- Specialty & Fine Chemicals

- Concrete Floor Coating Market

Concrete Floor Coating Market Size, Share, and Growth Forecast 2026 - 2033

Concrete Floor Coating Market by Product Type (Epoxy, Polyurethanes, Polyaspartic, Others), Application (Indoor, Outdoor), and Regional Analysis, 2026 - 2033

Concrete Floor Coating Market Size and Trend Analysis

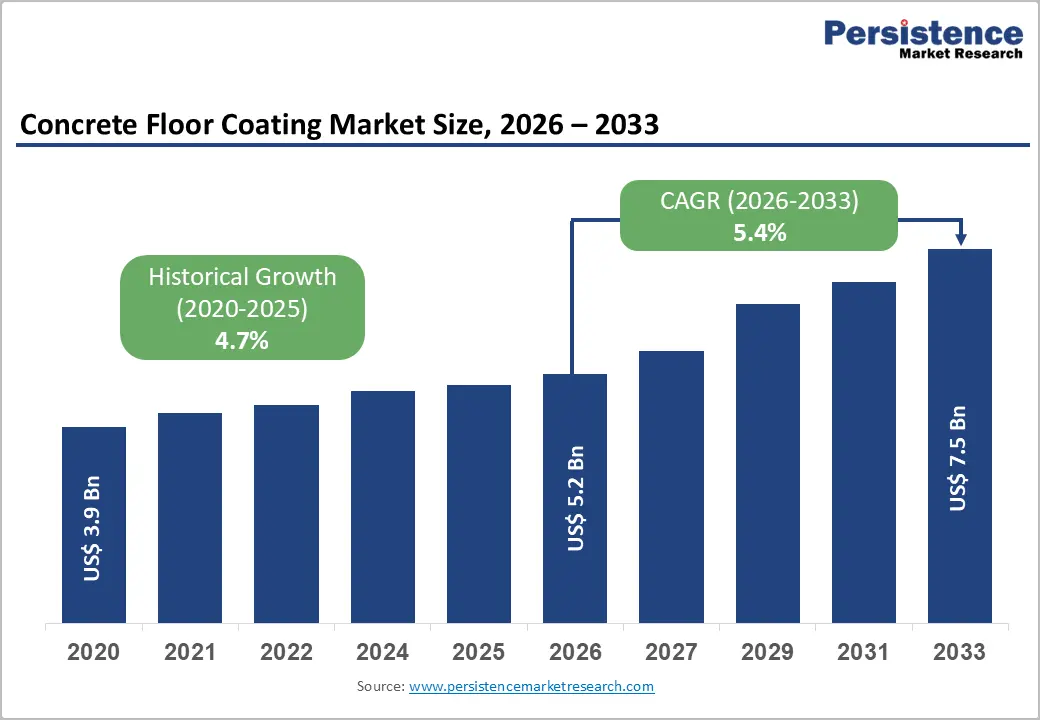

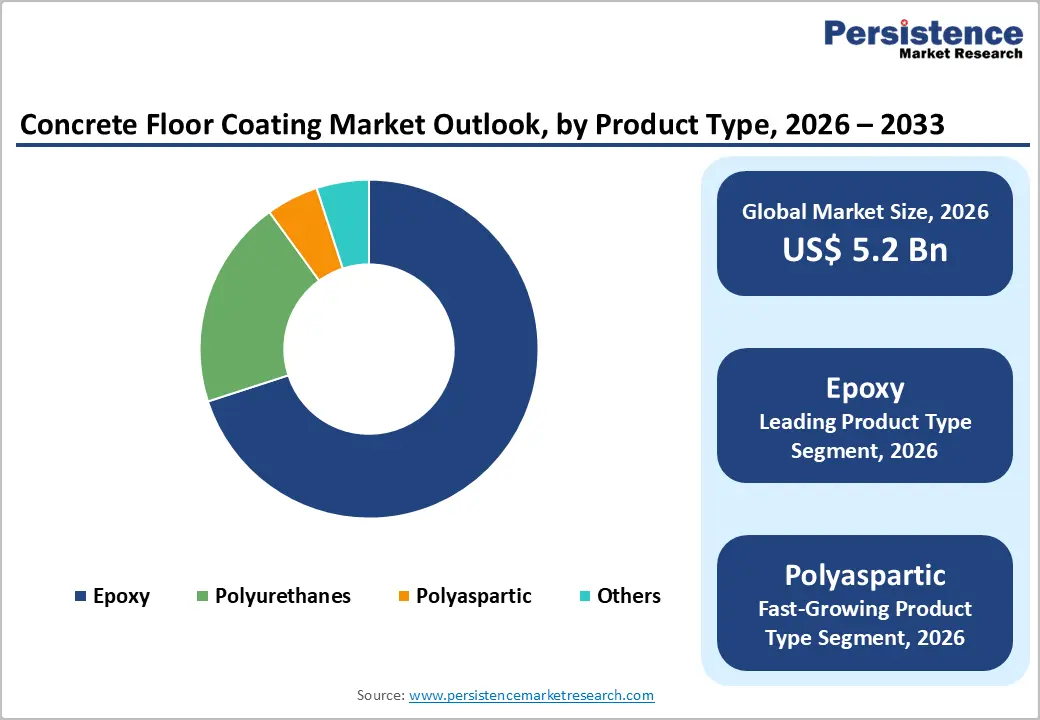

The global concrete floor coating market size is expected to be valued at US$ 5.2 billion in 2026 and projected to reach US$ 7.5 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

Robust demand from commercial, industrial, and residential construction is the primary growth catalyst, supported by rising investments in warehousing, food-processing plants, and automotive service centers.

According to the U.S. Census Bureau, total construction spending reached an annualized US$ 2.16 trillion in 2024, directly fueling the need for durable, chemical-resistant flooring solutions across end-use sectors.

Key Industry Highlights

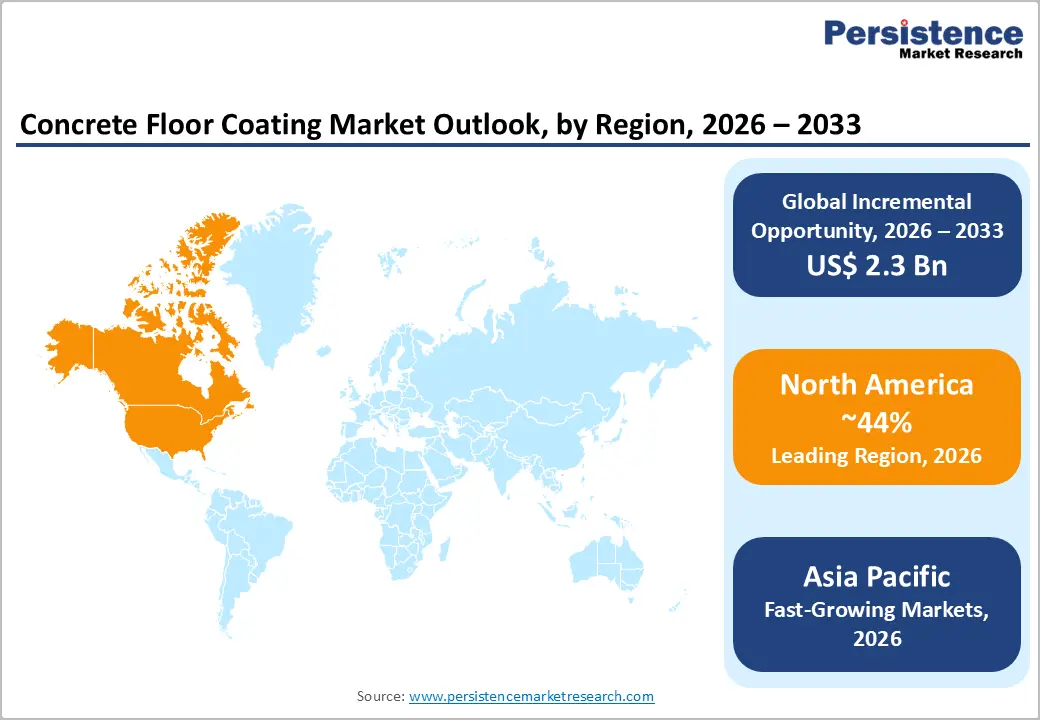

- Leading Region: North America leads the global concrete floor coating market with a commanding 44% share in 2026, driven by extensive warehousing growth, automotive reshoring, and strict OSHA workplace safety norms.

- Fastest Growing Region: Asia Pacific is the fastest-growing region during 2026 - 2033, fueled by rapid industrialization in China, India, and Southeast Asia, alongside government-backed manufacturing and logistics infrastructure investments.

- Dominant Segment: Epoxy coatings dominate the product landscape with about 70% market share in 2026, owing to balanced cost, chemical resistance, mechanical strength, and broad suitability across industrial and commercial floors.

- Fastest Growing Segment: Polyaspartic coatings form the fastest-growing segment at a 6% CAGR through 2033, propelled by rapid cure times, UV stability, and rising adoption in retail, hangar, and decorative residential applications.

- Key Market Opportunity: A key opportunity lies in decorative and residential garage coatings, supported by US$ 481 billion in U.S. home improvement spending and rising consumer demand for durable, aesthetic flooring finishes.

DRO Analysis

Drivers - Surge in Industrial and Warehousing Construction Activity

The rapid expansion of warehousing, logistics hubs, and manufacturing plants is the foremost driver propelling concrete floor coating demand. According to the U.S. Bureau of Labor Statistics, employment in warehousing and storage rose by nearly 35% between 2019 and 2024, reflecting unprecedented logistics infrastructure expansion.

Similarly, the European Construction Industry Federation (FIEC) reported that non-residential construction output grew by 2.3% in 2024 across the EU-27, with logistics and industrial space leading the way. Floor coatings such as epoxy and polyurethane provide superior abrasion resistance, chemical protection, and load-bearing performance essential for forklift traffic, automated storage, and heavy machinery operations, making them indispensable for modern industrial facilities.

Stringent Workplace Safety and Hygiene Regulations

Global regulatory bodies are mandating safer, cleaner industrial environments, fueling the adoption of high-performance floor coatings. The U.S. Occupational Safety and Health Administration (OSHA) enforces strict standards on slip-resistance and contamination control, particularly within food, pharmaceutical, and healthcare facilities regulated by the U.S. FDA.

The European Food Safety Authority (EFSA) and HACCP frameworks similarly require seamless, antimicrobial flooring in food processing zones. Polyurethane and polyaspartic systems offer chemical inertness, easy cleanability, and resistance to microbial growth, satisfying these compliance demands. The growing emphasis on GMP-certified manufacturing facilities globally is significantly accelerating the replacement of conventional flooring with engineered coating systems.

Restraints - Volatility in Raw Material Prices

Fluctuating prices of petrochemical-derived raw materials such as epichlorohydrin, bisphenol-A, and isocyanates pose a significant threat to manufacturers' margins. According to the U.S. Energy Information Administration (EIA), crude oil prices swung between US$ 70 and US$ 95 per barrel during 2023-2024, creating cost unpredictability across the polymer supply chain. This volatility complicates long-term contract pricing and squeezes profit margins for both manufacturers and applicators, particularly small and medium contractors who lack hedging capabilities.

Stringent Environmental and VOC Regulations

Concrete floor coatings, especially solvent-based epoxy and polyurethane systems, traditionally emit volatile organic compounds (VOCs). Regulations such as the U.S. EPA's National Emission Standards and the European Union's REACH framework restrict VOC content, compelling manufacturers to invest in low-emission reformulations. The California Air Resources Board (CARB) caps VOCs in industrial maintenance coatings at 250 g/L, raising compliance costs and limiting traditional product portfolios. These restrictions necessitate expensive R&D for waterborne and high-solid alternatives, slowing adoption in price-sensitive markets.

Opportunities - Growing Adoption of Polyaspartic Coatings in Fast-Track Projects

Polyaspartic coatings, growing at an estimated 6% CAGR from 2026 to 2033, present a compelling opportunity for industry participants. Their rapid cure time, often less than one hour, enables single-day floor installations, drastically reducing facility downtime in retail showrooms, automotive service centers, and aviation hangars. The Federal Aviation Administration (FAA) and major retail chains increasingly specify polyaspartic systems for hangar floors and store renovations due to their UV stability and minimal disruption.

Major coating manufacturers, including The Sherwin-Williams Company and PPG Industries, have expanded their polyaspartic product lines in recent years to capture this fast-growing niche. The technology aligns well with the broader industrial flooring market push toward operational efficiency, durability, and aesthetic versatility.

Expansion of Decorative and Residential Garage Coatings

The booming home improvement sector, particularly in North America and parts of Europe, is generating sizable demand for decorative concrete coatings. According to the Joint Center for Housing Studies of Harvard University, U.S. home improvement spending exceeded US$ 481 billion in 2024. Homeowners increasingly seek durable garage and basement flooring with metallic, flake, or quartz finishes that offer both functionality and visual appeal.

Companies such as Elite Crete Systems and BEHR Process Corp. are launching DIY-friendly polyaspartic and epoxy kits to capitalize on this trend. Additionally, the growth of premium residential developments and luxury showrooms presents long-term demand opportunities for value-added decorative floor coating systems.

Category-wise Analysis

Product Type Insights

Epoxy is the dominant product type, accounting for nearly 70% of global concrete floor coating market share in 2026. Its leadership stems from a balanced combination of cost-effectiveness, chemical resistance, mechanical strength, and ease of application across diverse end-use environments. Epoxy coatings withstand exposure to acids, alkalis, oils, and abrasive traffic, making them the standard choice for warehouses, food-processing plants, and automotive workshops regulated under OSHA and FDA guidelines.

According to the American Coatings Association (ACA), epoxy formulations represent the largest volume share within industrial maintenance coatings. Continuous innovations in waterborne and 100%-solids epoxy systems by manufacturers such as BASF SE and Sherwin-Williams further extend their dominance by addressing VOC and sustainability concerns without compromising performance.

Application Insights

The indoor application segment commands the leading position, capturing approximately 78% of total demand in 2026. Indoor environments, including manufacturing plants, warehouses, retail outlets, hospitals, and parking garages, require coatings that withstand heavy foot and vehicle traffic, chemical spillage, and frequent cleaning. According to the U.S. Census Bureau, private nonresidential construction spending hit US$ 1.13 trillion in 2024, with manufacturing and warehouse construction leading growth.

Strict hygiene mandates from HACCP, FDA, and EU GMP in food and pharmaceutical facilities further drive indoor coating adoption. Additionally, the rise of e-commerce fulfillment centers and cold-storage facilities reinforces demand. Indoor flooring also benefits from controlled curing conditions, allowing wider product use including epoxy, polyurethane, and decorative quartz systems.

Regional Analysis

North America Concrete Floor Coating Market Trends and Insights

North America leads the global market with a 44% share in 2026, driven by extensive industrial infrastructure, robust warehousing expansion, and strict workplace safety norms enforced by OSHA and EPA. Booming e-commerce logistics, automotive manufacturing reshoring, and rapid adoption of polyaspartic and decorative coatings in residential garages reinforce regional dominance. Continuous renovation of aging commercial real estate further supports steady demand growth.

U.S. Concrete Floor Coating Market Size

The United States represents nearly 85% of North American demand, supported by US$ 2.16 trillion in total construction spending in 2024 reported by the U.S. Census Bureau. Massive warehouse construction tied to e-commerce giants like Amazon and Walmart, alongside semiconductor fabrication plants under the CHIPS and Science Act, are fueling robust uptake of high-performance epoxy and polyaspartic flooring systems.

Europe Concrete Floor Coating Market Trends and Insights

Europe holds a strong global position, supported by stringent EU REACH, CARB-equivalent VOC, and food safety regulations driving migration to waterborne and low-VOC formulations. Demand stems from food processing, pharmaceutical manufacturing, and automotive sectors. Sustainable construction initiatives under the European Green Deal and rising warehousing investments further boost adoption of advanced epoxy and polyurethane coatings region wide.

Germany Concrete Floor Coating Market Size

Germany commands roughly 22% of the European concrete floor coating market, anchored by its strong automotive, chemical, and pharmaceutical manufacturing base. According to Destatis, Germany's industrial production output remains a European benchmark, with chemical industry revenues exceeding EUR 230 billion in 2024. Demand is fueled by Industry 4.0 facility upgrades and stringent DIN flooring standards.

U.K. Concrete Floor Coating Market Size

The United Kingdom accounts for approximately 15% of European demand. The Office for National Statistics (ONS) reported construction output of GBP 178 billion in 2024, with logistics warehousing leading new builds. Growth is supported by strict HSE workplace flooring requirements and rising adoption of polyaspartic systems in retail and automotive showroom refurbishments across major cities.

France Concrete Floor Coating Market Size

France holds nearly 13% of the European market, supported by strong food and beverage manufacturing and pharmaceutical exports tracked by INSEE. Government-led infrastructure initiatives such as France Relance and the Grand Paris project boost commercial construction activity. Strict hygiene compliance under EFSA food safety norms drives continuous demand for seamless, antimicrobial industrial coatings.

Asia Pacific Concrete Floor Coating Market Trends and Insights

Asia Pacific is the fastest-growing region, propelled by rapid industrialization, urbanization, and infrastructure expansion across China, India, and Southeast Asia. China alone contributes nearly half of regional demand, fueled by mega-warehousing, EV manufacturing, and pharmaceutical plant build-outs. According to the National Bureau of Statistics of China, fixed-asset investment in manufacturing rose by 9.2% in 2024, sustaining strong floor coating uptake.

India Concrete Floor Coating Market Size

India is among the fastest-expanding national markets, accounting for nearly 15% of Asia Pacific demand. The Ministry of Statistics and Programme Implementation (MoSPI) reported 8.2% GDP growth in fiscal 2024, with construction expanding briskly. Government schemes like Make in India, PLI for electronics, and PM Gati Shakti logistics infrastructure accelerate adoption of epoxy and polyurethane industrial floors.

Japan Concrete Floor Coating Market Size

Japan represents around 18% of Asia Pacific demand, anchored by automotive, electronics, and semiconductor industries. According to the Japan Paint Manufacturers Association (JPMA), industrial coatings shipments remained stable through 2024. Demand is supported by precision manufacturing standards, strict JIS quality benchmarks, and ongoing facility upgrades by companies such as Toyota and Sony.

Southeast Asia Concrete Floor Coating Market Size

Southeast Asia accounts for roughly 12% of regional demand, with Vietnam, Indonesia, and Thailand as key growth engines. The ASEAN Secretariat reports manufacturing FDI inflows surpassing US$ 100 billion in 2024 across the region, driven by China-plus-one supply chain shifts. Expanding electronics, food processing, and warehousing facilities are spurring rapid floor coating adoption.

Competitive Landscape

The global concrete floor coating market is moderately consolidated, with the top five players controlling a substantial share while numerous regional contractors and specialty manufacturers compete in niche applications. Leading companies such as The Sherwin-Williams Company, BASF SE, PPG Industries, Axalta Coating Systems, and Jotun focus on R&D for low-VOC, fast-cure, and antimicrobial formulations. Strategic acquisitions, distributor network expansion, and partnerships with applicator networks define growth strategies.

Emerging trends include digital color-visualization tools, value-added applicator training programs, and bundled service-product offerings. Sustainability-driven product portfolios and bio-based resin development are increasingly important competitive differentiators.

Key Developments:

- In March 2025, The Sherwin-Williams Company launched its next-generation polyaspartic floor coating system targeting commercial and industrial fast-track applications, offering enhanced UV resistance and same-day return-to-service capability.

- In November 2024, PPG Industries expanded its powder and liquid coating manufacturing capacity in Sumaré, Brazil, with a multi-million-dollar investment to support growing Latin American demand for industrial flooring solutions.

- In July 2024, BASF SE introduced new bio-based polyurethane raw materials under its Sovermol® line, supporting sustainable, low-emission concrete floor coating formulations across European and North American markets.

Concrete Floor Coating Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 3.9 billion |

| Current Market Value (2026) | US$ 5.2 billion |

| Projected Market Value (2033) | US$ 7.5 billion |

| CAGR (2026 - 2033) | 5.4% |

| Leading Region | North America, 44% |

| Dominant Category-1 | Epoxy, 70% share |

| Top-ranking Category-2 | Indoor, 78% share |

| Incremental Opportunity | US$ 2.3 billion |

Companies Covered in Concrete Floor Coating Market

- Trucrete Surfacing Systems

- The Sherwin-Williams Company

- North American Coating Solutions

- BASF SE

- Vanguard Concrete Coating

- Tennant Coatings

- Jotun

- Axalta Coating Systems

- Elite Crete Systems

- Stonhard

- PPG Pittsburgh Paints

- Key Resin Company

- BEHR Process Corp.

- Epmar Corp.

- Pratt & Lambert.

Frequently Asked Questions

The global concrete floor coating market is expected to be valued at US$ 5.2 billion in 2026 and is forecast to reach US$ 7.5 billion by 2033, expanding at a steady 5.4% CAGR.

Rapid expansion of warehousing, logistics, and manufacturing facilities, coupled with stringent workplace safety and hygiene mandates from OSHA, FDA, and EU REACH, is the foremost driver fueling robust global demand for concrete floor coatings.

North America leads the market with approximately 44% share in 2026, supported by massive warehouse construction, automotive reshoring under the CHIPS Act, and strong residential and commercial renovation activity across the United States and Canada.

The growing adoption of polyaspartic coatings, projected to expand at a 6% CAGR, alongside rising decorative residential garage flooring demand backed by US$ 481 billion in U.S. home improvement spending, presents a significant growth opportunity.

Major participants include The Sherwin-Williams Company, BASF SE, PPG Industries, Axalta Coating Systems, Jotun, Stonhard, Tennant Coatings, Elite Crete Systems, BEHR Process Corp., and Key Resin Company, among other regional and specialty manufacturers.