- Automotive Components & Materials

- Automotive Flywheel Market

Automotive Flywheel Market Size, Share, and Growth Forecast, 2026 – 2033

Automotive Flywheel Market by Flywheel Type (Single Mass Flywheel (SMF), Dual Mass Flywheel (DMF), Others), Material Type (Cast Iron, Steel, Aluminum, Others), Vehicle Type (Passenger Cars, Heavy Commercial Vehicles (HCVs), Off-Highway Vehicles), and Regional Analysis for 2026-2033

Automotive Flywheel Market Share and Trends Analysis

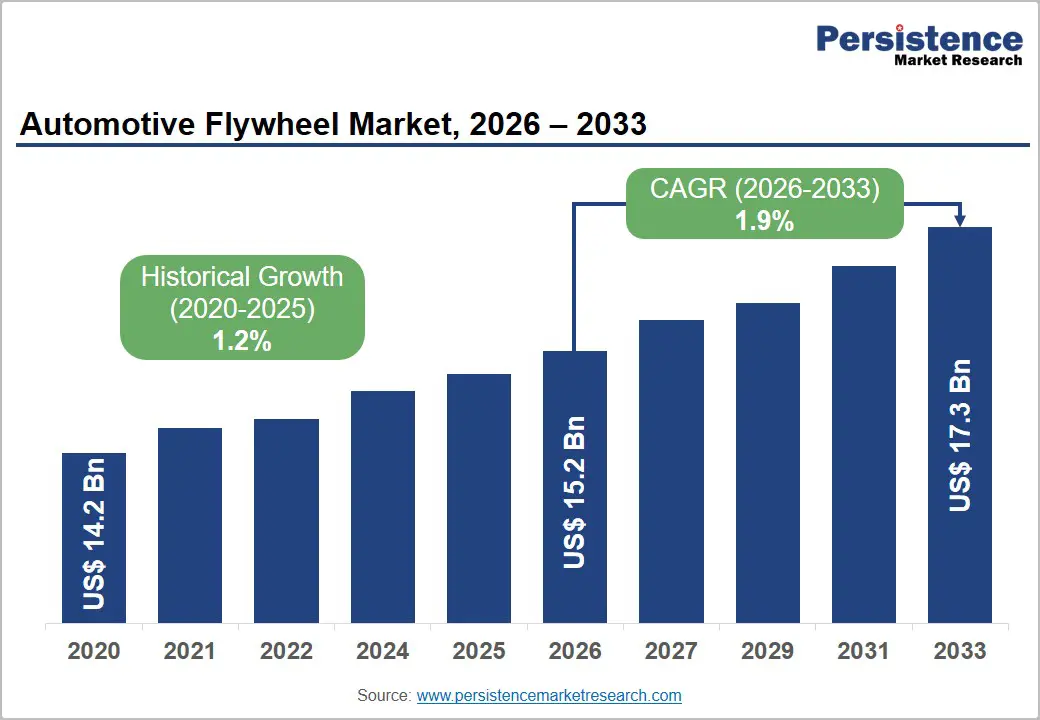

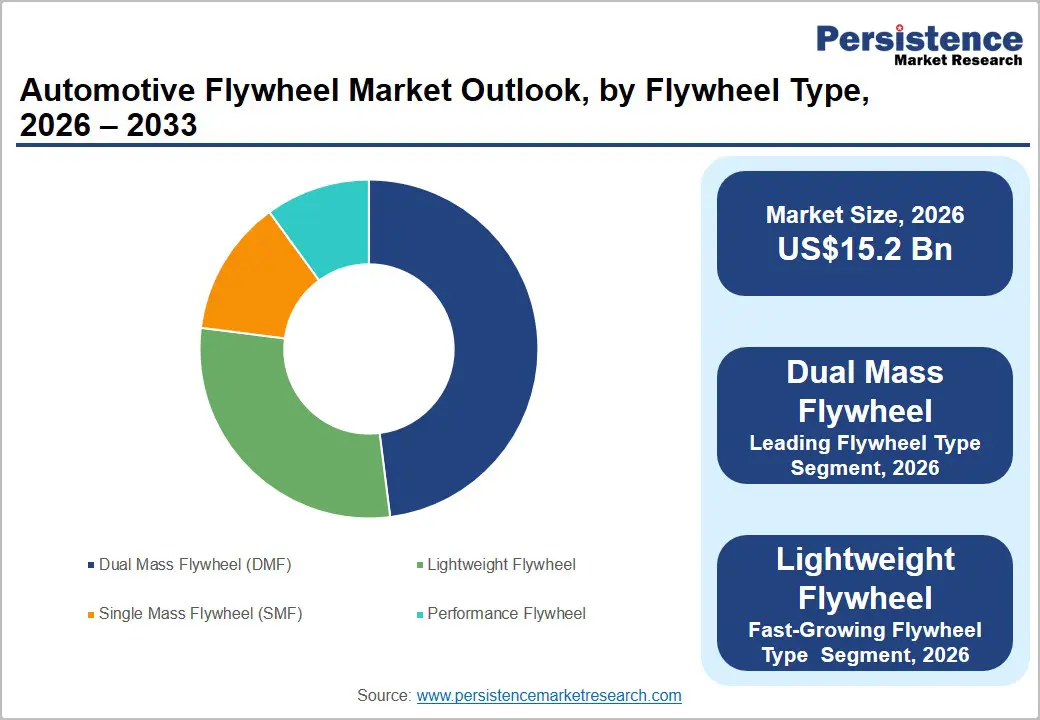

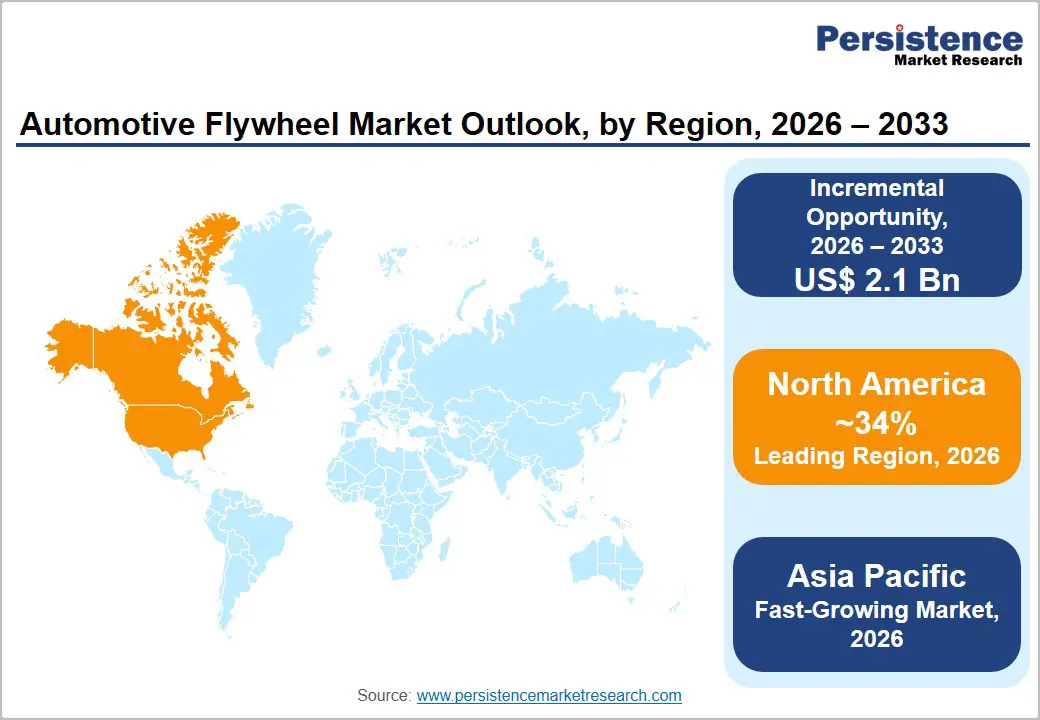

The global automotive flywheel market size is likely to be valued at US$15.2 billion in 2026 and is estimated to reach US$17.3 billion by 2033, growing at a CAGR of 1.9% during the forecast period from 2026 to 2033, driven by rising vehicle production volumes across emerging economies and tightening fuel efficiency regulations.

Growing middle-class populations in Asia Pacific create sustained demand for passenger vehicles equipped with manual and automated transmission systems. Regulatory bodies enforcing stricter emission norms push automakers toward dual mass flywheel adoption for noise and vibration reduction.

Key Industry Highlights

- Leading Flywheel Type: Dual mass flywheel is set to hold around 48% revenue share in 2026, driven by widespread adoption for noise reduction across passenger vehicle platforms.

- Fastest-growing Flywheel Type: Lightweight flywheel is projected as the fastest-growing segment, supported by expanding hybrid vehicle transmission integration.

- Leading Material Type: Cast iron is estimated to hold roughly a 52% revenue share in 2026, due to cost-effective durability across heavy-duty applications.

- Fastest-growing Material Type: Aluminum is forecast to record the fastest growth, driven by lightweight material adoption for fuel efficiency improvement.

- Regional Leadership: North America is projected to capture roughly 34% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to expanding vehicle production.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players including Dana Incorporated and ZF Friedrichshafen leveraging supply chain integration and regional manufacturing presence.

DRO Analysis

Driver - Rising Vehicle Production Supports Flywheel Component Demand

Global vehicle production expansion creates direct demand for transmission components, including flywheels. The United States Bureau of Transportation Statistics reported registered highway vehicles exceeding 290 million units in 2025, reflecting sustained fleet replacement cycles. Replacement and new vehicle assembly activity generate parallel demand for flywheel units across manual and automated transmission platforms, supporting consistent order volumes for component manufacturers throughout the forecast period.

Manufacturers respond to production increases by expanding casting and forging capacity for flywheel components. Original equipment manufacturers integrate flywheel sourcing into broader transmission supply contracts. This integration creates predictable demand patterns for tier one suppliers, allowing capacity planning aligned with vehicle assembly schedules across major production hubs in Asia Pacific and North America.

Restraint - Electric Vehicle Transition Reduces Long-Term Component Demand

Battery electric vehicle architectures eliminate traditional flywheel requirements in powertrain assemblies. This structural shift reduces addressable market scope for conventional flywheel manufacturers focused on internal combustion engine platforms.

Manufacturers face reduced order volumes from automakers transitioning production lines toward electric platforms. Supply chain dependency on internal combustion engine programs creates exposure to declining production allocations, limiting long term capacity utilization for flywheel-focused component facilities.

Opportunity - Lightweight Flywheel Development Expands Hybrid Vehicle Applications

Hybrid vehicle architectures require flywheel components optimized for combined combustion and electric drive integration. Lightweight flywheel designs using aluminum and composite materials reduce rotational mass, improving energy recovery efficiency. Manufacturers investing in lightweight material engineering position component portfolios for hybrid platform integration across passenger and light commercial vehicle segments globally.

Policy support for hybrid vehicle adoption in transitional markets creates expansion pathways for lightweight flywheel suppliers. Government incentive programs targeting hybrid powertrain production encourage component localization. Manufacturers establishing lightweight flywheel production facilities near hybrid assembly hubs gain logistical advantages, supporting market expansion into emerging hybrid vehicle manufacturing regions across Asia Pacific.

Category-wise Analysis

Flywheel Type Insights

Dual mass flywheel is anticipated to secure around 48% of the automotive flywheel market share in 2026, reflecting widespread adoption across passenger vehicle platforms for noise reduction. Volkswagen integrates dual mass flywheel systems across diesel transmission lines for vibration dampening. Adoption continues expanding as manufacturers prioritize cabin comfort standards across compact and midsize vehicle segments globally.

The lightweight flywheel is expected to be the fastest-growing segment, propelled by demand for fuel-efficient transmission components in hybrid platforms. Toyota incorporates lightweight flywheel designs within hybrid synergy drive transmission assemblies. Material innovation in aluminum casting techniques supports broader adoption across compact hybrid vehicle production lines through the forecast period.

Material Type Insights

Cast iron is poised to dominate with a forecast market share of over 52% in 2026, powered by cost-effective manufacturing processes and durability characteristics suited for heavy-duty applications. Ford utilizes cast iron flywheels within commercial truck transmission assemblies. Established casting infrastructure supports continued cast iron preference across high-torque vehicle platforms.

Aluminum is estimated to be the fastest-growing segment, fueled by increasing adoption of lightweight drivetrain technologies aimed at improving fuel economy and vehicle performance. Material advancements enable stronger and more durable lightweight designs suitable for modern automotive applications. For example, several performance vehicle programs employ aluminum flywheels to enhance throttle response. Growing emphasis on efficiency optimization and emissions reduction encourages broader integration throughout the forecast period.

Vehicle Type Insights

Passenger cars are likely to be the leading segment with a projected 61% of the automotive flywheel market share in 2026 due to high production volumes across global assembly plants. Hyundai produces flywheel-equipped manual transmission units across compact sedan platforms. Sustained passenger vehicle demand supports continued segment leadership through the forecast period.

Light commercial vehicles are anticipated to be the fastest-growing segment, fueled by expanding logistics and last-mile delivery fleet requirements. Tata Motors integrates flywheel components within light commercial vehicle transmission assemblies for urban delivery applications. Fleet expansion across e-commerce logistics networks supports accelerated segment growth.

Regional Insights

North America Automotive Flywheel Market Trends

North America is expected to lead with an estimated 34% of the global market share in 2026, supported by a large vehicle parc, strong commercial vehicle demand, and continued production of internal combustion engine vehicles. Investments in advanced drivetrain technologies and replacement component demand sustain consumption. Major manufacturers continue focusing on vibration reduction and fuel-efficiency improvements, supporting adoption of dual-mass and lightweight flywheel systems.

U.S. Automotive Flywheel Market Insights

The U.S. is projected to account for approximately 81% of the North America market share in 2026, driven by strong passenger vehicle production, extensive aftermarket activity, and growing light commercial vehicle utilization. Manufacturing investments by automotive companies and drivetrain component suppliers contribute to the stable procurement of advanced flywheel assemblies.

Canada Automotive Flywheel Market Insights

Canada is forecast to hold nearly 19% of the North America market share in 2026. Commercial transportation activity, automotive manufacturing operations in Ontario, and demand for replacement drivetrain components support growth. Ongoing modernization of vehicle fleets encourages adoption of durable and fuel-efficient flywheel technologies.

Europe Automotive Flywheel Market Trends

Europe is projected to capture around 29% of the global market share in 2026, driven by widespread adoption of dual-mass flywheel systems and stringent fuel-efficiency regulations. Strong engineering capabilities, advanced automotive manufacturing infrastructure, and continuous vehicle technology upgrades support demand. Premium vehicle production contributes significantly to the utilization of sophisticated vibration-control solutions.

Germany Automotive Flywheel Market Insights

Germany is expected to contribute approximately 27% of the Europe market share in 2026. High vehicle production volumes, strong presence of premium automotive brands, and continuous drivetrain innovation stimulate demand. Investments in advanced transmission technologies encourage the integration of high-performance flywheel systems.

France Automotive Flywheel Market Insights

France is likely to account for nearly 15% of the Europe market share in 2026. Continued production of passenger vehicles and emphasis on fuel-efficient mobility solutions support component demand. Automotive manufacturers remain focused on reducing drivetrain vibration and improving operating efficiency through advanced flywheel integration.

Asia Pacific Automotive Flywheel Market Trends

Asia Pacific is forecast to be the fastest-growing regional market, stimulated by expanding vehicle production, rising vehicle ownership, and increasing industrial activity. Large-scale manufacturing facilities, growing commercial transportation requirements, and ongoing infrastructure development create substantial demand for drivetrain components.

China Automotive Flywheel Market Insights

China is projected to account for nearly 36% of the Asia Pacific share in 2026. Extensive passenger car production, strong commercial vehicle manufacturing capacity, and continued investments in automotive technology support demand. Growth in domestic vehicle sales and replacement parts consumption reinforces market expansion.

India Automotive Flywheel Market Insights

India is forecast to contribute approximately 21% of the Asia Pacific market share in 2026. Rising vehicle ownership, expanding logistics networks, and increasing production of passenger and commercial vehicles support adoption. Government initiatives promoting manufacturing expansion and automotive localization strengthen demand for flywheel systems across original equipment and aftermarket channels.

Competitive Landscape

The global automotive flywheel market is moderately fragmented, with established suppliers including Dana Incorporated, ZF Friedrichshafen, Valeo, Aisin Corporation, and Schaeffler Group maintaining competitive positions across regional transmission component supply chains globally.

Regional manufacturers compete alongside global suppliers within specific vehicle platform segments. Original equipment supply contracts distribute production volumes across multiple component manufacturers, limiting concentration within passenger vehicle transmission supply networks worldwide.

Key Industry Developments:

- In January 2026, Yuchai Group and Rolls-Royce Power Systems launched a flywheel range extender system for commercial vehicles, strengthening innovation in automotive flywheel technology.

Companies Covered in Automotive Flywheel Market

- Dana Incorporated

- ZF Friedrichshafen

- Valeo

- Aisin Corporation

- Schaeffler Group

- Eaton Corporation

- BorgWarner Inc

- Exedy Corporation

- Mahle GmbH

- AP Racing

- Spec Clutch

Frequently Asked Questions

The global automotive flywheel market is projected to reach US$15.2 billion in 2026.

Rising vehicle production, growing demand for fuel-efficient powertrains, and increasing adoption of advanced drivetrain technologies drive the automotive flywheel market.

The automotive flywheel market is poised to witness a CAGR of 1.9% from 2026 to 2033.

Growing adoption of lightweight flywheels, expanding demand for dual-mass flywheel systems, and advancements in fuel-efficient drivetrain technologies create key opportunities in the automotive flywheel market.

Some of the key market players include Dana Incorporated, ZF Friedrichshafen, Valeo, Aisin Corporation, and Schaeffler Group.