- Bulk Chemicals

- Drilling and Completion Fluids Market

Drilling and Completion Fluids Market Size, Share, and Growth Forecast 2026 - 2033

Drilling and Completion Fluids Market by Fluid Type (Water-Based Fluids, Oil-Based Fluids, Synthetic-Based Fluids, Pneumatic Fluids, Foam-Based Fluids), by Well Type (Conventional Wells, Horizontal Wells, Directional Wells, Deepwater Wells, Ultra-Deepwater Wells), Application (Drilling Fluids, Completion Fluids, Workover & Repair Fluids, Stimulation Fluids), End-user (Onshore, Offshore), and Regional Analysis, 2026 - 2033

Drilling and Completion Fluids Market Size and Trend Analysis

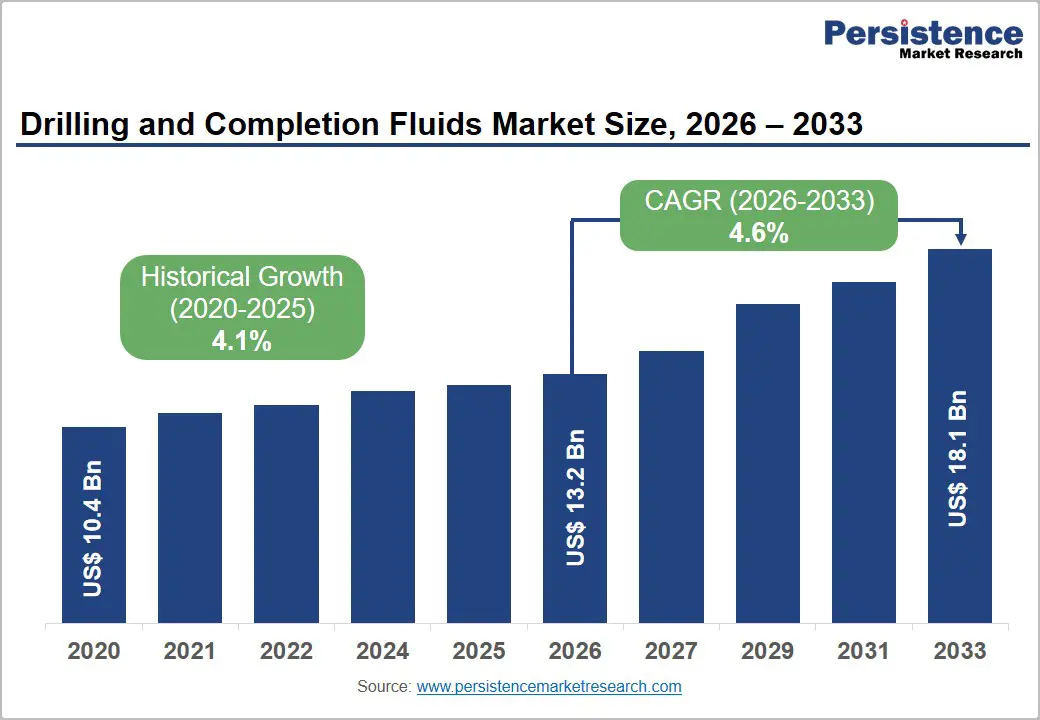

The global drilling and completion fluids market size is expected to be valued at US$ 13.2 billion in 2026 and projected to reach US$ 18.1 billion, growing at a CAGR of 4.6% between 2026 and 2033.

Resurgent upstream capital expenditure and the structural shift toward complex well architectures are reshaping demand for advanced fluid chemistries. The International Energy Agency (IEA) reported that global upstream oil and gas investment exceeded US$ 570 billion in 2024, the highest level in a decade. Horizontal and deepwater drilling, both fluid-intensive operations, now account for the majority of new well starts globally, lifting per-well consumption and rewarding suppliers with high-performance synthetic and water-based fluid portfolios.

Key Industry Highlights:

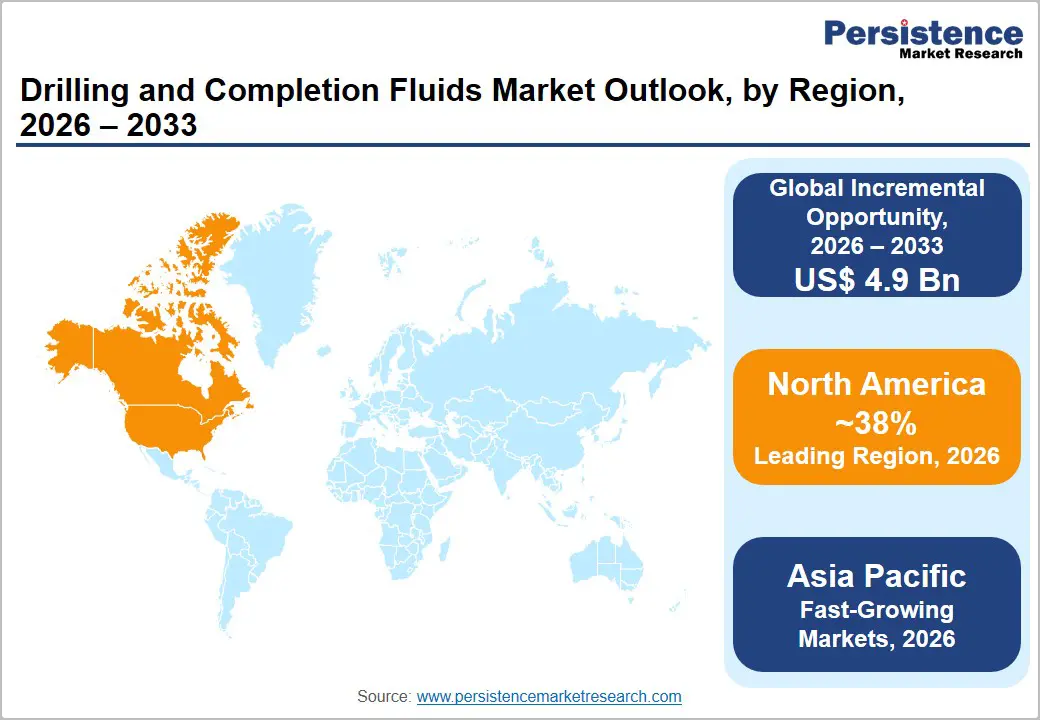

- Leading Region: North America leads with approximately 38% share in 2026, anchored by U.S. shale dominance, mature service ecosystems, and high fluid intensity per horizontal well across major unconventional plays.

- Fastest Growing Region: Asia Pacific is the fast-growing market at a projected CAGR of approximately 5.5%, driven by China's unconventional gas push and India's offshore exploration acceleration.

- Dominant Fluid Type: Water-based fluids (WBF) dominate the fluid type category with approximately 52% share in 2026, supported by cost advantages and broad regulatory acceptance across onshore basins worldwide.

- Fastest Growing Well Type: Ultra-deepwater wells represent the fast-growing well-type segment at a CAGR of approximately 6.2%, propelled by sanctioned Guyana, Brazil, Suriname, and Namibia offshore developments.

- Key Opportunity: Bio-based, low-toxicity fluid systems offer a high-margin opportunity as ESG procurement screens harden across European and offshore operators, rewarding early movers with multi-well contracts.

Market Dynamics

Drivers - Expansion of Unconventional and Horizontal Drilling Activity Anchors Volume Demand

For fluid suppliers, the structural shift from vertical to horizontal and unconventional drilling represents the most durable volume tailwind in this market. Horizontal wells consume two to four times the fluid volume of conventional vertical wells because of longer lateral lengths and the elevated need for hole cleaning and pressure control. The U.S. Energy Information Administration (EIA) reports that horizontal wells accounted for more than 96% of new oil and gas wells drilled in the Permian Basin in 2024, while average lateral lengths in U.S. shale plays exceeded 10,500 feet in 2024, up from roughly 7,500 feet in 2018. This translates directly into higher fluid intensity per well, sustained service contract values, and stronger pricing leverage for suppliers offering performance-engineered water-based and synthetic systems.

Rising Deepwater and Offshore Exploration & Production Investment Drives Premium Fluid Demand

Operators returning to deepwater plays are pulling suppliers up the value chain toward premium synthetic-based and high-density completion fluid systems, where margins are materially higher than legacy water-based mud. Rystad Energy estimates global offshore upstream investment crossed US$ 200 billion in 2024, with sanctioned deepwater projects reaching their highest level since 2013.

Pre-salt activity offshore Brazil, expansion offshore Guyana, and Saudi Aramco's Jafurah unconventional gas program, a US$ 100 billion investment commitment through 2030, collectively underpin a multi-year demand pipeline. For chemistry-driven suppliers, this signals a structural shift in revenue mix toward higher-margin proprietary systems and integrated fluids management services. This dynamic is reinforced by broader oilfield chemicals demand, where specialty molecules command premium pricing in challenging downhole environments.

Restraints - Tightening Environmental Regulations and Waste Disposal Costs Compress Margins

For operators and service providers, environmental compliance has become a significant cost line, particularly in offshore basins where regulators have hardened discharge rules. The U.S. Environmental Protection Agency (EPA) Effluent Limitation Guidelines and OSPAR Commission standards in the North Sea restrict overboard discharge of oil-based fluid cuttings, forcing operators to either transport cuttings onshore for treatment at costs that can exceed US$ 200 per metric ton or invest in costlier synthetic alternatives.

The European Chemicals Agency (ECHA) continues to tighten REACH classifications for several drilling additives, narrowing the formulation toolbox and increasing reformulation costs for suppliers. The net effect is sustained margin pressure on legacy oil-based fluid product lines and a higher hurdle rate for new entrants without verifiable sustainable chemistry credentials.

Oil Price Volatility and Capital Discipline Cap Cyclical Upside

The industry's structural shift toward shareholder returns over reinvestment means even periods of elevated oil prices no longer translate proportionally into rig count expansion, a friction that fluid suppliers cannot model away. According to Baker Hughes, the global rig count averaged approximately 1,750 in 2024, well below the 2014 peak of over 3,600, despite multi-year highs in upstream cash flow. OPEC+ supply discipline keeps benchmark crude prices range-bound, while U.S. shale operators have publicly committed to capital efficiency rather than aggressive volume growth. For fluid suppliers, this caps the upside of a conventional cyclical recovery and forces a strategic pivot toward share-of-wallet expansion, integrated service models, and aftermarket workover-driven demand.

Opportunities - Bio-based and Low-Toxicity Fluid Systems Open a Premium Sustainability Window

Suppliers that move early on verifiable, third-party-certified low-toxicity systems are positioned to lock in long-cycle offshore and arctic contracts where ESG procurement screens are now hard gates rather than soft preferences. Operators including Equinor, Shell, and TotalEnergies have set explicit targets to reduce Scope 3 emissions and chemical hazard profiles across their drilling supply chains, with several major North Sea operators publishing yellow- and green-rated chemical mandates aligned with the OSPAR Harmonised Mandatory Control System (HMCS).

The emerging specialty chemicals demand pool is increasingly favoring suppliers with proprietary bio-polymer thickeners, modified starches, and synthetic ester base fluids. Early movers expanding plant-based viscosifier portfolios are likely to convert pilot programs into multi-well master service agreements as procurement standards harden through 2026-2027. This opens a defensible high-margin niche distinct from commoditized mud chemistry.

Digital Fluid Management and Real-Time Performance Optimization Create High-Value Service Layers

A genuine opportunity exists for suppliers to monetize data and engineering services rather than just barrels of mud, particularly as operators target well-cost reductions on deepwater projects ranging from US$ 8-12 million per well. Real-time fluid property monitoring, automated mud mixing systems, and AI-enabled hydraulics modeling can cut non-productive time by 10-15%, according to operator-published case studies from Petrobras and ADNOC. The shift is time-sensitive because integrated digital offerings, combining downhole sensors, edge analytics, and fluid chemistry expertise, are becoming de facto qualifiers in tender requirements from national oil companies across the Middle East and Latin America.

Suppliers that pair traditional chemistry with platform-based digital deliverables can defend pricing, reduce customer churn, and capture a share of the broader well-construction value pool currently held by larger integrated service providers. This trend complements parallel growth in the enhanced oil recovery (EOR) chemicals ecosystem, where data-driven dosing has become standard practice.

Category-wise Insights

Fluid Type Analysis

Water-based fluids (WBF) lead the category with an estimated share of approximately 52% in 2026. Their dominance is anchored by significantly lower per-barrel cost compared with oil- and synthetic-based systems, broad regulatory acceptance, particularly across onshore U.S., China, and India, where discharge rules favor water-based chemistries, and continual performance improvements through high-performance additives that narrow the technical gap with non-aqueous systems.

According to the U.S. EPA, water-based fluids remain the default approved discharge option in most Gulf of Mexico shelf operations. Synthetic-Based Fluids (SBF) are expected to be the fastest-growing sub-segment at a projected CAGR of approximately 5.6% through 2033, propelled by deepwater expansion where high lubricity, low toxicity, and thermal stability outweigh the cost premium.

Well Type Insights

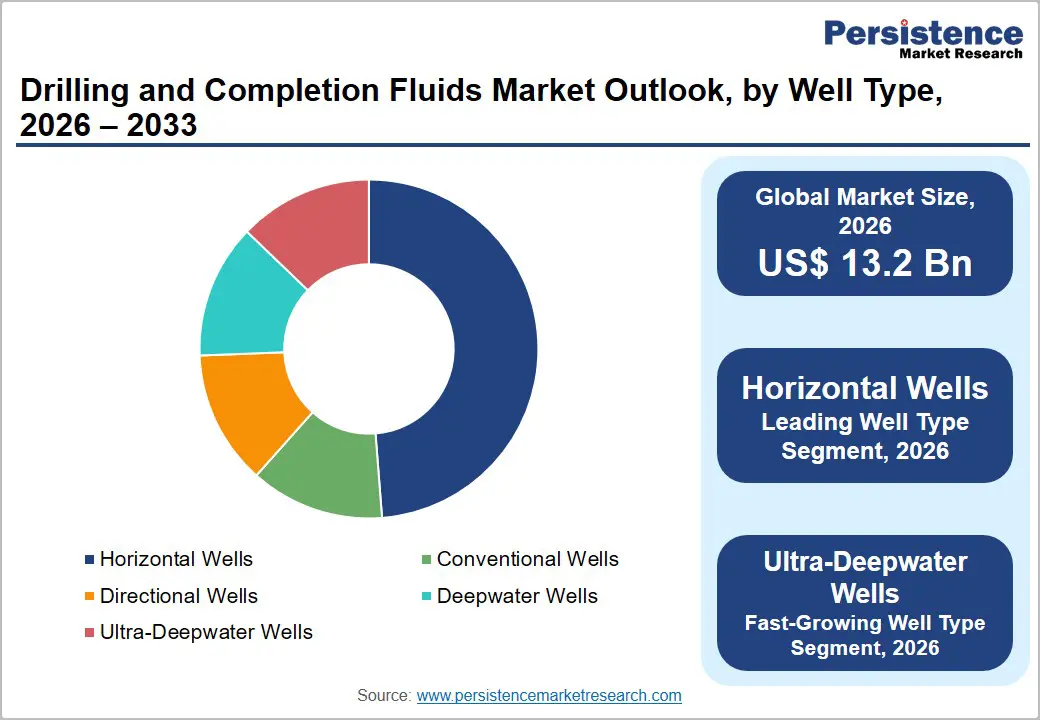

Horizontal wells are likely to lead with an estimated share of approximately 48% in 2026, reflecting the transformation of global drilling activity over the last decade. The EIA confirms horizontal completions dominate U.S. unconventional production, and similar patterns are spreading across Argentina's Vaca Muerta, China's Sichuan Basin, and North Dakota's Bakken play. Higher fluid volumes per well, the need for advanced rheology to clean extended laterals, and operator preference for performance-driven contracts entrench this leadership.

Ultra-Deepwater Wells represent the fastest-growing well-type sub-segment at an expected CAGR of approximately 6.2%, driven by sanctioned projects offshore Guyana, Suriname, Brazil, and Namibia, where well costs and fluid complexity are at their highest.

Application Insights

Drilling fluids are likely to lead the application category with an estimated share of approximately 64% in 2026. The sheer volume intensity of mud systems consumed during the drilling phase, covering hole cleaning, pressure control, wellbore stability, and bit cooling, makes the largest revenue pool across well types. Industry technical disclosures from major operators indicate that fluid systems account for 5-15% of total well construction cost, depending on complexity and depth.

Completion Fluids are projected to be the fastest-growing application sub-segment at a CAGR of approximately 5.2% through 2033, as horizontal completions and multi-stage hydraulic fracturing programs increasingly require specialized clear brines and reservoir-compatible chemistries to protect production zones.

End-user Insights

Onshore operations are likely to lead the end-user category with an estimated share of approximately 66% in 2026. The scale of U.S. shale, Argentina's Vaca Muerta development, China's tight gas programs, and Middle East onshore mega-projects collectively generate the largest absolute well count and corresponding fluid consumption.

The EIA estimates U.S. onshore tight oil production averaged over 8.5 million barrels per day in 2024, underpinning continuous chemical demand. Offshore is the faster-growing end-use at a projected CAGR of approximately 5.4%, as offshore exploration and production recovers from a multi-year underinvestment cycle and pre-salt, deepwater Guyana, and West African projects ramp up sanctioning activity.

Regional Insights

North America Drilling and Completion Fluids Market Trends and Insights

North America leads the global market with an estimated share of approximately 38% in 2026, anchored by sustained shale activity, mature service supply chains, and a dense concentration of fluid chemistry innovators. Use of advanced horizontal drilling techniques, vertically integrated service ecosystems, and proximity to chemical feedstock translate into outsized fluid intensity per rig. Operator capital discipline has shifted demand toward efficiency-enhancing premium chemistries and digital fluid management platforms.

Looking ahead, sustained Permian and Haynesville activity, combined with rising LNG-linked gas drilling, points to continued share leadership through 2033 even as growth rates moderate.

U.S. Drilling and Completion Fluids Market Size

The U.S. is likely to represent an estimated 85% of the North American market in 2026, reflecting its unrivaled position as the world's largest unconventional oil and gas producer. Long lateral drilling, completion intensification, and operator preference for advanced synthetic and high-performance water-based chemistries justify this concentration. The EIA reported U.S. crude oil production averaging over 13.2 million barrels per day in 2024, a record. Looking forward, the U.S. will remain the global pricing benchmark and innovation hub for drilling fluid technology through the forecast period.

Europe Drilling and Completion Fluids Market Trends and Insights

Europe's market is shaped by a stringent regulatory framework, particularly the OSPAR Commission discharge controls and REACH chemical compliance regime, that pushes operators toward premium low-toxicity systems and synthetic-based fluids. North Sea redevelopment, late-life field maintenance, and selective new exploration in the Norwegian Continental Shelf sustain demand despite the region's overall declining well count. Demand intensity per well remains elevated due to mature reservoir complexity and deeper offshore targets.

Going forward, Europe will function more as a high-margin, technology-led market than a volume engine, rewarding suppliers with strong sustainability credentials and integrated digital offerings.

Germany Drilling and Completion Fluids Market Size

Germany is likely to register an estimated 8% share in 2026, supported by limited onshore conventional gas drilling and a strong chemicals industry footprint that supplies additives regionally. Demand is anchored less by drilling activity itself and more by Germany's role as a formulation and additive supply base, with companies such as BASF SE and Evonik Industries AG headquartered domestically. The forward viewpoints to incremental demand from geothermal drilling programs as the country pursues its energy transition objectives.

U.K. Drilling and Completion Fluids Market Size

UK is likely to represent an estimated 22% share of European demand in 2026, driven primarily by North Sea offshore activity, late-life production support, and well intervention work. The North Sea Transition Authority (NSTA) has continued to authorize selective new field developments while emphasizing emissions reduction, sustaining demand for premium synthetic-based fluids. Looking ahead, decommissioning activity and incremental field tie-backs will keep the U.K. market resilient but largely flat in volume terms.

France Drilling and Completion Fluids Market Size

France is likely to account for an estimated 5% share in 2026. Domestic upstream activity is minimal following the country's hydrocarbon production phase-out legislation, but France remains relevant as a base for major service and chemical companies operating across West Africa, the Mediterranean, and the Middle East. Demand is therefore exported rather than consumed locally. Forward growth will be tied to engineered geothermal and carbon storage well construction rather than conventional oil and gas drilling.

Asia Pacific Drilling and Completion Fluids Market Trends and Insights

Asia Pacific is the fastest-growing region at a projected CAGR of approximately 5.5% propelled by national energy security agendas, rising shale and tight gas activity in China, and frontier offshore exploration across India, Indonesia, and Malaysia. China targets significantly increased domestic production through unconventional gas resources, with CNPC and Sinopec scaling horizontal drilling in the Sichuan Basin.

The region's shift from import dependence to indigenous production creates a multi-decade demand corridor. For market participants, Asia Pacific represents the most attractive geography for scaling, but success requires localized formulations, partnerships with national oil companies, and competitive cost positioning.

India Drilling and Completion Fluids Market Size

India is poised to register an estimated 18% share of the Asia Pacific market in 2026, with demand driven by ONGC and Oil India Limited drilling campaigns onshore and offshore in the KG Basin and Mumbai High. The government's stated objective to raise domestic oil and gas output and reduce import dependence by 2030 underpins sustained drilling activity. Looking ahead, India's offshore deepwater push and renewed shale gas exploration will lift demand for premium fluid systems through the forecast period.

Japan Drilling and Completion Fluids Market Size

Japan represents an estimated 4% share of the Asia Pacific demand in 2025. With minimal domestic hydrocarbon resources, consumption is concentrated in geothermal drilling, methane hydrate research wells, and Japanese trading houses' overseas exploration and production operations. JOGMEC-backed methane hydrate pilot programs and renewed geothermal investment provide a niche but rising opportunity. The country's trajectory points to specialized, non-conventional well construction rather than volume oil and gas drilling.

South Korea Drilling and Completion Fluids Market Size

South Korea accounts for an estimated 3% share of Asia Pacific demand in 2026. While domestic upstream activity is limited, recent exploration interest in the East Sea following KNOC's announced offshore prospects has reignited drilling planning. Demand is also supported by Korean shipbuilders and offshore engineering firms exporting drilling services regionally. The forward outlook depends heavily on the commercial outcome of current frontier exploration drilling.

Competitive Landscape

The global drilling and completion fluids market is moderately consolidated, with a small group of large integrated oilfield service providers controlling a significant share of global revenue. Market competition is strongly influenced by the ability to deliver bundled well-construction solutions that combine drilling fluids with cementing, pressure control, wireline, and digital drilling services. This integrated service model creates strong competitive barriers for smaller stand-alone chemical suppliers and strengthens long-term customer relationships with exploration and production companies.

Competitive differentiation is increasingly centered on advanced fluid chemistries designed for unconventional drilling, deepwater exploration, and environmentally sensitive operations. Suppliers are investing heavily in low-toxicity, bio-based, and high-performance synthetic fluid systems that support regulatory compliance and operational efficiency. Digital fluid monitoring platforms, real-time well analytics, and automation technologies are also becoming major strategic priorities across the industry. Companies are further expanding through vertical integration of additive production and strategic acquisitions of specialty chemical and fluid technology firms to strengthen proprietary product portfolios and improve margin performance.

Key Developments:

- November 2025: Chevron Phillips Chemical Company launched NanoSlide drilling fluid technology featuring multiphase lubrication capabilities designed to improve drilling efficiency, reduce torque and drag, and enhance wellbore performance in complex drilling environments.

- October 2024: Halliburton partnered with Singapore’s A*STAR to launch NEX Labs, an advanced well completion technology initiative focused on accelerating digital innovation, sustainable drilling solutions, and next-generation completion system development for the energy sector.

Companies Covered in Drilling and Completion Fluids Market

- BASF SE

- Clariant AG

- Dow Inc.

- Schlumberger Limited (SLB)

- Baker Hughes

- Ashland

- Solenis

- Halliburton

- Huntsman Corporation

- Evonik Industries AG

- Newpark Resources

- Stepan Company

- Syensqo

- Chevron Phillips Chemical Company

- PfP Industries

- Tetra Technologies Inc.

- CES Energy Solutions

- Sinopec Oilfield Service Corporation

Frequently Asked Questions

The global drilling and completion fluids market is valued at US$ 13.2 billion in 2026 and is projected to reach US$ 18.1 billion by 2033, growing at a CAGR of 4.6%.

Growing horizontal and unconventional drilling activity is the primary demand driver for the market.

North America leads the market with around 38% share due to strong shale drilling activity and advanced drilling technologies.

Bio-based and low-toxicity fluid systems represent a major growth opportunity for market participants.

Key players include SLB, Halliburton, Baker Hughes, BASF SE, Clariant AG, and Dow Inc.