- Animal Health

- Animal Healthcare Market

Animal Healthcare Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

Animal Healthcare Market by Drugs (Anti-Infective Agents, Anti-Inflammatory & Analgesic Agents, Parasiticides, Vaccines, Hormones & Substitutes, Nutritional Products, and Others), by Animals (Companion Animals, Farm Animals), by Route of Administration (Oral, Parenteral, Topical, and Others), by Distribution Channel, sand Regional Analysis from 2025 - 2032

Animal Healthcare Market Share and Trends Analysis

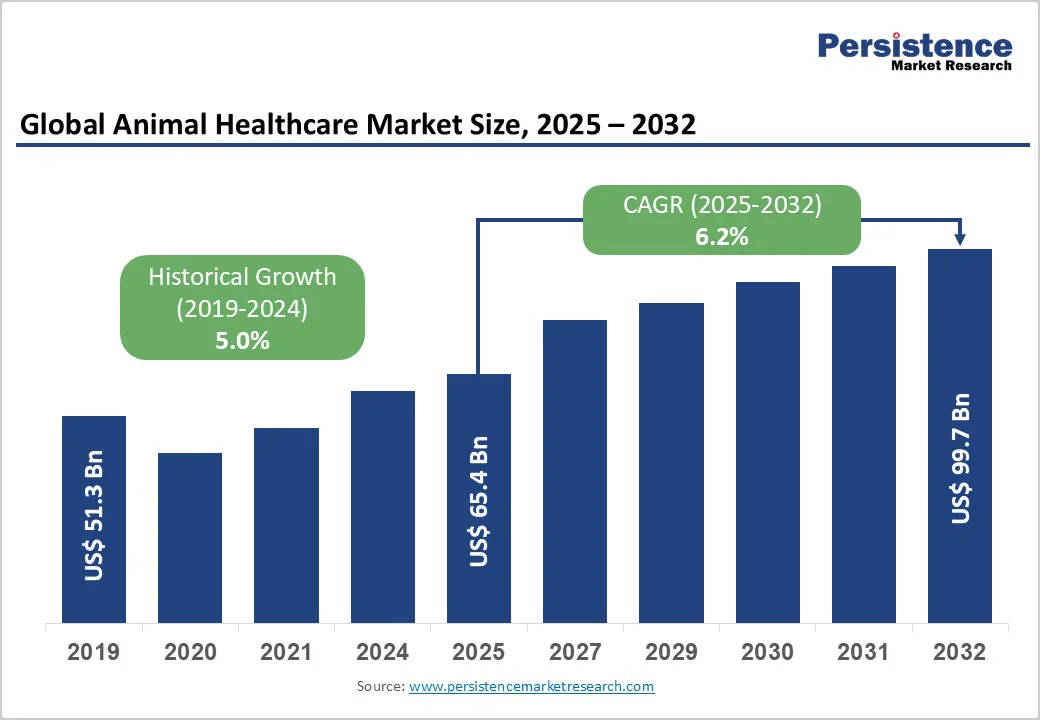

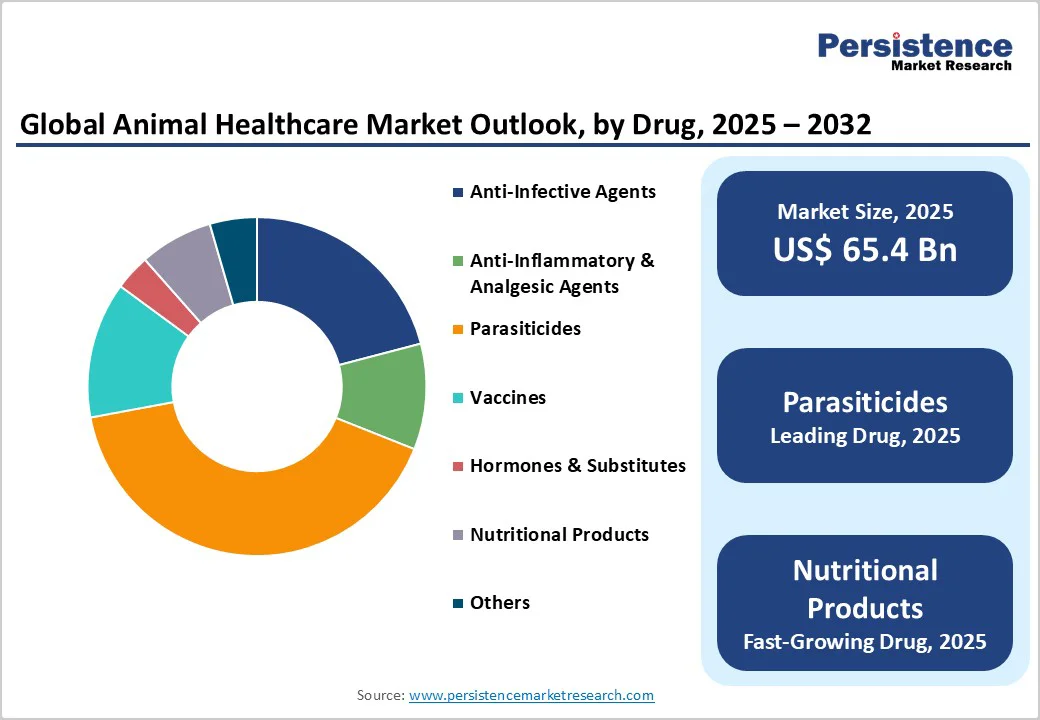

The global animal healthcare market size is valued at US$ 65.4 billion in 2025 and is projected to reach US$ 99.7 billion growing at a CAGR of 6.2% during the forecast period from 2025 to 2032.

Global demand for animal healthcare is increasing as the veterinary, pharmaceutical, and animal health industries expand the production of vaccines, biologics, and specialty therapeutics. Rising regulatory requirements for animal safety and quality, coupled with the growing adoption of advanced diagnostics and in-vitro testing methods, are fueling market growth. Additionally, the expansion of veterinary infrastructure, improved livestock management practices, and enhanced manufacturing capabilities in developing regions are increasing access to animal healthcare products and services.

Key Industry Highlights:

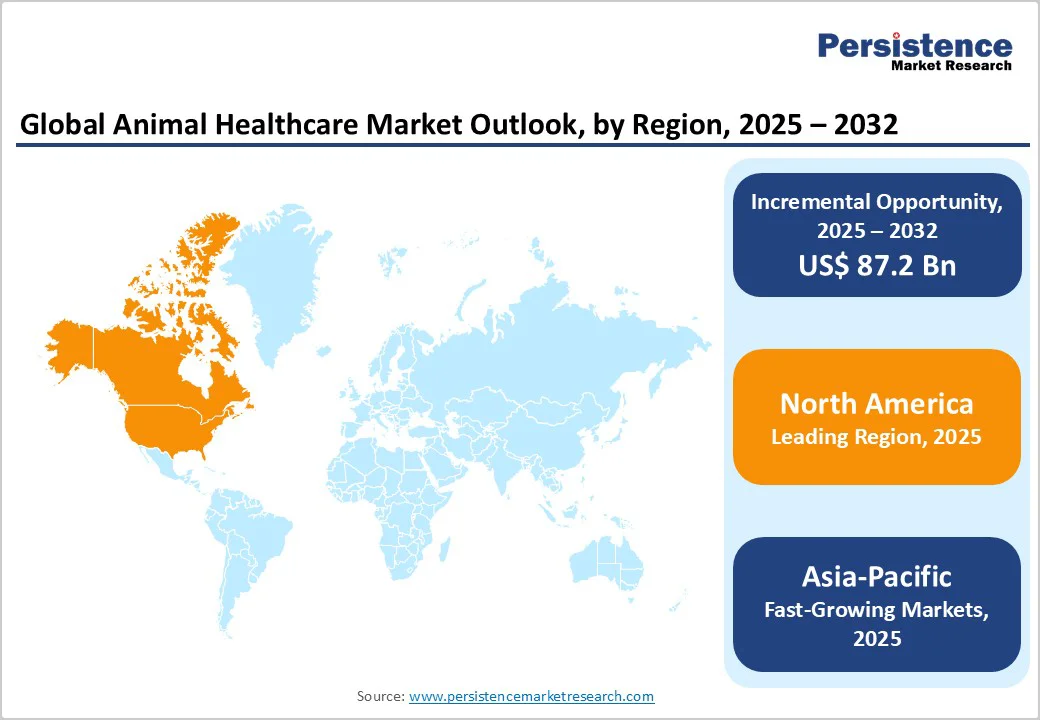

- Leading Region: North America dominates the global animal healthcare market with a share value of 43.4%, driven by a strong presence of major veterinary pharmaceutical companies, well-established veterinary infrastructure, high pet ownership, and stringent regulatory standards.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, fueled by expanding livestock production, rising pet ownership, increasing veterinary infrastructure, and growing alignment with global animal health regulatory standards.

- Leading Drugs Segment: Parasiticides lead the market with a share value of 41.0%, driven by their widespread use across companion and production animals, strong focus on preventive healthcare, and proven efficacy in controlling parasitic infections.

- Fastest-Growing Drugs Segment: Nutritional Products is the fastest-growing segment, supported by rising demand for immunity-boosting formulations, specialty feed additives, and supplements that enhance animal health and productivity.

- Leading Route of Administration Segment: Oral hold the largest share of 43.0%, due to easy administration, cost-effectiveness, and wide use in livestock and companion animals for antiparasitics, antibiotics, and supplements.

- Fastest-Growing Route of Administration Segment: Topical is experiencing rapid growth, Growing rapidly owing to rising adoption of pour-on and spot-on formulations for parasite control and skin treatments with convenient, non-invasive use.

| Key Insights | Details |

|---|---|

|

Animal Healthcare Market Size (2025E) |

US$ 65.4 Bn |

|

Market Value Forecast (2032F) |

US$ 99.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.0% |

Market Dynamics

Driver - Pet Humanization and Technological Advancements

The growing trend of treating pets as family members is significantly increasing per-animal spending on vaccines, diagnostics, specialty therapeutics, and wellness programs. This shift is expanding demand in companion-animal segments such as dermatology, pain management, and oncology, while driving steady revenue through preventive and subscription-based healthcare models.

The growing worldwide consumption of meat, dairy, and aquaculture products is prompting producers to enhance herd and flock health through vaccines, feed additives, diagnostics, and biosecurity measures to safeguard productivity and food safety. This is accelerating demand for veterinary pharmaceuticals and herd-level healthcare services, particularly in regions implementing intensive farming practices.

Restraints - High Costs of Advanced Products and Veterinary Services Restrict Market Access

The steep prices of premium diagnostics, biologics, and specialized veterinary care pose significant barriers for low-income farmers and cost-conscious pet owners. In many regions, escalating veterinary consultation fees, coupled with labor shortages, force owners to opt for more affordable alternatives or postpone treatments altogether. This limits the adoption of higher-margin products and services, constraining overall market growth.

Moreover, numerous regions struggle with insufficient veterinary staff, limited clinic availability, and uneven access to diagnostics and cold-chain logistics. These challenges reduce the frequency of preventive care and diagnostic services and hinder the deployment of advanced therapies, especially in rural and low-income areas.

Opportunity - Expanding Medical Device Industry Boosts Animal Healthcare Demand

The increasing adoption of pet insurance, preventive care packages, and subscription-based wellness models is creating stable, recurring revenue streams for clinics and manufacturers offering bundled services such as diagnostics, vaccines, and digital monitoring. This encourages uptake of higher-value services, including specialty care and advanced medications, while enabling cross-selling opportunities in companion-animal segments.

Furthermore, emerging markets such as India, Southeast Asia, and Latin America are experiencing rapid growth due to rising disposable incomes, expanding intensive farming, and improving veterinary infrastructure. These regions present strong potential for affordable diagnostics, generic pharmaceuticals, and large-scale preventive healthcare programs tailored to local production systems.

Category-wise Analysis

By Drugs, Parasiticides Dominate Globally Due to Their Widespread Use in Preventing and Controlling Parasitic Infections in Livestock and Companion Animals

The parasiticides segment is projected to dominate the global animal healthcare market in 2025, accounting for a revenue share of 41.0%. The segment’s strong performance is primarily driven by the rising prevalence of parasitic infections in livestock and companion animals, which significantly affect productivity, health, and welfare. Increasing awareness among pet owners and farmers about the economic impact of parasitic diseases has accelerated the adoption of anthelmintics, ectoparasiticides, and endoparasiticides for effective control and prevention. Additionally, the development of long-acting formulations, broad-spectrum parasiticides, and combination therapies that offer convenience and enhanced efficacy is further supporting market expansion.

By Animals, Companion Animals Dominate Globally Due to Rising Pet Ownership, Increased Spending on Preventive Care, and Growing Awareness of Animal Wellness

The companion animals segment is projected to dominate the global animal healthcare market in 2025, accounting for a revenue share of 59.5%. This is due to the rising trend of pet humanization, where owners increasingly treat pets as family members and invest heavily in their health and well-being. Growing awareness of preventive care, advanced diagnostics, specialty therapeutics, and wellness programs is boosting demand for veterinary services and products targeted at dogs, cats, and other companion animals. Additionally, expanding pet insurance coverage and subscription-based wellness models are further supporting the segment’s strong growth.

By Route of Administration, Oral Leads the Market Globally Due to Ease of Use, Cost-Effectiveness, and Wide Acceptance

The oral segment is projected to dominate the global animal healthcare market in 2025, accounting for a revenue share of 43.0%. This is due to its ease of administration, cost-effectiveness, and wide acceptance of oral formulations among both companion and production animals. Oral medications, including antibiotics, antiparasitics, and nutritional supplements, offer convenient dosing without the need for specialized veterinary procedures, encouraging higher adoption. Additionally, growing awareness of preventive care and increasing demand for livestock productivity and pet health.

Region-wise Insights

North America Animal Healthcare Market Trends

The North America market is expected to dominate globally with a value share of 43.4% in the 2025, with the U.S. leading the region due to the several key factors, including high pet ownership and the increasing humanization of pets, which fuels demand for preventive care, advanced diagnostics, and specialty treatments. The region benefits from a well-established veterinary infrastructure, a large pool of skilled professionals, and robust regulatory frameworks that ensure the availability and quality of veterinary products. High penetration of pet insurance and subscription-based wellness programs further supports the adoption of premium services and therapies. Additionally, rapid technological advancements, such as AI-enabled diagnostics, telemedicine, and biologics, are being integrated into routine veterinary care, enhancing early disease detection, treatment efficiency, and overall animal health outcomes. These combined factors position North America as the dominant region in the global animal healthcare market.

Europe Animal Healthcare Market Trends

The Europe market is expected to grow steadily, driven by several converging factors. Rising awareness of animal welfare and the increasing adoption of companion animals are motivating pet owners to invest more in preventive care, diagnostics, and specialty treatments. In the livestock sector, stringent regulations promoting food safety, responsible antibiotic use, and disease prevention are boosting demand for vaccines, biologics, and alternative therapies. Well-established veterinary infrastructure, a high density of skilled professionals, and expanding pet insurance coverage support wider access to quality animal healthcare. Furthermore, the integration of advanced technologies such as telemedicine, point-of-care diagnostics, and digital monitoring solutions is enhancing treatment efficiency and animal health outcomes

Asia and Pacific Animal Healthcare Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR of around 8.4% between 2025 and 2032, driven by multiple growth factors such as the rising demand for animal protein is prompting investments in livestock health, including vaccines, feed additives, diagnostics, and biosecurity measures to enhance productivity and ensure food safety. At the same time, pet ownership is increasing rapidly in countries such as India, China, and Southeast Asia, fueling demand for preventive care, wellness programs, and specialty treatments. Improvements in veterinary infrastructure, a growing pool of skilled professionals, and increasing awareness of animal health and welfare are further supporting market growth. Additionally, adoption of modern technologies such as telemedicine, AI-enabled diagnostics, and advanced biologics is expanding access to high-quality animal healthcare services. Together, these factors are creating significant opportunities for manufacturers, service providers, and distributors.

Competitive Landscape

The global animal healthcare market is highly competitive, with major players such as Bayer AG, Boehringer Ingelheim International GmbH, Virbac, Zoetis Services LLC, HESTER BIOSCIENCES LIMITED, Intas Pharmaceuticals Ltd., and Merck & Co leading the industry through extensive product portfolios, strong global distribution networks, and continuous innovation in veterinary pharmaceuticals, vaccines, and diagnostics.

These companies prioritize the development of advanced vaccines, biologics, parasiticides, and diagnostic solutions to enhance disease prevention, treatment accuracy, and overall animal health outcomes. Strategic initiatives such as mergers and acquisitions, capacity expansions, and partnerships with veterinary service providers and biopharma manufacturers.

Key Industry Developments:

- In November 2025, MSD Animal Health, a division of Merck & Co., Inc announced that the Secretaria de Agricultura y Desarrollo Rural (SADER) in Mexico approved EXZOLT™ 5% Pour-on (fluralaner 50 mg/mL) for use in the country. This innovative product belongs to the newest class of parasiticides, isoxazolines, and is effective in preventing and treating infestations caused by New World Screwworm (Cochliomyia hominivorax) larvae (myiasis).

- In September 2025, Sai Life Sciences, a Hyderabad-based contract research, development, and manufacturing organization (CRDMO), inaugurated Unit VI, a dedicated veterinary API facility in Bidar, India, located next to its flagship API site. The facility is designed to serve animal-health sponsors and contract clients, addressing the growing demand for veterinary medicines. Sai Life Sciences highlighted that the new site provides specialized manufacturing capacity compliant with veterinary-specific regulatory standards, supporting the production of high-quality APIs for the animal healthcare industry.

- In January 2025, Covetrus, a leading tech-enabled veterinary practice improvement company, introduced the Covetrus Platform™ ahead of the VMX 2025 Conference. The platform offers a comprehensive and connected suite of solutions tailored for modern veterinary practices. Combined with the expanding VetSuite network, the Covetrus Platform aims to unlock the full potential of veterinary clinics across the U.S., enhancing operational efficiency, client engagement, and overall practice performance.

Companies Covered in Animal Healthcare Market

- Bayer AG

- Boehringer Ingelheim International GmbH

- Virbac

- Zoetis Services LLC

- HESTER BIOSCIENCES LIMITED

- Intas Pharmaceuticals Ltd.

- Merck & Co.

- Elanco

- Ceva

- Alivira Animal Health Limited

- Vetoquinol

- Zydus Group.

- Norbrook

- Phibro Animal Health Corporation.

- Dechra

- Others

Frequently Asked Questions

The global animal healthcare market is projected to be valued at US$ 65.4 Bn in 2025.

Rising pet ownership, increasing demand for animal protein, and growing awareness of preventive care. Additionally, expansion of veterinary infrastructure and adoption of advanced diagnostics and biologics are driving the global animal healthcare market.

The global animal healthcare market is poised to witness a CAGR of 6.2% between 2025 and 2032.

Growing adoption of pet insurance, preventive care, and subscription-based wellness models. Rapid growth in emerging markets and increasing demand for vaccines, biologics, and advanced diagnostics are creating significant growth opportunities in the animal healthcare market.

Bayer AG, Boehringer Ingelheim International GmbH, Virbac, Zoetis Services LLC, HESTER BIOSCIENCES LIMITED, Intas Pharmaceuticals Ltd., and Merck & Co are some of the key players in the animal healthcare market.