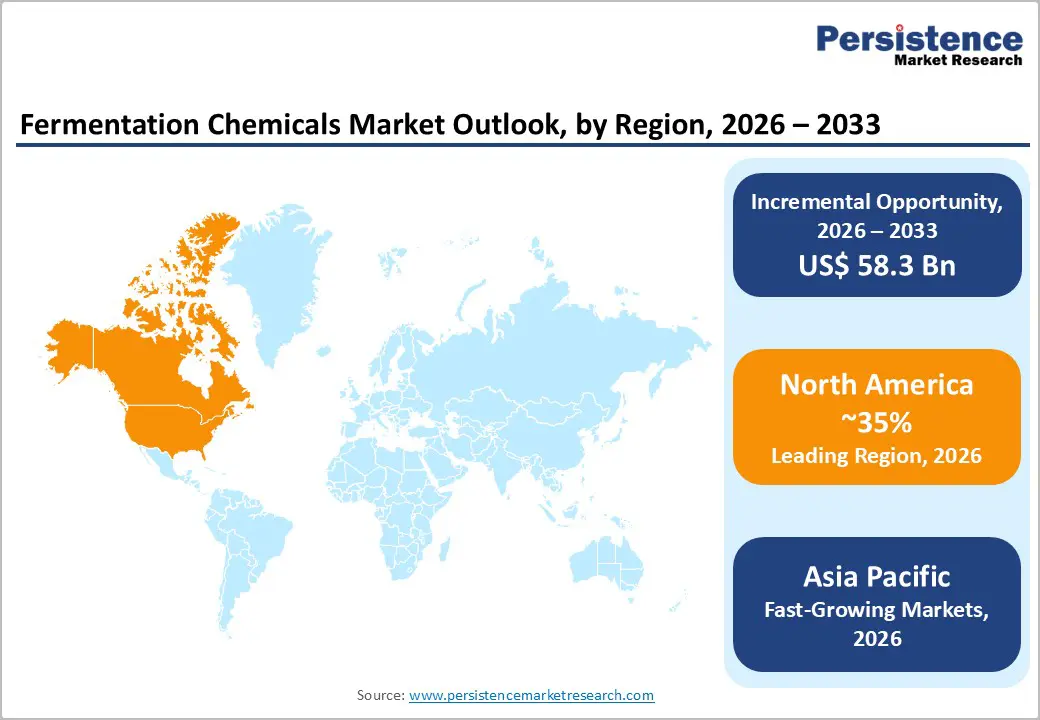

- Leading Region: North America leads the global fermentation chemicals market, driven by its dominant pharmaceutical industry, strong biofuel mandates, and extensive R&D ecosystem, accounting for approximately 35% of global revenues.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, projected to expand at approximately 6.5% CAGR through 2033, fueled by expanding pharmaceutical, food & beverage, and bioplastics sectors in China, India, and ASEAN countries.

- Dominant Segment: The Alcohols product type segment dominates the market with approximately 53% share, primarily driven by large-scale ethanol demand in biofuels, pharmaceuticals, and industrial solvent applications across global markets.

- Fastest Growing Segment: The Plastics & Fibers application segment registers the fastest growth rate at approximately 7.8% CAGR, propelled by surging demand for fermentation-derived lactic acid for PLA bioplastics production under global regulatory anti-plastics mandates.

- Key Market Opportunity: Precision fermentation technology represents the most significant near-term opportunity, enabling production of high-value specialty chemicals, biosurfactants, and pharmaceutical actives at competitive economics, attracting substantial venture and strategic investment in 2024–2025.

| Key Insights | Details |

|---|---|

|

Fermentation Chemicals Market Size (2026E) |

US$ 91.4 Bn |

|

Market Value Forecast (2033F) |

US$ 149.7 Bn |

|

Projected Growth CAGR (2026–2033) |

7.3% |

|

Historical Market Growth (2020–2025) |

5.2% |

Market Dynamics

Drivers - Rising Demand for Bio-Based Chemicals and Sustainability-Driven Industrial Transition

The global industrial sector is undergoing a decisive transition away from petrochemical-based inputs toward bio-derived alternatives, placing fermentation chemicals at the center of the green chemistry revolution. Regulatory frameworks such as the European Union's Green Deal and the U.S. Renewable Fuel Standard (RFS) mandate significant reductions in fossil fuel dependency, driving manufacturers to adopt fermentation-derived alcohols, organic acids, and specialty enzymes.

According to the U.S. Department of Energy, the bioeconomy contributes over US$ 400 billion annually to the U.S. economy, with bio-based chemicals occupying a rapidly growing share. Fermentation-derived ethanol, lactic acid, and succinic acid are increasingly used in biofuels, bioplastics, and solvents, substituting petroleum-derived counterparts. Furthermore, heightened environmental awareness among industrial buyers and tightening EPA emission norms are accelerating the adoption of fermentation chemicals across plastics, textiles, and chemical manufacturing sectors worldwide.

Expanding Pharmaceutical and Nutritional Sector Fueling Demand for Market

The pharmaceutical industry is one of the fastest-growing end-use sectors for fermentation chemicals, relying on fermentation processes to produce antibiotics, vitamins, vaccines, amino acids, and biologically active intermediates. The World Health Organization (WHO) projects global cancer cases to rise from 20 million in 2024 to 30 million by 2040, escalating demand for fermentation-based drug molecules and active pharmaceutical ingredients (APIs). According to AstraZeneca, the United States pharmaceutical spending is projected to be between US$ 605–635 billion in 2024, underscoring the strength of this end-use market.

In the nutritional space, the U.S. Centers for Disease Control and Prevention (CDC) reports over 38 million Americans suffering from diabetes in 2024, with fermented food-based diets increasingly linked to reduced risks of non-communicable diseases. This dual demand for pharmaceuticals and nutrition underscores the critical role of fermentation chemicals as high-value platform compounds.

Restraints - High Production Costs and Complexity of Fermentation Manufacturing Processes

Despite broad application potential, the commercial scalability of fermentation chemicals is constrained by elevated production costs arising from complex upstream and downstream bioprocessing requirements. Maintaining sterile bioreactor environments, optimizing microbial strain performance, and executing energy-intensive separation and purification steps contribute to cost structures that are significantly higher than those of conventional synthetic chemical manufacturing.

The high cost of lactic acid fermentation, for instance, has historically restricted its broader adoption in dairy applications. These cost barriers particularly disadvantage smaller market participants and inhibit penetration into price-sensitive commodity segments, thereby limiting the overall addressable market for fermentation chemicals in certain geographies and sectors.

Feedstock Availability and Price Volatility of Agricultural Raw Materials

Fermentation chemicals predominantly rely on agricultural feedstocks such as sugarcane, corn, wheat, and starch, making the market highly susceptible to supply disruptions and commodity price fluctuations. Climate-related agricultural shocks, geopolitical trade disruptions, and competition for feedstocks from the food and biofuel sectors can create significant volatility in input costs.

The Food and Agriculture Organization (FAO) has repeatedly flagged the vulnerability of agro-industrial supply chains to climate events, with cereal price volatility directly impacting fermentation economics. Such feedstock dependency can compress margins for fermentation chemical producers and deter investment in capacity expansions, particularly in emerging markets where supply chain reliability is limited.

Opportunities - Precision Fermentation and Synthetic Biology Opening High-Value Chemical Niches

The rapid advancement of precision fermentation technologies, which leverage genetically engineered microorganisms to produce complex, high-purity molecules, is creating transformative opportunities for fermentation chemical manufacturers. Precision fermentation enables cost-efficient production of specialty enzymes, rare amino acids, biosurfactants, and pharmaceutical excipients that were previously economically unviable.

In March 2025, biotech firm Liberation Labs secured US$ 50.5 million to build a large-scale precision fermentation facility in Richmond, Indiana, with a planned capacity of 600,000 liters. Similarly, Genomatica raised US$ 75 million in Q1 2025 to commercialize fermentation-derived chemicals for plastics and personal care. As scale-up economics improve and microbial strain intellectual property matures, precision fermentation is poised to unlock high-margin specialty chemical niches across pharma, cosmetics, and advanced materials sectors.

Bioplastics and Sustainable Plastics Boom Creating Demand for Organic Acids from Fermentation

The increasing global emphasis on biodegradable and compostable packaging solutions is driving strong demand for fermentation-derived polylactic acid (PLA) and its key precursor, lactic acid. Regulatory initiatives such as the European Union Plastics Strategy, alongside comparable frameworks in Japan, South Korea, and India, mandate reductions in single-use plastics, thereby redirecting investments toward bio-based polymer alternatives.

In parallel, Corbion N.V. commissioned a new lactic acid production facility in Thailand in 2024, utilizing circular manufacturing technology, reflecting substantial capacity expansion in this segment. As a result of these structural drivers, the plastics and fibers application segment is projected to grow at a compound annual growth rate exceeding 7.8% over the forecast period, positioning it among the fastest-growing demand areas for fermentation chemicals.

Category-wise Analysis

Product Type Insights

The Alcohols segment commands the leading share, approximately 53%, of the global fermentation chemicals market, underpinned by its extensive range of industrial, pharmaceutical, and energy applications. Ethanol, the dominant product within this segment, serves as a critical raw material in alcoholic beverages, biofuels, sanitizers, pharmaceutical tinctures, and industrial solvents. The global biofuel push, driven by mandates such as the U.S. Renewable Fuel Standard and the EU's RED II Directive, has substantially increased bioethanol demand, particularly as a fuel additive reducing vehicular carbon emissions.

Methanol derived via fermentation pathways is also gaining traction as an industrial solvent and chemical intermediate. In emerging economies with rapidly growing middle-class populations, rising demand for premium alcoholic beverages is further supporting volume growth. The alcohol segment benefits from relatively cost-effective fermentation pathways using sugarcane, corn, and starch feedstocks, enabling competitive large-scale production across multiple geographies.

Application Insights

The Industrial application segment holds the largest market share, accounting for approximately 42% of total fermentation chemicals consumption, driven by the extensive utilization of fermentation-derived products in biofuels, specialty chemical manufacturing, agriculture, and textiles. The industrial segment's dominance is anchored in the large-scale demand for ethanol as a biofuel blending component and fermentation-derived organic acids as platform chemicals for polymer and solvent production.

Furthermore, fermentation-derived enzymes find critical industrial applications in paper and pulp processing, textile de-sizing, and detergent formulation, supporting broad-based demand. The segment's trajectory is further supported by rising institutional procurement of bio-based industrial chemicals across North America and Europe, aligned with regulatory decarbonization mandates issued by bodies such as the U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA).

Regional Insights

North America Fermentation Chemicals Market Trends

North America remains the leading regional market for fermentation chemicals, accounting for approximately 35% of global revenue in 2025. The region’s dominant position is supported by its well-established pharmaceutical and biotechnology industries, extensive biofuel production infrastructure, and regulatory frameworks that actively promote the adoption of bio-based chemicals. The United States is projected to remain the world’s largest pharmaceutical market, thereby sustaining strong demand for fermentation-derived active pharmaceutical ingredients and enzymes.

Ongoing geopolitical uncertainties, including U.S.–Iran tensions, have further accelerated efforts to strengthen domestic bio-based chemical manufacturing as part of broader supply chain risk-mitigation strategies. Investment momentum continues across the region, with significant funding allocated to precision fermentation facilities, government-backed biomanufacturing initiatives, and expanding fermentation applications in Canada and Mexico’s growing food and beverage sector.

Europe Fermentation Chemicals Market Trends

Europe represents the second-largest regional market for fermentation chemicals, with growth strongly supported by the EU Green Deal and the Chemicals Strategy for Sustainability (CSS), which together establish a favorable regulatory framework for bio-based, fermentation-derived chemicals as alternatives to petroleum-based products. Germany leads regional production, supported by the presence of established chemical majors such as BASF SE and Evonik Industries AG, both of which have made significant investments in fermentation and biosurfactant technologies.

The U.K. and France exhibit robust demand from pharmaceutical and functional food industries, while Spain is emerging as an important production hub following Corbion’s relocation of selected fermentation operations in 2024. Geopolitical pressures, including U.S.–Iran tensions and broader Middle Eastern instability, have intensified Europe’s strategic emphasis on domestic bio-based chemical self-sufficiency. Regulatory harmonization efforts and recent capacity expansions, such as Lonza’s investment in Switzerland, continue to strengthen the region’s fermentation manufacturing capabilities.

Asia Pacific Fermentation Chemicals Market Trends

Asia Pacific represents the fastest-growing regional market for fermentation chemicals, with a projected CAGR of approximately 6.5% over the forecast period. China accounts for the largest share within the region, supported by its extensive manufacturing base, cost-competitive labor environment, and expanding pharmaceutical and food processing industries. Japan remains a global leader in enzyme and amino acid fermentation, driven by sustained innovation from established players such as Ajinomoto Co., Inc.

India is witnessing accelerating demand, driven by the rapid growth of food and beverage start-ups and by companies such as Biocon expanding their biopharmaceutical fermentation capacities. Additionally, Southeast Asian economies, particularly Thailand and Indonesia, are attracting increased investment due to abundant agricultural feedstocks and supportive policy frameworks. Ongoing global supply chain diversification trends are further strengthening the Asia Pacific’s position in the bio-based chemicals landscape.

Competitive Landscape

The global fermentation chemicals market is characterized by a fragmented and partially consolidated competitive structure, with the top players, including BASF SE, Novonesis, Cargill, and Evonik Industries AG, collectively accounting for less than 20% of the global market share. Competition is increasingly shifting from price-based differentiation toward technological leadership, sustainability credentials, and application-specific biosolution capabilities. Market leaders are investing heavily in bioprocess intensification, microbial strain IP development, and downstream purification technologies. Strategic mergers, such as the Novozymes–Chr. Hansen merger, creating Novonesis in 2024, is consolidating R&D pipelines and broadening product portfolios. Emerging business models emphasizing contract fermentation, precision fermentation-as-a-service, and integrated bio-based value chains are reshaping competitive dynamics across the sector.

Key Developments:

- October 2025: BASF Aroma Ingredients' biotechnology brand, Isobionics®, launched a new natural product on the flavor market. Isobionics® Natural alpha-Farnesene 95 is the latest addition to the company's natural flavor ingredient portfolio for lime applications. Like all Isobionics® products, Isobionics® Natural alpha-Farnesene 95 is fermentation-based and produced from renewable resources.

- January 2024: Novozymes and Chr. Hansen Holding A/S completed its landmark merger to form Novonesis, creating a global biosolutions leader with combined fermentation capabilities spanning food, agriculture, health, and industrial applications.

- February 2024: TotalEnergies Corbion announced a strategic collaboration with Bluepha, a leading Chinese synthetic biology company, to develop sustainable fiber solutions using Luminy PLA and Bluepha PHA.

Top Companies in the Fermentation Chemicals Market

BASF SE (Ludwigshafen, Germany) is a global leader in chemical manufacturing with a comprehensive fermentation chemicals portfolio spanning enzymes, organic acids, alcohols, and bio-based specialty chemicals. In October 2023, BASF announced plans to build a new fermentation plant at its Ludwigshafen site for biological crop protection products. Its extensive R&D infrastructure and integrated value chain give BASF strong competitive positioning in both industrial and pharmaceutical fermentation segments globally.

Novonesis (Bagsvaerd, Denmark), formed by the merger of Novozymes A/S and Chr. Hansen Holding A/S, in early 2024, Novonesis is the world's largest dedicated biosolutions company. The company reported net sales of €4.157 billion (US$ 4.9 billion) in 2025, with 7% organic growth and an adjusted EBITDA margin of 37.1%. Its precision fermentation platform and enzyme innovation capabilities make it the industry's most influential technology provider.

Cargill, Inc. (Minneapolis, U.S.) combines a dominant global agricultural sourcing network with deep fermentation expertise to produce bio-based organic acids, ethanol, and specialty food ingredients. The company announced the expansion of its fermentation-based bioindustrial platform in September 2023 to boost sustainable chemical production. Cargill's vertically integrated feedstock-to-product model, spanning 70+ countries, provides a distinctive competitive advantage in feedstock cost management and production scalability.

Companies Covered in Fermentation Chemicals Market

- BASF SE

- Novonesis

- Cargill, Inc.

- Evonik Industries AG

- AB Enzymes

- Chr. Hansen Holding A/S

- Ajinomoto Co., Inc.

- ADM

- Biocon

- Lonza

- Dow Inc.

- Corbion N.V.

Frequently Asked Questions

The global Fermentation Chemicals market is valued at US$ 91.4 Bn in 2026 and is projected to reach US$ 149.7 Bn by 2033, growing at a CAGR of 7.3% during the forecast period 2026–2033.

The market's growth is primarily driven by the global industrial shift from petroleum-derived chemicals to bio-based alternatives, strong regulatory mandates such as the EU Green Deal and U.S. Renewable Fuel Standard, expanding pharmaceutical demand for fermentation-derived APIs and enzymes, and rising consumer preference for natural and clean-label food ingredients.

The Alcohols segment leads the Fermentation Chemicals market with approximately 53% share, driven by large-scale global demand for bioethanol in biofuels, pharmaceutical solvents, and alcoholic beverages. Ethanol's role as a strategic bio-based fuel additive under emission-reduction mandates globally reinforces this segment's dominant position.

North America is the leading regional market for fermentation chemicals, accounting for approximately 35% of global revenues. The region's dominance is attributed to its world-leading pharmaceutical industry, robust biofuel infrastructure, and strong innovation ecosystem backed by companies such as ADM, Cargill, and Dow Inc.

Precision fermentation technology represents the most significant near-term growth opportunity, enabling cost-efficient production of high-value specialty molecules, including biosurfactants, specialty enzymes, and pharmaceutical actives. Scaling precision fermentation for bioplastics precursors such as lactic acid for PLA production also offers substantial revenue potential given regulatory tailwinds against single-use plastics globally.