- Executive Summary

- Global Anesthetics Delivery Pens Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-economic Factors

- Global Sectoral Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Tool Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Analysis, 2026A

- Key Highlights

- Key Factors Impacting Deployment Costs

- Pricing Analysis, By Product Type

- Global Anesthetics Delivery Pens Market Outlook

- Key Highlights

- Market Volume (Units) Projections

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2026-2026

- Market Size (US$ Bn) Analysis and Forecast, 2026 - 2033

- Global Anesthetics Delivery Pens Market Outlook: Product Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Product Type, 2026 - 2026

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Manual Pens

- Computer-Controlled Local Anesthetic Delivery (CCLAD)

- Needle-Free Injectors

- Market Attractiveness Analysis: Product Type

- Global Anesthetics Delivery Pens Market Outlook: Technology

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Technology, 2026 - 2026

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2026 - 2033

- Flow-Controlled Systems

- Pressure-Sensing Systems

- Multi-Mode Systems

- Market Attractiveness Analysis: Technology

- Global Anesthetics Delivery Pens Market Outlook: Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application, 2026 - 2026

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026 - 2033

- Dental

- Dermatology

- Surgical

- Market Attractiveness Analysis: Application

- Key Highlights

- Global Anesthetics Delivery Pens Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Region, 2026 - 2026

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Region, 2026 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Anesthetics Delivery Pens Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2026 - 2026

- By Country

- By Product Type

- By Technology

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- U.S.

- Canada

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Manual Pens

- Computer-Controlled Local Anesthetic Delivery (CCLAD)

- Needle-Free Injectors

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2026 - 2033

- Flow-Controlled Systems

- Pressure-Sensing Systems

- Multi-Mode Systems

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Dental

- Dermatology

- Surgical

- Market Attractiveness Analysis

- Europe Anesthetics Delivery Pens Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2026 - 2026

- By Country

- By Product Type

- By Technology

- Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Manual Pens

- Computer-Controlled Local Anesthetic Delivery (CCLAD)

- Needle-Free Injectors

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2026 - 2033

- Flow-Controlled Systems

- Pressure-Sensing Systems

- Multi-Mode Systems

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Dental

- Dermatology

- Surgical

- Market Attractiveness Analysis

- East Asia Anesthetics Delivery Pens Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2026 - 2026

- By Country

- By Product Type

- By Technology

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Manual Pens

- Computer-Controlled Local Anesthetic Delivery (CCLAD)

- Needle-Free Injectors

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2026 - 2033

- Flow-Controlled Systems

- Pressure-Sensing Systems

- Multi-Mode Systems

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Dental

- Dermatology

- Surgical

- Market Attractiveness Analysis

- South Asia & Oceania Anesthetics Delivery Pens Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2026 - 2026

- By Country

- By Product Type

- By Technology

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Manual Pens

- Computer-Controlled Local Anesthetic Delivery (CCLAD)

- Needle-Free Injectors

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2026 - 2033

- Flow-Controlled Systems

- Pressure-Sensing Systems

- Multi-Mode Systems

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Dental

- Dermatology

- Surgical

- Market Attractiveness Analysis

- Latin America Anesthetics Delivery Pens Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2026 - 2026

- By Country

- By Product Type

- By Technology

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Manual Pens

- Computer-Controlled Local Anesthetic Delivery (CCLAD)

- Needle-Free Injectors

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2026 - 2033

- Flow-Controlled Systems

- Pressure-Sensing Systems

- Multi-Mode Systems

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Dental

- Dermatology

- Surgical

- Market Attractiveness Analysis

- Middle East & Africa Anesthetics Delivery Pens Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2026 - 2026

- By Country

- By Product Type

- By Technology

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 - 2033

- Manual Pens

- Computer-Controlled Local Anesthetic Delivery (CCLAD)

- Needle-Free Injectors

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2026 - 2033

- Flow-Controlled Systems

- Pressure-Sensing Systems

- Multi-Mode Systems

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Dental

- Dermatology

- Surgical

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2026

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- Milestone Scientific Inc.

- Overview

- Segments and Deployments

- Key Financials

- Market Developments

- Market Strategy

- Septodont Holding

- Dentsply Sirona

- 3M Company

- Zyris Inc.

- Comfort-in

- PharmaJet

- Injex Pharma AG

- Henke-Sass, Wolf GmbH

- Medtronic plc

- Becton, Dickinson and Company

- Terumo Corporation

- Nipro Corporation

- Ultradent Products Inc.

- Milestone Scientific Inc.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Medical Devices

- Anesthetics Delivery Pens Market

Anesthetics Delivery Pens Market Size, Share and Growth Analysis, 2026 - 2033

Anesthetics Delivery Pens Market by Product Type (Manual Pens, Computer-Controlled Local Anesthetic Delivery (CCLAD)), Needle-Free Injectors), Technology (Flow-Controlled, Pressure-Sensing, Multi-Mode Systems), Application (Dental, Dermatology, Surgical), and Regional Analysis for 2026 - 2033

Key Industry Highlights

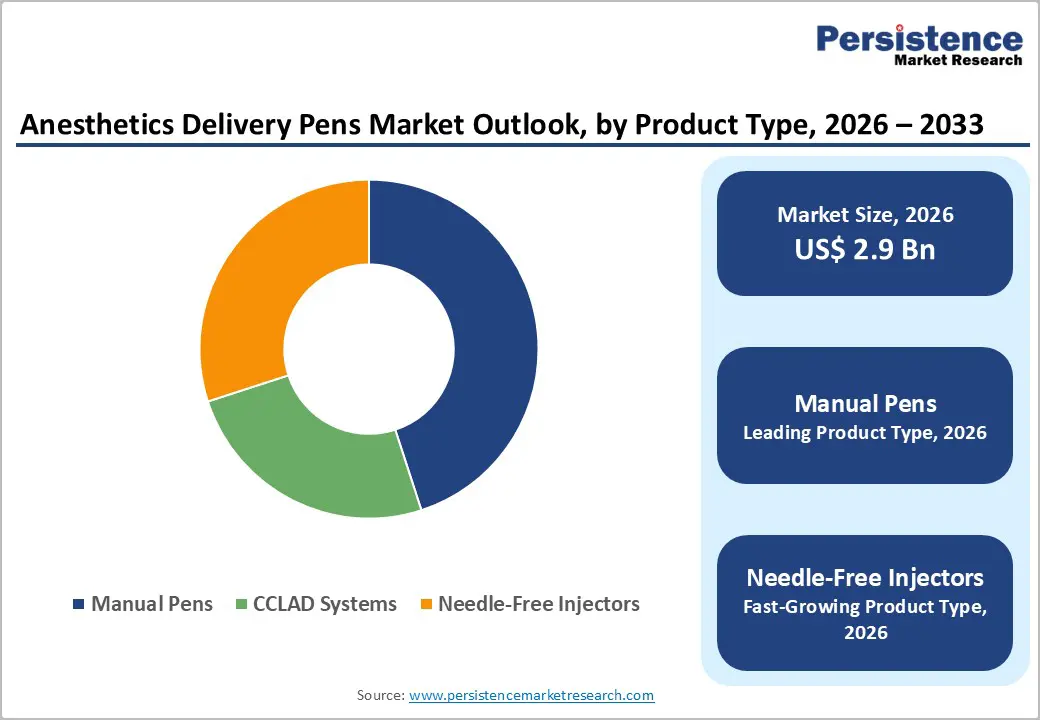

- Dominant Product Type: Manual pens are projected to command around 45% revenue share in 2026, while needle-free injectors are expected to be the fastest-growing at approximately 14.5% CAGR through 2033, driven by increasing demand for pain-free and infection-free drug delivery solutions.

- Dominant Technologies: Flow-controlled systems are projected to command around 40% revenue share in 2026, while multi-mode systems are expected to be the fastest-growing at approximately 13.8% CAGR through 2033, driven by their flexibility across multiple clinical applications.

- Leading Applications: Dental applications are anticipated to lead with an estimated 38% share in 2026, while dermatology/aesthetic applications are likely to be the fastest-growing at about 14.2% CAGR during 2026–2033, supported by the surge in cosmetic and minimally invasive procedures.

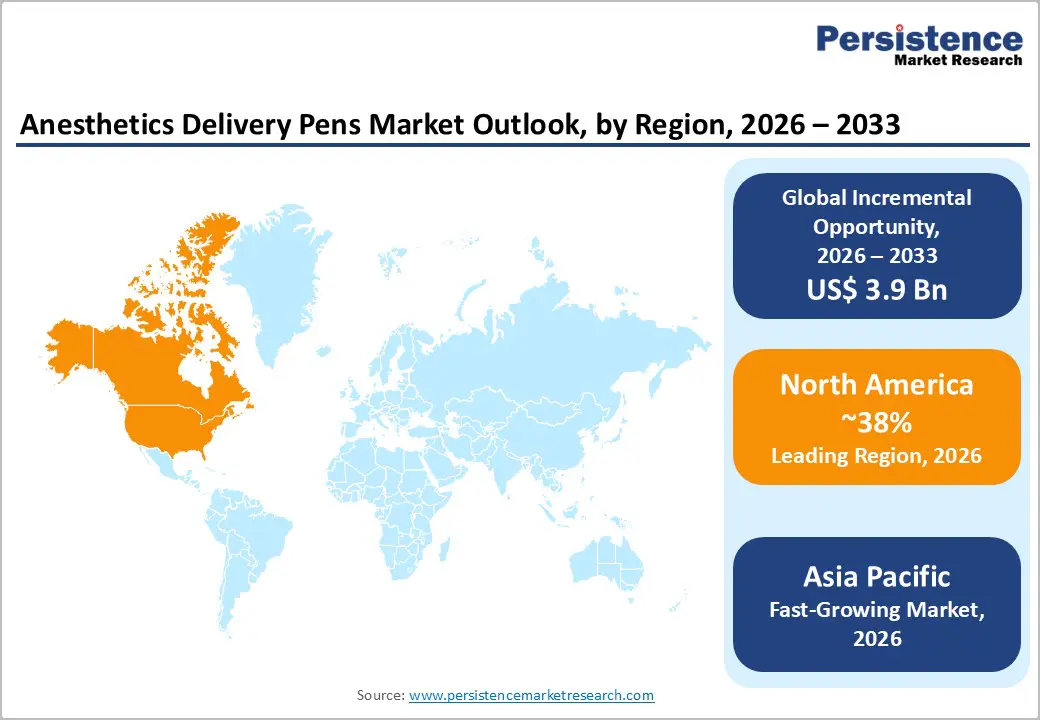

- Regional Leadership: North America is poised to dominate with an estimated 38% share in 2026, while Asia Pacific is expected to register the fastest growth at over 14% CAGR through 2033, fueled by expanding healthcare infrastructure and rising patient volumes.

- Competitive Dynamics: Market competition is getting increasingly characterized by product innovation, mergers and acquisitions, and expansion into Asia Pacific and Latin America by companies to strengthen their global footprint.

| Key Insights | Details |

|---|---|

|

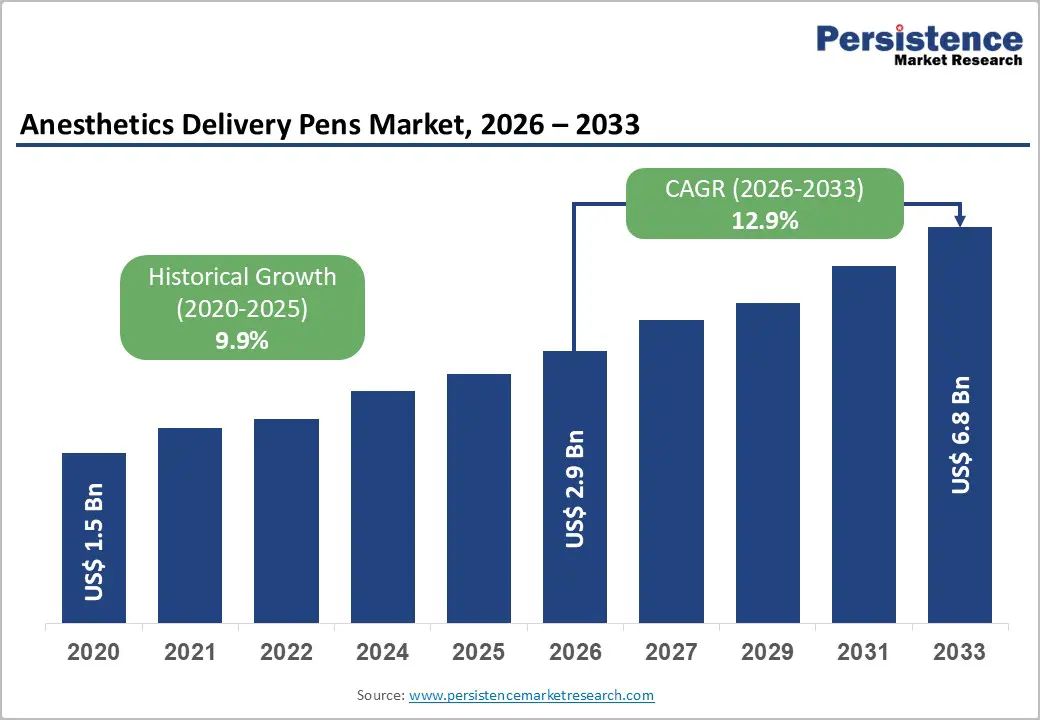

Anesthetics Delivery Pens Market Size (2026E) |

US$ 2.9 Bn |

|

Market Value Forecast (2033F) |

US$ 6.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

12.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.9% |

DRO Analysis

Surging Volume of Dental, Aesthetic, and Surgical Procedures

According to the World Health Organization (WHO), oral diseases affect nearly 3.5 billion people globally, with dental procedures steadily increasing in both developed and emerging economies. The American Society of Plastic Surgeons (ASPS) reported over 26 million cosmetic procedures in 2023, with continued growth into 2025, reflecting strong demand for minimally invasive treatments. These procedures require precise, pain-minimized anesthetic delivery, directly increasing demand for advanced delivery pens, especially in outpatient settings. Expanding public health initiatives and decentralized care models, supported by agencies such as the U.S. Centers for Disease Control and Prevention (CDC), are increasing procedural volumes in clinics and ambulatory centers, ensuring consistent demand, strengthening recurring revenue streams, and encouraging manufacturers to develop specialized solutions across dental, dermatology, and surgical applications.

Beyond dental and aesthetic care, the rise in surgical procedures is reinforcing demand at a broader healthcare level. The United Nations Department of Economic and Social Affairs (UN DESA) estimates that the global population aged 65+ will reach 1.6 billion by 2050, significantly increasing the need for surgical interventions and pain management solutions. At the same time, surgical volumes continue to grow steadily across major economies due to improved healthcare access and infrastructure expansion. This demographic and procedural shift is creating sustained demand for reliable anesthetic delivery solutions that enhance safety and precision, particularly in elderly patient populations, while also supporting long-term revenue visibility for manufacturers operating in high-growth clinical segments.

Technological Advancements in Precision Drug Delivery Systems

Innovations such as computer-controlled local anesthetic delivery (CCLAD) and pressure-sensing technologies have significantly improved dosing accuracy and patient comfort. Data from the U.S. Food and Drug Administration (FDA) device approvals (2023–2025) indicates a steady rise in advanced delivery systems entering the market, reflecting growing regulatory support for innovation. These technologies enable controlled flow rates, automated pressure regulation, and real-time feedback, minimizing human error and improving clinical outcomes across procedures. As healthcare providers increasingly prioritize precision and patient experience, adoption of such systems is rising across dental clinics and surgical centers, accelerating the replacement of traditional syringes and enabling higher-value product adoption.

Industry developments over the past years have strongly reinforced this technological transition toward smarter systems. Recent FDA clearances for next-generation syringe-less injector platforms highlight advancements in automation, interoperability, and dosing efficiency, indicating rapid innovation in delivery mechanisms. Additionally, new needle-free injection systems introduced in 2025 feature integrated cartridge-based designs that simplify administration and reduce contamination risks, improving overall safety standards. Innovations showcased at global technology platforms in 2025 also emphasize microfluidic and needle-free approaches aimed at eliminating needle-related discomfort and injuries, thereby improving workflow efficiency, enabling premium pricing, and strengthening competitive positioning for technology-focused manufacturers.

High Cost of Advanced Delivery Systems

Advanced systems such as CCLAD and needle-free injectors can cost 3–5 times more than conventional syringes, creating affordability challenges, particularly in low- and middle-income countries. In 2025, procurement data from public healthcare systems in Asia and Africa indicated budget constraints limiting adoption of premium devices, especially in government-funded hospitals and community clinics. This cost disparity becomes more critical in high-volume care environments where affordability and scalability are key decision factors. As a result, many healthcare providers continue to rely on traditional, lower-cost alternatives despite the clinical advantages offered by advanced delivery technologies, reinforcing uneven adoption patterns across regions.

The pricing barrier is further compounded by ongoing medical device supply chain and cost pressures highlighted by regulatory bodies such as the U.S. FDA, which has emphasized vulnerabilities affecting device availability and affordability. These challenges, combined with inflationary pressures on healthcare budgets in 2025, have forced providers to prioritize essential procurement over advanced technologies. Impact: Cost sensitivity restricts penetration in emerging markets, slows the transition toward technologically advanced systems, and creates a fragmented demand landscape where premium products remain concentrated in developed regions.

Regulatory and Compliance Challenges

Medical devices must comply with stringent regulatory frameworks such as FDA, CE marking, and Central Drugs Standard Control Organisation (CDSCO) approvals, which involve extensive clinical validation, safety testing, and documentation. In 2025, several device recalls in the broader drug delivery category highlighted risks associated with device malfunction and calibration errors, reinforcing the importance of strict regulatory oversight. Notably, the FDA expanded its medical device recall communication program to strengthen post-market surveillance and risk reporting. These developments underscore the increasing scrutiny on device performance, particularly for systems involved in drug delivery and patient safety.

Recent high-profile recall events further illustrate the regulatory burden and associated risks. For instance, in March 2026, a drug delivery-related device correction involving insulin delivery pods was initiated due to a manufacturing defect affecting dosing accuracy, highlighting real-world risks of system failures. Additionally, multiple Class I recalls reported in 2025 across medical devices emphasize the severity of potential failures and their impact on patient safety. Impact: Lengthy approval timelines and high compliance costs increase operational risks, delay product launches, and create entry barriers for smaller players, ultimately affecting innovation speed and overall market expansion.

Expansion in Emerging Markets and Healthcare Infrastructure Development

Countries such as India, China, and Brazil are increasing healthcare spending. The World Bank reports healthcare expenditure in emerging economies growing at 6–8% annually, reflecting sustained investment in healthcare infrastructure and accessibility. Governments across these regions are also prioritizing primary care expansion and surgical capacity building, which directly increases the need for efficient anesthetic delivery systems across hospitals and outpatient settings, creating a strong foundation for long-term market penetration.

Recent developments further support this trend. The government-led healthcare initiatives, such as India’s expanded public health infrastructure programs and China’s hospital modernization efforts, have accelerated access to surgical and outpatient care services. Additionally, coverage by leading outlets such as BBC News and Reuters highlights rising investments in healthcare capacity and medical device accessibility across emerging economies. Manufacturers can leverage cost-optimized solutions, localized production, and strategic partnerships to capture untapped demand, improve accessibility, and establish strong footholds in rapidly evolving healthcare ecosystems.

Adoption of Needle-Free and Smart Drug Delivery Technologies

Needle-free injectors are gaining traction due to reduced infection risk and improved patient comfort. The U.S. CDC has emphasized minimizing needle-stick injuries, which affect over 385,000 healthcare workers annually in the U.S., highlighting the need for safer alternatives. At the same time, the integration of IoT-enabled and AI-assisted delivery systems is emerging, with several medtech firms introducing prototypes in 2025 featuring real-time dosage tracking and patient data integration. These advancements are reshaping clinical workflows by improving precision, safety, and monitoring capabilities across healthcare settings.

Industry movements strongly validate this shift toward safer and smarter delivery technologies. Reports from the U.S. FDA and coverage by Reuters highlight increasing regulatory focus on reducing device-related risks and improving patient safety through innovation. Additionally, global healthcare discussions in 2025 emphasized reducing needle-stick injuries and promoting non-invasive delivery methods in clinical settings. The convergence of safety-driven innovation and digital health integration is accelerating adoption, enabling premium pricing models and potentially generating 10–15% incremental revenue streams for manufacturers operating in this high-growth, technology-driven segment.

Category-wise Analysis

Product Type Insights

Manual pens are likely to continue leading with approximately 45% of the anesthetics delivery pens market revenue share in 2026, primarily due to their cost-effectiveness, operational simplicity, and widespread accessibility across both developed and developing healthcare systems. These devices remain essential in high-volume clinical environments such as dental and primary care settings, where affordability and ease of use are critical. Their compatibility with existing workflows and minimal training requirements further strengthen their adoption in public healthcare systems. In 2025, innovation within this segment was reinforced by the U.S. FDA’s broader push toward AI-enabled and performance-evaluated medical devices, indicating a shift toward improving even conventional delivery tools with smarter monitoring and safety features. This supports the continued evolution of manual pens while maintaining their affordability advantage.

The needle-free injectors are anticipated as the fastest-growing segment, projected to expand at a CAGR of around 14.5% through 2033, driven by rapid innovation and expanding clinical applications. In June 2025, a breakthrough anesthetic delivery system (DentalJect) received regulatory clearance, introducing a non-invasive cryogenic spray mechanism that numbs oral tissue within seconds, eliminating the need for traditional needle-based pre-anesthesia. Clinical studies continue to highlight the benefits of needle-free anesthesia, including the elimination of injection pain and improved patient compliance. These developments demonstrate a clear transition toward non-invasive, high-precision delivery systems, accelerating adoption across advanced clinical environments.

Application Insights

Dental applications are expected to dominate the market, accounting for approximately 38% of the anesthetics delivery pens market share in 2026, driven by the high frequency of procedures such as fillings, root canals, and extractions. Dentistry remains one of the most procedure-intensive medical fields, requiring consistent use of local anesthetics for pain management. The increasing burden of oral health conditions and the expansion of preventive care programs continue to support strong procedural volumes globally. In 2025, regulatory focus by the U.S. FDA included updated guidance and evaluation frameworks for dental-related devices and implants, reflecting increased oversight and innovation in dental treatment technologies. This indicates a strengthening clinical ecosystem that supports sustained demand for anesthetic delivery systems in routine dental practice.

The dermatology segment is poised to be the fastest-growing application area, expected to expand at a CAGR of approximately 14.2% during 2026–2033, fueled by rapid innovation and rising consumer demand for minimally invasive treatments. The advancements in needle-free jet injection technologies were increasingly highlighted for their ability to deliver anesthesia through high-pressure streams without skin penetration, improving comfort and reducing procedure-related anxiety. Additionally, regulatory and clinical attention toward non-invasive and patient-friendly treatment modalities continues to accelerate adoption in cosmetic dermatology. These developments are strengthening the role of advanced anesthetic delivery systems in aesthetic procedures, supporting sustained high growth in this segment.

Regional Insights

North America Anesthetics Delivery Pens Market Trends

North America is expected to account for approximately 38% of the anesthetics delivery pens market value in 2026, driven primarily by the United States. The region benefits from advanced healthcare infrastructure, high procedural volumes, and strong adoption of innovative technologies across dental, dermatology, and surgical applications. The U.S. market is supported by favorable reimbursement frameworks and widespread use of precision-based delivery systems. In 2025, leading dental technology company Dentsply Sirona expanded its digital and minimally invasive solutions portfolio, reinforcing demand for precise anesthetic delivery systems in clinical workflows. This reflects a broader shift toward efficiency and patient-centric care in outpatient and ambulatory settings.

The region also maintains a strong innovation ecosystem supported by corporate investments and technological advancements. In 2026, Becton, Dickinson and Company advanced its drug delivery portfolio with a focus on improving injection safety and reducing device-related complications. Additionally, collaborations between healthcare providers and technology firms are accelerating the adoption of smart and connected delivery systems across hospitals and clinics. Strong R&D capabilities and consistent funding activity continue to support innovation across the region. These developments reinforce North America’s leadership position while creating opportunities for premium and high-value product adoption.

Europe Anesthetics Delivery Pens Market Trends

Europe represents a significant regional market, supported by well-established healthcare systems and consistent demand across key economies such as Germany, the U.K., France, and Spain. The region benefits from universal healthcare access, ensuring stable procedural volumes across dental, dermatology, and surgical applications. Germany plays a leading role in manufacturing and technology adoption, while the U.K. shows strong demand for dental and aesthetic procedures. In 2025, Septodont expanded its production capacity and distribution network across Europe, strengthening supply of dental anesthetics and related delivery solutions. This reflects growing procedural demand and the need for reliable anesthetic delivery technologies.

The regulatory environment in Europe continues to be shaped by the European Union (EU) Medical Device Regulation (MDR), which emphasizes product safety and quality standards. 3M Company strengthened its healthcare portfolio in the region through strategic restructuring and a focus on advanced medical solutions. Additionally, increasing collaboration between manufacturers and healthcare institutions is supporting the adoption of minimally invasive technologies. Despite compliance complexities, the region continues to promote innovation and patient safety. These factors collectively create opportunities for advanced anesthetic delivery systems across diverse clinical applications.

Asia Pacific Anesthetics Delivery Pens Market Trends

The Asia Pacific market is projected to record the highest 2026-2033 CAGR of approximately 14%, driven by rapid healthcare expansion and increasing patient demand. The region includes key markets such as China, Japan, India, and ASEAN countries, each contributing to overall growth through rising healthcare access and infrastructure development. China leads in manufacturing capabilities, while India is witnessing strong demand due to expanding healthcare services and a growing middle-class population. Terumo Corporation expanded its regional operations to strengthen the supply of drug delivery systems. These highlights increasing industry focus on Asia Pacific as a key growth hub.

The region also benefits from cost advantages, favorable manufacturing conditions, and growing medical tourism across several countries. In 2026, Nipro Corporation increased its investments in production facilities across Asia to meet rising domestic and export demand. Additionally, partnerships between global and regional players are improving the accessibility and affordability of advanced medical devices. Regulatory frameworks are evolving to support faster market entry while maintaining quality standards. These developments position Asia Pacific as a high-growth market with strong opportunities for scalable and cost-effective anesthetic delivery solutions.

Competitive Landscape

The global anesthetics delivery pens market structure is moderately consolidated, with leading players such as Dentsply Sirona, Septodont, Becton, Dickinson and Company, and 3M Company collectively accounting for a significant share of global revenue. These companies leverage strong distribution networks, established relationships with dental and healthcare providers, and diversified product portfolios spanning anesthetics and delivery systems. Their competitive advantage lies in continuous investment in precision delivery technologies, ergonomic device design, and integration of safety-enhancing features to meet evolving clinical requirements.

The specialized and regional players, such as Milestone Scientific and Terumo Corporation, are focusing on niche innovations, including computer-controlled delivery systems and advanced injection technologies. Market entry barriers remain moderate to high due to stringent regulatory approvals, clinical validation requirements, and the need for practitioner training, which limit rapid new entrant penetration. However, ongoing advancements in needle-free technologies and smart drug delivery systems are opening opportunities for emerging players and technology-driven firms. The competitive landscape is expected to evolve gradually, with established players pursuing strategic acquisitions, product innovation, and geographic expansion, while smaller companies increasingly collaborate through technology partnerships and distribution alliances.

Key Industry Developments

- In February 2026, Crossject SA progressed toward an FDA Emergency Use Authorization (EUA) for its ZENEO® needle-free auto-injector. The move is supported by a potential US$ 155 million U.S. government contract through BARDA for emergency stockpiling, highlighting both strong institutional backing and strategic importance in national preparedness programs.

- In January 2026, PharmaJet’s needle-free injection system was chosen to administer DNA-based immunotherapy for advanced melanoma following positive Phase-2 results. The company plans a registrational Phase-3 study in the second half of 2026, demonstrating the clinical versatility of its delivery platform and potential for broader therapeutic adoption.

- In September 2025, Portal Instruments and Gerresheimer AG expanded their collaboration to commercialize the PRIME Nexus™ reusable injector platform. This partnership combines innovative injector technology with global manufacturing scale, accelerating adoption in both chronic disease management and high-volume clinical settings.

Companies Covered in Anesthetics Delivery Pens Market

- Milestone Scientific Inc.

- Septodont Holding

- Dentsply Sirona

- 3M Company

- Zyris Inc.

- Comfort-in

- PharmaJet

- Injex Pharma AG

- Henke-Sass, Wolf GmbH

- Medtronic plc

- Becton, Dickinson and Company

- Terumo Corporation

- Nipro Corporation

- Ultradent Products Inc.

Frequently Asked Questions

The global anesthetics delivery pens market is projected to reach US$ 2.9 billion in 2026.

Rising demand for minimally invasive procedures, increasing dental and aesthetic treatments, and advancements in precision drug delivery technologies are key market drivers.

The market is poised to witness a CAGR of 12.9% from 2026 to 2033.

Expansion in emerging markets and growing adoption of needle-free and smart delivery systems present major opportunities.

Dentsply Sirona, Septodont, Becton, Dickinson and Company, and 3M Company are among the key players in the market.