- Executive Summary

- Global Chloromethane Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Pharmaceutical Industry Overview

- Global Beauty and Personal Care Industry Overview

- Global Chemical Industry Overview

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Chloromethane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Chloromethane Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Product Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Methylene Chloride

- Methyl Chloride

- Carbon Tetrachloride

- Chloroform

- Others

- Market Attractiveness Analysis: Product Type

- Global Chloromethane Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Application, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Silicones

- Agriculture Chemicals

- Pharmaceutical

- Chemical Intermediate

- Personal Care

- Foam Blowing

- Other

- Market Attractiveness Analysis: Application

- Global Chloromethane Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Chloromethane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Methylene Chloride

- Methyl Chloride

- Carbon Tetrachloride

- Chloroform

- Others

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Silicones

- Agriculture Chemicals

- Pharmaceutical

- Chemical Intermediate

- Personal Care

- Foam Blowing

- Other

- Europe Chloromethane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Methylene Chloride

- Methyl Chloride

- Carbon Tetrachloride

- Chloroform

- Others

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Silicones

- Agriculture Chemicals

- Pharmaceutical

- Chemical Intermediate

- Personal Care

- Foam Blowing

- Other

- East Asia Chloromethane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Methylene Chloride

- Methyl Chloride

- Carbon Tetrachloride

- Chloroform

- Others

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Silicones

- Agriculture Chemicals

- Pharmaceutical

- Chemical Intermediate

- Personal Care

- Foam Blowing

- Other

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by , 2026-2033

- South Asia & Oceania Chloromethane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Methylene Chloride

- Methyl Chloride

- Carbon Tetrachloride

- Chloroform

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Silicones

- Agriculture Chemicals

- Pharmaceutical

- Chemical Intermediate

- Personal Care

- Foam Blowing

- Other

- Latin America Chloromethane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Methylene Chloride

- Methyl Chloride

- Carbon Tetrachloride

- Chloroform

- Others

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Silicones

- Agriculture Chemicals

- Pharmaceutical

- Chemical Intermediate

- Personal Care

- Foam Blowing

- Other

- Middle East & Africa Chloromethane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Methylene Chloride

- Methyl Chloride

- Carbon Tetrachloride

- Chloroform

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Silicones

- Agriculture Chemicals

- Pharmaceutical

- Chemical Intermediate

- Personal Care

- Foam Blowing

- Other

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- AkzoNobel N.V.

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Dow Chemical Company

- INEOS Group

- Solvay S.A.

- Shin-Etsu Chemical Co., Ltd.

- AGC Inc.

- Tokuyama Corporation

- KEM ONE

- Ercros S.A.

- SRF Limited

- Shandong Lubei Chemical Co., Ltd.

- Juhua Group

- Gujarat Alkalies and Chemicals Ltd.

- AkzoNobel N.V.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Specialty & Fine Chemicals

- Chloromethane Market

Chloromethane Market Size, Share, and Growth Forecast 2026 - 2033

Chloromethane Market by Product Type (Methylene Chloride, Methyl Chloride, Carbon Tetrachloride, Chloroform, Others), Application (Silicones, Agriculture Chemicals, Pharmaceutical, Chemical Intermediate, Personal Care, Foam Blowing, Other), and Regional Analysis for 2026 - 2033

Chloromethane Market Size and Trend Analysis

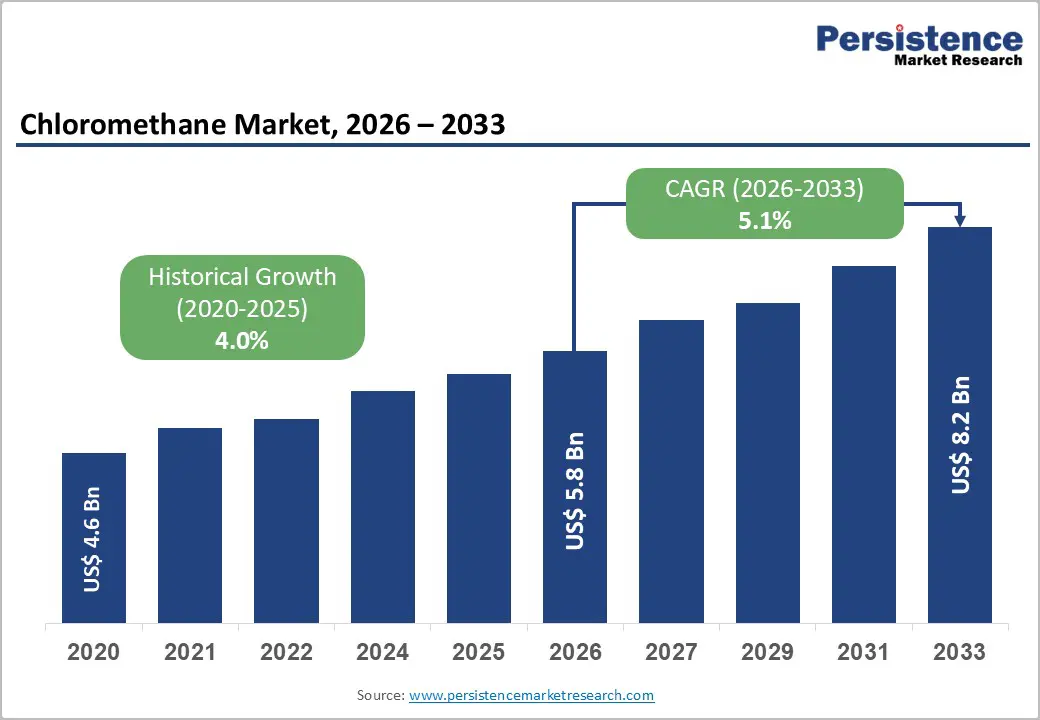

The global chloromethane market is valued at US$5.8 billion in 2026 and is projected to reach US$8.2 billion by 2033, growing at a CAGR of 5.1% over 2026 - 2033. Chloromethane’s indispensable role as a chemical intermediate in silicone manufacturing, pharmaceuticals, and agrochemicals underpins this steady growth trajectory.

According to the Global Silicones Council, an estimated 673,000 metric tons of silicone products are sold to the construction sector annually, directly amplifying methyl chloride demand. Rapid industrialization in the Asia-Pacific, rising pharmaceutical production capacity in India and China, and the accelerating shift toward electric vehicles further consolidate this upward demand cycle.

Key Industry Highlights:

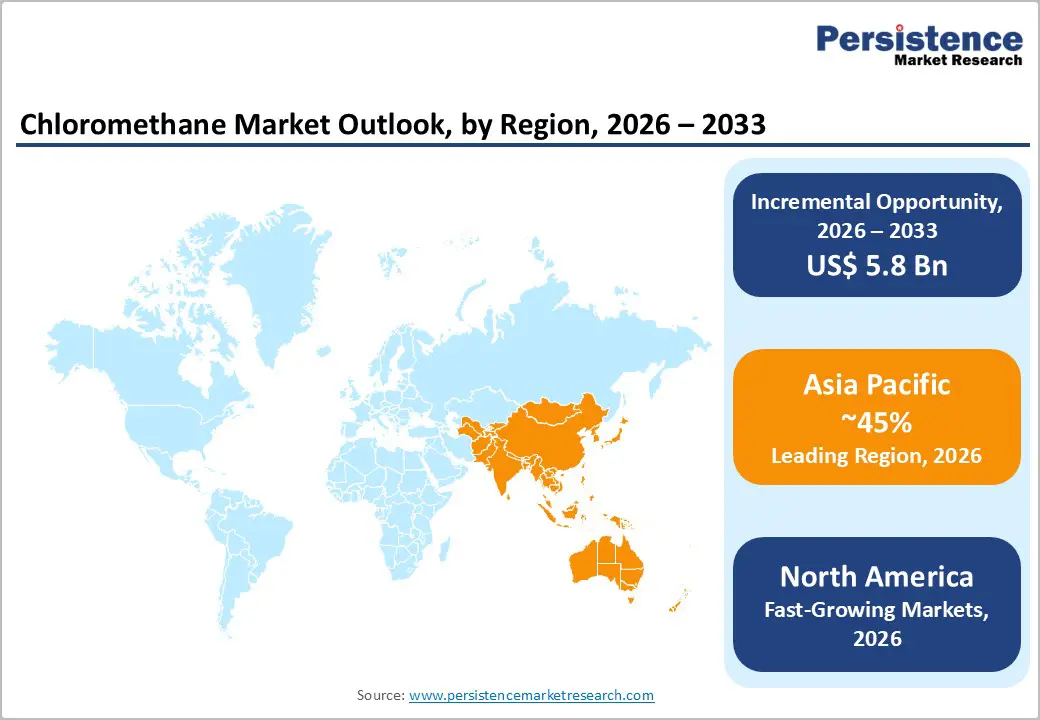

- Leading Region: Asia-Pacific dominates the global chloromethane market with over 45% of total consumption, anchored by China’s massive silicone and agrochemical industries and India’s rapidly expanding pharmaceutical and API manufacturing sector, supported by government-led investment policies.

- Fastest Growing Region: North America is the fastest growing region, with the U.S. representing nearly 950 kilotons of annual demand.

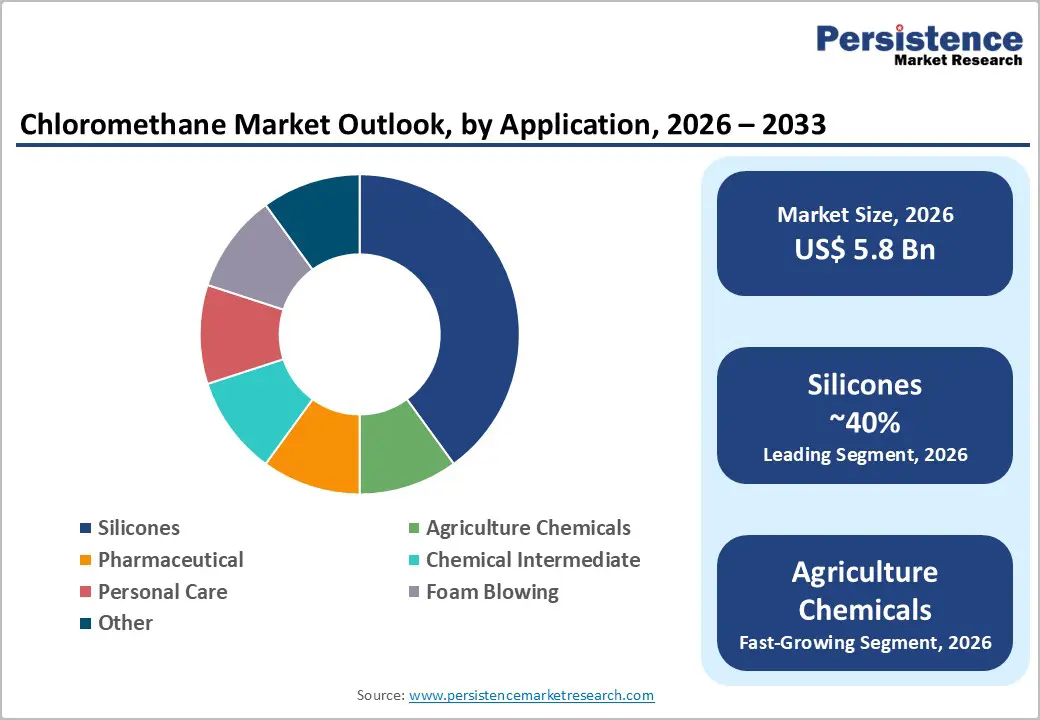

- Dominant Segment: Silicones is the leading application segment, commanding approximately 40% market share, fueled by indispensable demand from construction, automotive, electronics, and personal care industries globally, linked directly to methyl chloride feedstock consumption.

- Fastest Growing Segment: Methyl chloride is the fastest growing product type, supported by expanding silicone polymer production, EV thermal management applications, and growing demand from specialty chemical and pharmaceutical manufacturing sectors globally.

- Key Opportunity: The EV and renewable energy transition offers transformative growth for chloromethane producers, with silicone demand in solar encapsulants and EV battery systems projected to grow at over 8% annually through 2030, per IRENA, creating a high-value, structurally durable growth channel.

| Key Insights | Details |

|---|---|

| Chloromethane Market Size (2026E) | US$ 5.8 Bn |

| Market Value Forecast (2033F) | US$ 8.2 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.1% |

| Historical Market Growth (2020 - 2025) | 4.0% |

DRO Analysis

Drivers - Surging Demand for Silicone Polymers Across Construction and Automotive Industries

Silicone polymers constitute the largest application segment for chloromethane, representing nearly 40% of global demand. Methyl chloride serves as an essential feedstock in the synthesis of methyl chlorosilanes, which are subsequently utilized to produce silicone elastomers, fluids, and resins. Industry data indicates that approximately 673,000 metric tons of silicone products are supplied annually to the construction sector, the highest among all end use industries.

The global construction market continues to expand across Asia Pacific, the Middle East, and Latin America. Concurrently, growing electric vehicle adoption is driving additional need for silicone-based thermal management materials. With global EV sales surpassing 14 million units in 2023 and related silicone usage rising steadily, these structural trends are projected to sustain strong chloromethane demand through 2033.

Rising Pharmaceutical and Agrochemical Production in Emerging Economies

Chloromethane, including methylene chloride and chloroform, serves as a critical solvent and synthetic intermediate within the pharmaceutical sector. It is extensively utilized in the manufacture of active pharmaceutical ingredients, antibiotics, anesthetics, and vitamins. With the global pharmaceutical market exceeding US$1.6 trillion in 2024, India’s US$42 billion pharmaceutical industry has emerged as a major producer of generic medicines and a key consumer of chloromethane.

Concurrently, rising pesticide application in Asia and Latin America, where derivatives such as disodium methanearsonate and paraquat are incorporated into herbicide formulations, continues to support agrochemical demand. As global food security pressures intensify, driven by a population projected to reach 9.7 billion by 2050, chloromethane consumption in pharmaceutical and agrochemical applications is expected to remain structurally robust over the forecast horizon.

Restraint - Stringent Environmental Regulations Limiting Industrial Usage

Chloromethane compounds, particularly methylene chloride and carbon tetrachloride, face significant regulatory headwinds across major markets. The U.S. Environmental Protection Agency (EPA) has prohibited the use of methylene chloride in all paint removers intended for consumer use, directly curtailing one of its key applications. In Europe, the REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulation and the CLP Regulation impose strict exposure limits, handling, and reporting requirements. Compliance costs associated with Volatile Organic Compound (VOC) and carbon emission standards are estimated to account for approximately 27% of total operating costs for chloromethane manufacturers. Restrictions in developed economies have collectively reduced industrial solvent consumption of methylene chloride by an estimated 11% between 2021 and 2024, constraining revenue in mature markets.

Volatile Feedstock Prices and Raw Material Supply Uncertainty

The production of chloromethane is primarily dependent on methanol and natural gas (methane), both of which are subject to significant price volatility driven by geopolitical tensions, seasonal demand fluctuations, and energy market cycles. In the Asia-Pacific, natural gas prices increased by approximately 10% in 2024, driven by supply chain disruptions and geopolitical uncertainty. This directly elevates the cost of chloromethane synthesis, squeezing manufacturer margins and limiting price competitiveness. Feedstock price instability also hampers long-term capital planning, discouraging capacity expansion investments, particularly among mid-sized and smaller regional producers. The limited substitutability of methanol in current production pathways further amplifies this vulnerability, posing a sustained restraint on market profitability.

Opportunities - Expanding API Manufacturing and Pharmaceutical Growth in India and China

The pharmaceutical industry continues to represent one of the most substantial and enduring growth avenues for participants in the chloromethane market. India’s National Chemicals Policy 2024 aims to raise the chemical sector’s GDP contribution by US$100 billion, with a strong focus on enhancing domestic intermediate chemical production capacity. Complementing this objective, the Production Linked Incentive (PLI) Scheme for Pharmaceuticals is directing significant investment toward API manufacturing, thereby reinforcing demand for pharmaceutical grade methylene chloride.

China’s chemical industry, contributing approximately US$1.5 trillion to national GDP in 2024, has likewise recorded consistent growth in chloromethane consumption. As of 2024, the Asia Pacific region has expanded chloromethane production capacity by 43% since 2018, with China and India jointly accounting for over 60% of regional output. Firms aligning high purity production and efficient supply chains with these demand hubs are positioned to secure premium contracts through 2033.

Electric Vehicle and Renewable Energy Transition Creating Structural Silicone Demand

The global shift toward renewable energy and electric mobility is creating a sustained and structurally strong demand for chloromethane based silicone products. In solar applications, silicones play a critical role as encapsulants, sealants, and potting materials for photovoltaic modules. Global solar capacity additions are projected to surpass 350 GW annually by 2025, while silicon demand in solar technologies is expected to expand at over 8% per year through 2030.

In the electric vehicle sector, silicone rubbers derived from methyl chloride intermediates are integral to battery thermal management, high voltage insulation, and motor encapsulation. With more than 300 million EVs anticipated on global roads by 2030, companies advancing high purity methyl chloride production and closed loop sustainable manufacturing are well positioned to benefit from this rapidly expanding and premium downstream market.

Category-wise Analysis

Product Type Insights

Methyl chloride is the dominant product in the global chloromethane market, accounting for approximately 45% of the market value in 2025. This leadership position is fundamentally anchored in its role as the primary feedstock for methyl chlorosilane synthesis, which underpins global silicone polymer production. Shin-Etsu Chemical Co., Ltd. and Dow Chemical Company, two of the world’s largest silicone manufacturers, collectively rely on methyl chloride as a core raw material. The versatility of methyl chloride as a methylating and chlorinating agent across sectors, including agrochemicals, cellulose ethers, and quaternary ammonium compounds, further reinforces its dominance.

According to OECD industrial chemical usage data, global silicone demand is projected to rise steadily through 2030, driven by construction, automotive, and electronics sector investments. In volume terms, methyl chloride accounted for approximately 48% of the total chloromethane market volume in 2024. Its indispensable role in both the silicone value chain and diversified specialty chemical synthesis makes it the most structurally resilient and growth-oriented product type within the global chloromethane product portfolio.

Application Insights

The silicones application segment maintains a dominant position in the global chloromethane market, accounting for an estimated 40% value share in 2025. Silicone’s exceptional thermal stability, chemical resistance, electrical insulation, and flexibility make it indispensable across construction, automotive, electronics, healthcare, and personal care industries. According to industry data, construction applications alone utilize nearly 673,000 metric tons of silicone products annually, reinforcing their importance in structural bonding, weatherproofing, and energy efficient glazing.

Rising electric vehicle adoption and increased semiconductor investments are further expanding silicone demand, with the automotive silicone market growing by approximately 22% between 2020 and 2024. Agriculture chemicals form the second largest application, supported by sustained growth in herbicide and pesticide usage across Asia and Latin America. This strong linkage to methyl chloride feedstock ensures silicones remain the most stable and growth driven segment through 2026 - 2033.

Regional Insights

North America Chloromethane Market Trends

North America remains one of the most strategically significant markets for chloromethane, with the U.S. accounting for approximately 24% of global consumption in 2024, representing nearly 950 kilotons of annual demand. The country’s robust pharmaceutical manufacturing base, strong chemical intermediates sector, and sustained demand from Occidental Chemical Corporation (OxyChem) and Dow Chemical Company’s domestic silicone operations underpin market stability. The U.S. EPA’s regulatory framework, including the ban on methylene chloride in consumer paint strippers and VOC emission limits, has redirected demand toward higher-value pharmaceutical and silicone applications, elevating average revenue per ton in the region.

Evolving U.S. trade tariff policies on chemical imports and the indirect effects of Middle East geopolitical tensions on energy and feedstock prices are influencing North American supply chain configurations. Regional producers are increasing investment in emission-control technologies and closed-loop production systems to meet tightening OSHA and EPA standards. The expanding EV and renewable energy sectors are expected to generate new silicone-related demand for chloromethane from North American manufacturers over the 2026-2033 period, reinforcing the region’s position as a high-value, premium-grade chloromethane market.

Europe Chloromethane Market Trends

Europe represents a mature, regulation driven chloromethane market, with Germany, France, and Spain serving as the primary demand centers. Germany is one of the region’s leading producers and exporters, supported by major facilities operated by Nouryon and INEOS INOVYN. Stringent EU frameworks, including REACH and the CLP Regulation, impose rigorous standards on handling and exposure limits, prompting manufacturers to invest in advanced abatement and recovery technologies. Despite these regulatory constraints, demand for pharmaceutical intermediates and silicone manufacturing remains resilient.

The European Green Deal and Circular Economy Action Plan are further accelerating the shift toward low emission production practices. Spain’s Ercros S.A. continues to meet stable domestic pharmaceutical and agrochemical needs, while supply chain disruptions linked to Middle Eastern geopolitical tensions have driven producers to strengthen methanol supply security. Post Brexit, the U.K. is aligning its regulatory framework with EU REACH to maintain consistent product standards.

Asia Pacific Chloromethane Market Trends

Asia Pacific remains the leading global market for chloromethane, accounting for more than 45% of total consumption. China, India, and Japan serve as the principal demand centers, with China’s chemical industry, valued at approximately US$1.5 trillion in 2024, representing the world’s largest consumer of chloromethane due to its extensive silicone polymer, agrochemical, and pharmaceutical production. China’s position as the world’s largest pesticide exporter, contributing over 30% of global output, further reinforces demand for agrochemical grade chloromethane.

India’s growth trajectory is similarly strong, supported by the National Chemicals Policy 2024, which targets a US$100 billion expansion in the chemical sector GDP and increased API manufacturing. Japan and South Korea drive additional demand through advanced semiconductor and electronics grade silicone production. Regional supply chain shifts, alongside a 43% rise in production capacity since 2018, have strengthened Asia Pacific’s standing as a self sufficient chloromethane hub.

Competitive Landscape

The global chloromethane market exhibits a highly consolidated structure, with the top eight players collectively controlling over 70% of global market capacity. AkzoNobel N.V. (Nouryon) leads with a market share exceeding 17%. Key competitive strategies include capacity expansion, vertical integration, and R&D investment in sustainable and low-emission production technologies. Market leaders differentiate through production scale, product purity grades, global distribution networks, and integrated downstream silicone positioning. Emerging business model trends include long-term supply contracts with silicone manufacturers, investment in closed-loop solvent recovery systems, and development of high-purity pharmaceutical-grade chloromethane product lines. The top 10 companies account for approximately 62% of global chloromethane capacity, underscoring the market’s oligopolistic structure and high barriers to entry for new entrants.

Key Developments:

- March 2026: Shintech, the U.S. arm of Shin-Etsu Chemical, announced a US$ 3.4 billion investment to expand chlor-alkali (280,000 t/yr chlorine, 310,000 t/yr caustic soda), ethylene (625,000 t/yr), and vinyl chloride monomer (VCM) capacity at its Plaquemine, Louisiana facility. Completion is expected by the end of 2030.

- December 2025: INEOS announced a major £150 million investment to underpin the long-term future of its Grangemouth site in Scotland, one of the UK’s most important industrial assets and a critical hub for the nation’s manufacturing and energy sectors.

- February 2025: GACL dispatched the first consignment of Poly Aluminium Chloride (PAC) 30 Powder from its new 9,900 metric ton per annum plant at the Coelho Complex, Vadodara. GACL's dedicated 1,05,000 TPA New Chloromethanes Complex positions GACL as India's largest integrated chloromethane producer, strengthening its supply capability to India's rapidly expanding pharmaceutical, agrochemical, and specialty chemicals markets.

Top Companies in the Chloromethane Market

- AkzoNobel N.V. (Amsterdam, Netherlands), as the global market leader with over 17% market share, commands an unrivaled position in chloromethane through its Frankfurt production hub. Its portfolio spans methyl chloride, methylene chloride, and chloroform, serving silicone manufacturers, pharmaceutical producers, and chemical intermediates customers across Europe, North America, and Asia. Its investment in energy-efficient production underscores long-term strategic commitment.

- Dow Chemical Company (Midland, Michigan, USA) is one of the world’s largest integrated producers of advanced materials and chemicals, with chloromethane central to its silicone product value chain. Its vertical integration, from chloromethane synthesis to silicone polymer production, provides a significant competitive moat. A 15% capacity expansion at its Texas facility in Q1 2024 signals continued strategic investment in this segment.

- Shin-Etsu Chemical Co., Ltd. (Tokyo, Japan), as the world’s largest PVC and silicone manufacturer, is among the most critical integrated consumers and producers of methyl chloride globally. Its investment in energy-efficient purification technology and the commissioning of a 200,000-ton/year chloromethane plant position the company as the Asia-Pacific’s foremost integrated chloromethane-silicone player, with a dominant regional share.

Companies Covered in Chloromethane Market

- AkzoNobel N.V. (Nouryon)

- Dow Chemical Company

- INEOS Group

- Solvay S.A.

- Shin-Etsu Chemical Co., Ltd.

- AGC Inc.

- Tokuyama Corporation

- KEM ONE

- Ercros S.A.

- SRF Limited

- Shandong Lubei Chemical Co., Ltd.

- Juhua Group

- Gujarat Alkalies and Chemicals Ltd.

Frequently Asked Questions

The global Chloromethane market is valued at US$ 5.8 Bn in 2026 and is projected to reach US$ 8.2 Bn by 2033, growing at a forecast CAGR of 5.1%. This is supported by a 4.0% historical CAGR recorded between 2020 and 2025, reflecting consistent industrial demand across pharmaceuticals, silicones, and agrochemicals.

The primary growth driver is the surging global demand for silicone polymers, which account for approximately 40% of total chloromethane consumption. As per the Global Silicones Council, an estimated 673,000 metric tons of silicone products are sold to the construction sector annually. Expanding applications in electric vehicles and renewable energy systems are creating additional demand momentum throughout the forecast period.

Methyl chloride is the dominant product type, commanding approximately 45% of market share by value in 2025. Its primacy is driven by its critical role as the feedstock for methyl chlorosilane synthesis, the precursor to all major silicone polymer families, and its versatility as a methylating and chlorinating agent across agrochemicals, cellulose ethers, and specialty chemical production.

Asia-Pacific is the leading region, accounting for over 45% of global chloromethane consumption. The region’s leadership is anchored in China’s expansive silicone manufacturing base, India’s growth in the pharmaceutical and agrochemical sectors, and Japan’s electronics and specialty chemicals industries. The region also recorded a 43% increase in production capacity since 2018, reinforcing its structural dominance.

The most significant emerging opportunity lies in the global transition to electric vehicles and renewable energy systems, creating structurally new demand for silicone products derived from chloromethane. Demand for silicone in solar panel encapsulants and EV battery thermal management systems is projected to grow at an annual rate exceeding 8% through 2030 (IRENA). Additionally, pharmaceutical API manufacturing expansion in India and China offers significant contract supply opportunities for high-purity chloromethane grades over the 2026-2033 forecast period.

The global chloromethane market is led by AkzoNobel N.V. (Nouryon), the market leader with over 17% global share, followed by Dow Chemical Company, INEOS Group, Solvay S.A., Shin-Etsu Chemical Co., Ltd., AGC Inc., Tokuyama Corporation, KEM ONE, Ercros S.A., SRF Limited, Shandong Lubei Chemical Co., Ltd., Juhua Group, and Gujarat Alkalies and Chemicals Ltd. The top eight players collectively control over 70% of global market capacity.