- Plastics, Polymers & Resins

- Corrosion-resistant Resin Market

Corrosion-resistant Resin Market Size, Share, and Growth Forecast, 2026 - 2033

Corrosion-resistant Resin Market by Resin Type (Epoxy Resin, Vinyl Ester Resin, Others), Application (Coatings, Composites, Others), End‑use Industry, and Regional Analysis for 2026 - 2033

Corrosion-resistant Resin Market Size and Trends Analysis

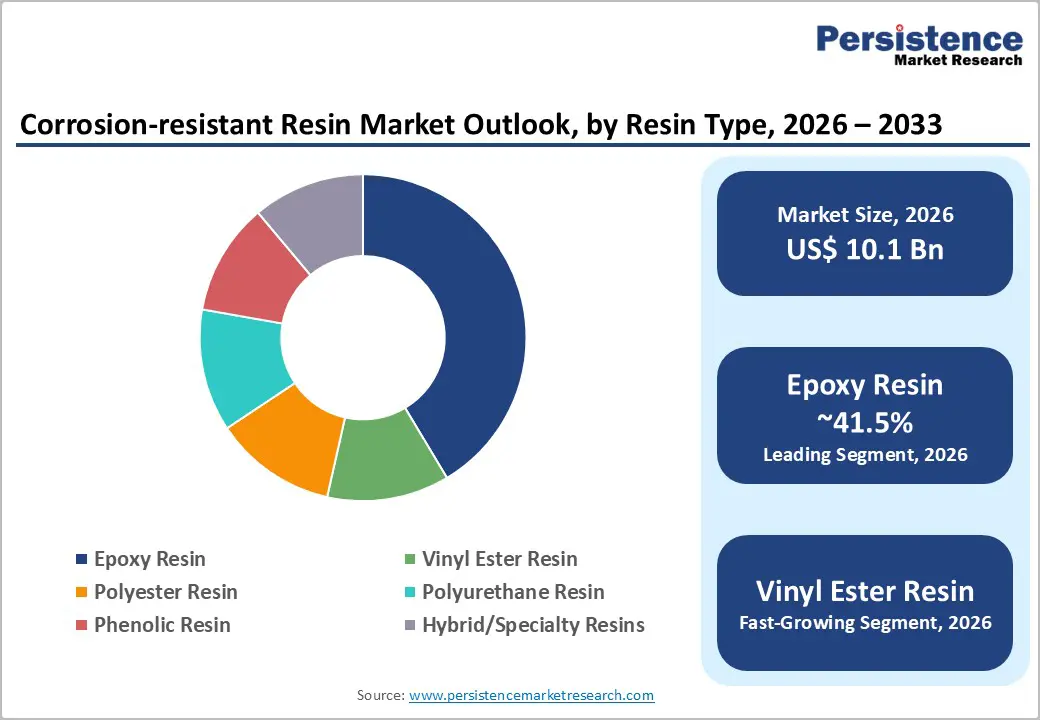

The global corrosion-resistant resin market size is likely to be valued at US$ 10.1 billion in 2026 and is expected to reach US$15.4 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033, driven by infrastructure rehabilitation in oil & gas and chemical processing industries, increasing adoption of corrosion-resistant composites in renewable energy and transportation, and stricter lifecycle and regulatory requirements favoring high-performance materials. Epoxy resins dominate the market due to their superior performance characteristics, while vinyl ester resins are the fastest-growing segment driven by demand in harsh chemical and marine environments. Supply chain volatility and sustainability-focused procurement are reshaping supplier strategies and material innovation.

Key Industry Highlights:

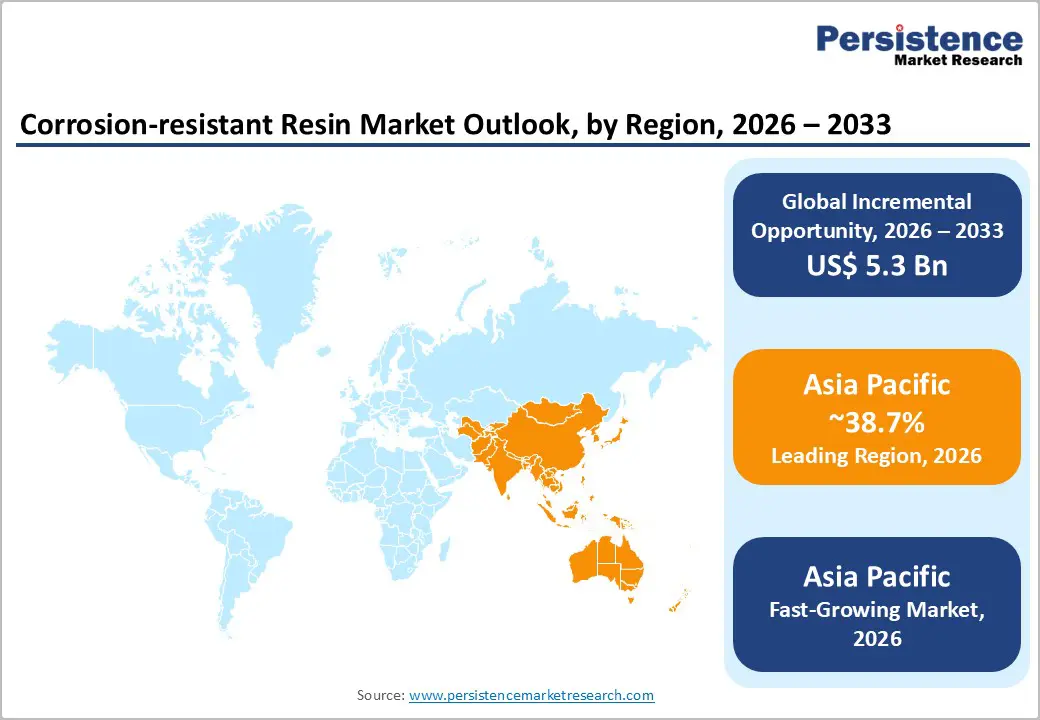

- Leading Region: Asia Pacific is projected to account for approximately 38.7% of the market share, driven by strong industrial growth, infrastructure development, and expanding manufacturing capacity in China and India.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, driven by rapid urbanization, rising investments in chemical processing, and increasing demand for corrosion-resistant materials across the infrastructure and energy sectors.

- Investment Plans: Companies are increasingly investing in localized production facilities, advanced resin formulations, and low-VOC technologies, particularly in the Asia Pacific and North America, to strengthen supply chains and meet evolving regulatory requirements.

- Dominant Resin Type: Epoxy resin is anticipated to hold approximately 41.5% of the market share, due to its superior adhesion, chemical resistance, and widespread use in coatings and structural applications.

- Leading Application: Coatings is estimated to account for around 49.2% of the market share, driven by high demand for protective layers in pipelines, storage tanks, marine structures, and industrial equipment.

| Key Insights | Details |

|---|---|

| Corrosion-resistant Resin Market Size (2026E) | US$10.1 Bn |

| Market Value Forecast (2033F) | US$15.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Infrastructure Renewal and Industrial Capital Expenditure Growth

Aging industrial infrastructure, particularly in developed economies, is driving significant demand for corrosion-resistant resins used in rehabilitation and maintenance. Pipelines, storage tanks, and chemical processing equipment require protective coatings and linings to extend service life and reduce operational costs. Governments and industrial operators are prioritizing refurbishment over replacement due to cost efficiency, creating sustained demand for epoxy and vinyl ester systems. These materials offer high chemical resistance and durability, making them essential for long-term asset protection. As a result, infrastructure modernization projects are increasing the adoption of premium resin formulations, contributing to higher average selling prices and stable revenue growth.

Rising Adoption of Composites in Renewable Energy and Transportation

Corrosion-resistant resins play a critical role in composite materials used in wind energy, automotive, and rail sectors. Wind turbine blades rely heavily on epoxy resins for structural integrity and resistance to environmental degradation. Similarly, the automotive industry is increasingly using lightweight composite materials to improve fuel efficiency and reduce emissions. Vinyl ester resins are gaining traction due to their superior fatigue resistance and chemical stability, particularly in structural applications. The shift toward electrification and renewable energy is accelerating demand for advanced resin systems, creating strong growth opportunities for high-performance materials.

Regulatory Focus on Lifecycle Performance and Sustainability

Regulatory frameworks and procurement standards are increasingly emphasizing lifecycle performance, environmental impact, and sustainability. Industrial buyers are prioritizing materials that reduce maintenance frequency and extend asset life. Corrosion-resistant resins with validated lifecycle performance data are gaining preference in public infrastructure and regulated industries. Manufacturers are investing in low-VOC formulations and environmentally compliant products to meet evolving standards. This shift is encouraging innovation and adoption of advanced resin systems that align with sustainability goals while maintaining high performance.

Barrier Analysis - Volatility in Raw Material Prices and Supply Chain Dependency

The corrosion-resistant resin market is heavily dependent on petrochemical feedstocks such as styrene, epichlorohydrin, and bisphenol-A. Fluctuations in crude oil prices and supply chain disruptions directly impact production costs and pricing stability. Sudden increases in raw material costs can lead to project delays or cancellations, particularly in cost-sensitive markets. Historical trends indicate that resin prices can fluctuate by 5-15% annually during periods of volatility, affecting profitability for both manufacturers and end users.

Processing Complexity and Availability of Skilled Labor

High-performance resins such as vinyl ester and specialty epoxies require precise processing conditions, including controlled temperatures and specialized curing agents. In regions with limited technical expertise, improper application can lead to performance issues, reducing customer confidence. The need for skilled labor and advanced application techniques increases installation costs, particularly in retrofit projects. This creates a barrier to adoption and allows lower-cost alternatives to remain competitive in certain applications.

Opportunity Analysis - Development of Low-VOC and Styrene-Free Resin Systems

Growing environmental concerns and increasingly stringent regulatory restrictions on emissions are accelerating the development and adoption of low-VOC and styrene-free resin systems. These advanced formulations are gaining traction across indoor environments, marine applications, and transportation sectors where emission control and worker safety are critical. Regulatory bodies are tightening permissible exposure limits for volatile compounds, pushing manufacturers to reformulate traditional resin systems without compromising performance. As a result, companies investing in environmentally compliant and sustainable solutions can access premium market segments, particularly in Europe and North America, where compliance standards are more rigorous. This shift is also encouraging innovation in bio-based resins and recyclable materials, enabling suppliers to differentiate their product portfolios while aligning with global sustainability goals and ESG commitments.

Adoption of Performance-Based Contracting Models

Industrial customers are increasingly shifting toward procurement strategies that prioritize lifecycle cost efficiency and long-term asset performance rather than initial installation costs. This transition is particularly evident in industries such as wastewater treatment, chemical processing, and oil & gas, where downtime and maintenance costs can significantly impact operations. Resin suppliers that can provide validated performance data, such as extended service life, reduced maintenance intervals, and resistance to aggressive chemical exposure, are gaining a competitive edge. Performance-based contracting models often include warranties, service agreements, and technical support, allowing suppliers to establish long-term partnerships and recurring revenue streams.

Expansion in Asia Pacific Markets and Localized Production

Asia Pacific offers significant growth opportunities driven by rapid industrialization, infrastructure development, and expanding manufacturing capacity. Local production and supply chain localization are becoming critical for market entry and competitiveness. Companies investing in regional manufacturing facilities and partnerships can benefit from lower costs and improved market access. This trend is particularly strong in countries with large infrastructure projects and growing industrial bases.

Category-wise Analysis

Resin Type Insights

Epoxy resins are anticipated to account for approximately 41.5% share in 2026, due to their superior adhesion, chemical resistance, and mechanical strength, making them highly suitable for coatings, linings, and structural composites in demanding environments. These resins are extensively used in oil & gas pipelines, storage tanks, offshore platforms, and wastewater treatment facilities, where long-term durability and resistance to corrosive agents are critical. In renewable energy, epoxy-based systems are widely used in wind turbine blades and electrical insulation components. Continuous advancements in curing agents, such as faster-curing and low-temperature systems, are improving application efficiency and expanding usability across varied climates. The shift toward high-performance, longer-lifecycle coatings is reinforcing epoxy’s dominant position in value terms.

Vinyl ester resins are experiencing the fastest growth due to their excellent resistance to aggressive chemicals, moisture, and extreme environmental conditions. These resins are widely used in FRP tanks, pipes, ducts, and marine structures, such as ship hulls and ballast tanks, where exposure to acids, alkalis, and saline conditions is common. Compared to polyester resins, vinyl esters offer better mechanical strength and longer service life, making them increasingly preferred in critical infrastructure applications. For example, vinyl ester-based composites are widely used in flue gas desulfurization systems and chemical storage tanks. Innovations such as low-styrene emissions and enhanced thermal resistance are further expanding their application scope, particularly in regulated industrial environments.

Application Insights

Coatings are anticipated to account for approximately 49.2% market share in 2026, driven by strong demand for protective layers in industrial equipment, pipelines, storage tanks, and marine structures. These coatings act as a primary barrier against corrosion, significantly reducing maintenance frequency and extending asset life. Epoxy-based coatings are commonly used in oil & gas pipelines and offshore rigs, while polyurethane coatings are preferred for their flexibility and UV resistance in external environments. In wastewater treatment plants and chemical processing units, specialized corrosion-resistant coatings are applied to concrete and steel surfaces to prevent chemical degradation. The growing emphasis on asset longevity and lifecycle cost reduction continues to drive adoption of high-performance coating systems.

The composites segment is expanding rapidly due to increasing adoption in infrastructure, transportation, and energy applications. Fiber-reinforced plastic (FRP) materials, made using epoxy or vinyl ester resins, offer high strength-to-weight ratios, corrosion resistance, and design flexibility. These materials are increasingly replacing traditional metals in applications such as storage tanks, pipes, bridge components, and offshore platforms. In renewable energy, composites are essential for manufacturing wind turbine blades, while in transportation, they are used in lightweight vehicle components to improve fuel efficiency and reduce emissions. For instance, FRP pipes are widely used in desalination plants and the chemical processing industry due to their durability and lower maintenance requirements. Rising investments in sustainable infrastructure and lightweight engineering solutions are accelerating growth in this segment.

Regional Insights

North America Corrosion-resistant Resin Market Trends - Infrastructure Refurbishment & Advanced Epoxy Supply Expansion

North America is a mature market characterized by advanced infrastructure, high asset replacement cycles, and strong demand for high-performance corrosion-resistant materials. The U.S. leads the region in both market size and technological innovation, supported by significant refurbishment activity across oil & gas pipelines, refineries, and chemical processing plants. Industrial maintenance programs increasingly prioritize epoxy-based linings and vinyl ester coatings to extend asset life and reduce unplanned downtime. A notable development includes capacity optimization and restructuring efforts by companies such as Westlake Corporation following its acquisition of epoxy assets from Hexion Inc., which strengthened domestic supply capabilities and reduced reliance on imports.

Investment in renewable energy and advanced manufacturing is further supporting demand, particularly in wind energy, where epoxy resins are widely used in turbine blades. Companies such as Huntsman Corporation continue to expand their advanced materials portfolio for composites, targeting both energy and transportation sectors. Canada contributes through oil sands and petrochemical applications requiring corrosion-resistant linings, while Mexico is emerging as a cost-effective manufacturing hub for coatings and composite components. The region’s strong regulatory framework, combined with innovation-led competition, continues to favor high-performance and environmentally compliant resin systems.

Europe Corrosion-resistant Resin Market Trends - Sustainability-Driven Low-VOC and Eco-Resin Innovation

Europe’s corrosion-resistant resin market is shaped by stringent environmental regulations and a strong emphasis on sustainability and lifecycle performance. Countries such as Germany, the U.K., France, and Spain are key contributors, with demand driven by chemical processing, marine infrastructure, and renewable energy installations. Regulatory frameworks across the European Union require extensive environmental compliance, pushing manufacturers to develop low-VOC, styrene-free, and recyclable resin systems.

A relevant development includes sustainability-focused product innovation by BASF SE and Arkema S.A., both of which have introduced advanced resin formulations with reduced environmental impact. Similarly, Sika AG has expanded its protective coatings portfolio for infrastructure and industrial applications, reinforcing its presence in corrosion protection solutions. Infrastructure modernization projects, including coastal protection systems and chemical plant retrofits, are driving steady demand. Europe’s focus on sustainability and regulatory compliance is accelerating the transition toward advanced, eco-efficient resin technologies while maintaining high product performance standards.

Asia Pacific Corrosion-resistant Resin Market Trends - Rapid Industrial Growth & Policy-Backed Domestic Resin Production

Asia Pacific is the largest and fastest-growing market, accounting for approximately 38.7% of market share, driven by rapid industrialization, urbanization, and large-scale infrastructure investments. China and India dominate the regional market due to their extensive manufacturing bases and increasing demand for corrosion-resistant materials across chemical processing, construction, and energy sectors. China continues to lead in composite manufacturing, particularly for FRP tanks and pipes, while India is witnessing strong growth in infrastructure and water treatment projects requiring protective coatings and linings.

Recent policy developments, such as anti-dumping measures on epoxy resins in India, have encouraged domestic production and strengthened the position of local manufacturers. Companies such as Allnex and Polynt Group are expanding their presence in the region through partnerships and localized production strategies to capture growing demand. In addition, Japan’s advanced manufacturing sector continues to focus on high-performance coatings for marine and industrial applications, while ASEAN countries are emerging as key hubs for composite fabrication. The combination of cost advantages, policy support, and expanding end-use industries makes Asia Pacific the most strategically important growth region for corrosion-resistant resin suppliers.

Competitive Landscape

The global corrosion-resistant resin market is moderately fragmented, with a mix of global chemical companies and regional players. Leading companies dominate high-performance segments, while smaller firms focus on cost-competitive solutions. Competition is driven by product innovation, pricing strategies, and technical expertise. Companies are increasingly investing in capacity expansion and supply chain optimization to strengthen their market position. Key players are focusing on innovation, sustainability, and regional expansion. Strategies include developing advanced resin formulations, improving supply chain efficiency, and forming strategic partnerships to enhance market reach and technical capabilities.

Key Industry Developments

- In March 2025, Westlake Corporation introduced its EpoVIVE™ epoxy product portfolio at the European Coatings Show 2025, focusing on sustainable, high-performance resin solutions aimed at improving safety, robustness, and environmental compliance in coatings applications.

Companies Covered in Corrosion-resistant Resin Market

- Ashland Inc.

- Hexion Inc.

- Huntsman Corporation

- BASF SE

- Dow Inc.

- Olin Corporation

- Polynt Group

- Reichhold LLC

- Scott Bader Company Ltd.

- Allnex

- AOC Resins

- Swancor Holding Co., Ltd.

- Sino Polymer Co., Ltd.

- Aditya Birla Chemicals

- Kukdo Chemical Co., Ltd.

- DIC Corporation

Frequently Asked Questions

The corrosion-resistant resin market is estimated to be valued at US$10.1 billion in 2026.

The market is projected to reach US$15.4 billion by 2033.

Key trends include increasing adoption of low-VOC and styrene-free resin systems, rising use of composite materials in renewable energy and transportation, and growing emphasis on lifecycle performance and sustainability-driven procurement. The shift toward lightweight and corrosion-resistant materials in infrastructure and automotive sectors is also shaping market growth.

The epoxy resin segment is the leading category, accounting for approximately 41.5% of the market share, driven by its superior adhesion, chemical resistance, and durability across coatings, linings, and composites.

The corrosion-resistant resin market is expected to grow at a CAGR of 6.2% between 2026 and 2033.

Some of the major players include BASF SE, Dow Inc., Huntsman Corporation, Ashland Inc., and Allnex.